Dekosig

Welcome to another installment of our weekly BDC market review, where we discuss market activity in the Business Development Company (“BDC”) sector from the bottom up – highlighting individual news and events – as well as from the top down – providing an overview of the market. Wider.

We also try to add some historical context as well as relevant topics that appear to be driving the market or that investors should consider. This update covers the period up to the fourth week of May.

Market action

BDC shares were roughly flat in a mostly down week for income markets. MSDL has performed poorly – the stock has been very volatile, likely due to the relatively low number of publicly traded shares. More shares will be issued after the lock-up period expires.

So far, the average stock in our coverage is up about 2%.

systematic income

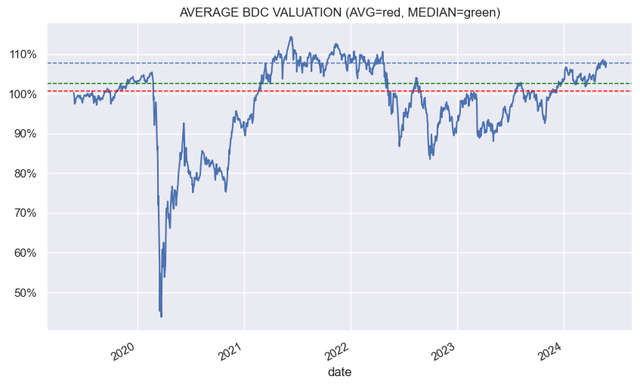

BDC ratings remain high. Although BDC valuations are not directly tied to net income, they are unlikely to rise further than current high levels in the face of the declining net income levels we have already seen in the first quarter.

systematic income

Market topics

One subscriber passed along some concerned comments related to BDC. The view appears to be that with “trillions” flowing into private credit markets, this could lower lending standards, while rising policy rates put pressure on borrowers, which could lead to increased defaults and defaults in investment portfolios. .

As far as the former is concerned, mathematically, trillions of dollars cannot flow into the private debt market if the size of this market is only $1.7 trillion and it takes 7 years to grow by $1 trillion. Furthermore, if we look at the capital at the disposal of business development companies, it’s not growing much – it’s only growing organically through market releases, the occasional IPO and retained income – a single-digit growth rate at best for most people. Business development centers.

Regarding deteriorating fundamentals, you could have said the same in 2022 when policy rates started to rise and the overall picture looked bleak. If you invest based on this view by avoiding BDC, you will miss out on a tremendous opportunity, with an average return of 32%.

Are non-accrual cases on the rise and are there defaults? Sure, in some places, but as always, we need to put things in context, which is that BDCs are still generating double-digit returns (i.e. total NAV returns) despite rising non-accruals and defaults. This is due to several levels of protection such as guarantees, sponsor shares, teams, restructuring assistance, etc. In fact, BDC managers complain that the fundamentals are too good – lending spreads are too tight and loans are made and are being repaid more quickly than expected, generating fewer opportunities which is why leverage is low across the sector.

Are there reasons for concern? Yes, but we would be more concerned about the fact that credit spreads are tight and BDC ratings are high than about vague things like “underwriting standards” or concerns about the future (who doesn’t have concerns about the future?). BDC directors are not puppets. They don’t want to make losses, so they won’t lend just because they have some capital.

Any type of analysis that links rates directly to defaults and BDC portfolio performance can look smart, but in reality it has little informational value. Things can always go wrong. It is more interesting to discuss why they did not make mistakes over the last two and a half years with rising interest rates than to ignore reality and continue to say that rising interest rates will only lead to poor BDC portfolio performance.

Quantitative analysis needs to be done (where are outstanding receivables high, are they large enough to be significant, are sponsors stepping up to support their companies, which BDCs have been the most resilient, and does the higher income of BDCs adequately offset the additional risk of default) repayment) and then noticeable to the market (if interest rate increases lead to non-accruals and defaults, why haven’t we seen more of them in the last 2.5 years).

The strategy of avoiding BDC when interest rates are high suggests that we should intervene fully when interest rates are low. This strategy would have been loading the boat at the end of 2021, precisely when BDC valuations were so high – even higher than they are today. This was not the time to turn to the upside as it was quickly followed by a sharp decline – creating a much better time to add exposure, especially since BDC net income levels were about to rise, as we highlighted at the time.

We are often asked what will happen to certain asset classes when interest rates rise or fall. Our answer is always that it depends on why prices are rising or falling. If interest rates are falling because we have entered a massive recession, it will likely be very bad for most credit assets. If interest rates are falling because the economy is going through a deflationary boom as we saw last year, that would likely be beneficial for most credit assets.

Our view at this point in the cycle is to hold some BDC exposure, with a particular focus on names that have been resilient through the cycle and those with modest leverage and high allocations to first lien loans. We have been reducing our exposure to the sector overall in the past few months, but not because of the rule of thumb of “high rates = bad” but because valuations are not far from historical highs. This value investing strategy is what has worked well in the past.

Market commentary

Saratoga Investments (SAR) raised its dividend by a penny. The stock has very high dividend coverage, so it was happy to adjust its dividend higher each quarter. SAR features what appears to be the highest level of leverage in the entire BDC sector – at around 2x versus an average closer to 1x. It would be different if that leverage were cheap, but about half of its bonds cost more than 8%, which leaves little, after fees, in terms of net investment income. NAV has also been volatile with non-accruals costing around 6%.

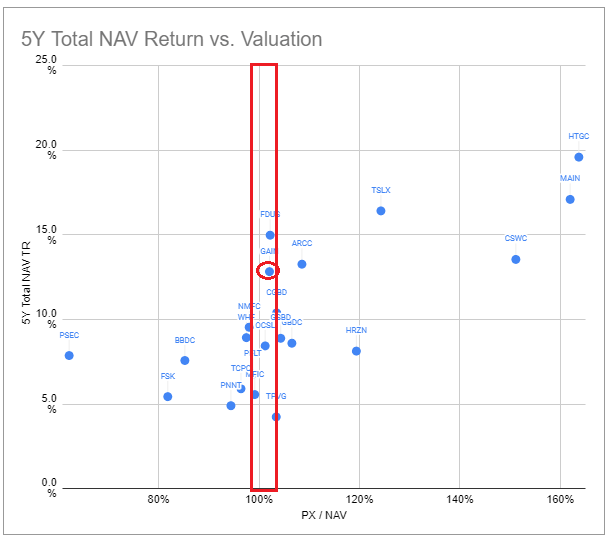

Gladstone Investment (GAIN) has stumbled recently, falling to a 2% premium to NAV this week – 6% below average and 1% below average. Of all the BDCs in trading coverage with a valuation close to 100%, only FDUS has a 5-year total NAV return. GAIN is somewhat unusual given its low first-lien allocation and somewhat undiversified portfolio, however, the historical performance speaks for itself.

BDC Systematic Income Tool

Attitude and fast food

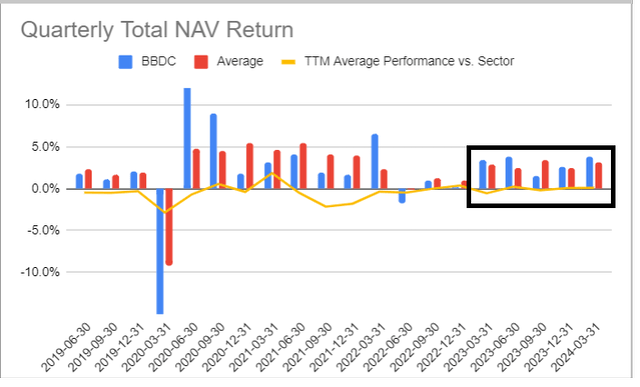

This week we added a position in Barings BDC (BBDC). The stock’s performance has been in line with the sector’s performance over the past 18 months or so, but it continues to trade at a significant discount – at a valuation about 20% below the sector average.

BDC Systematic Income Tool