JHVEphoto

At the Laboratory, our comprehensive coverage of the mining sector includes the BHP Group (New York Stock Exchange: BHP(OTCPK:BHPLF), Rio Tinto (OTCPK:RTNTF)(OTCPK:RTPPF), Glencore (OTCPK:GLCNF)(OTCPK:GLNCY), and Anglo American (OTCQX:AAUKF))(OTCQX:NGLOY). Since our last coverage,’Better outlook for goods but still expensive“BHP has made significant moves. Not only did they publish third-quarter results, but they also attempted a strategic acquisition of Anglo American assets. This is a noteworthy event, given our previous discussions about BHP’s M&A option; however, we believe that the Anglo American bid It has come to an end.

On May 29, the company stated: “BHP will not make a firm offer for Anglo American. BHP adheres to its capital allocation framework and maintains a disciplined approach to mergers and acquisitions“.

This was the third rejection from Anglo American’s board of directors. The latest offer valued the British company at 38.6 billion pounds. Anglo American was open to dialogue and awarded BHP Extension of one week to submit a new official offer. However, both Anglo American and BHP decided to step down. Anglo American incentivize The reason for rejection was always the same: “strategic concerns regarding structure”, material risks upon implementation due to regulatory approval, and disproportionate loss to existing shareholders. In addition, BHP’s proposal forced Anglo American to sell its entire stake in its platinum and iron ore businesses – Anglo American Platinum Limited and Kumba Iron Ore Limited.

As a reminder, BHP had already made two offers for Anglo American, both of which returned to sender: the first for £31.1 billion and the second raised to £34 billion. Counterparty management defined both orders as opportunistic with significant execution risks. Due to mounting pressure from shareholders due to BHP’s bids, Anglo American was also forced to accelerate a review of its asset base and introduced a major reorganization plan that includes the De Beers subsidiary and the sale of the production of its steel, nickel and platinum businesses.

Here in the lab, we think BHP’s timing has been very good (which is why we have a long-term buy rating on Anglo American called Too Cheap To Ignore); However, the price of copper and the complexity of the deal made this deal difficult to execute. However, since our last update, we believe BHP offers a better entry price.

Marie Eve. BHP laboratory classification update

Third quarter results

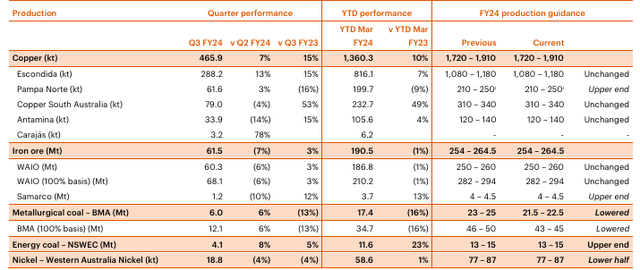

Very briefly, BHP Group reported mixed third-quarter results on a standalone basis. In summary, copper performed strongly, iron ore was in line with company guidance, while nickel and coal performed weaker than expected. Looking at the results, the copper division was supportive, thanks to the Escondida grade upgrade. WAIO requires a record Q4 on iron ore to meet the midpoint of BHP’s guidance. Shipments were in line with consensus, but the company was affected by bad weather and ramping up of rail infrastructure. Regarding the outlook, the company left iron ore and copper unchanged, but the Met coal rating was downgraded again. In detail, the coal forecast has been reduced from 46-50 million tons to 42.5-45 million tons due to weather impacts and is now -25% compared to BHP’s initial guidance. However, the stock is still low, and we believe this could lead to a reset starting in 2025. On the downside, Nickel’s performance has not been on track. The company now provides lower guidance for the end of fiscal 2024 of between 77 and 87 thousand tons. We believe BHP will issue a strategy update with a potential closure or new capital maintenance.

BHP results for the third quarter

Source: BHP press release – Q3 results

It’s a better entry point, but it’s still expensive.

We are more preferable for the following three reasons:

- (No deal offers a better entry price). Here in the laboratory, drawing on in-house Anglo-American research, we estimate the growth of copper production To 700 kilotons in 2035 from 550 kilotons in 2023. Quellaveco expansion pays offAnd we Mentioned“,”The value of this sector is approximately 21 billion US dollars, with an annual capacity of 35 thousand US dollars/ton.” this It is the basic scenario. In the expansion scenario, our NPV of the copper mine rises to approximately $25 billion. here in According to the lab, EBITDA could increase from $2.5 billion to $5 billion in 2030, including lower unit costs. Consider BHP’s interior OZ Minerals Evolution BHP’s EBITDA would have been 46% of the company’s commodity mix in a consolidation scenario. However, we must point out that there are significant risks in implementation. Here at the laboratory, we take into account regulatory approvals, mining plan details, long-term costs and copper grade profiles. As potential investors in BHP, this transaction was very complex and, in our analysis, it was not clear that the agreement was accretive;

- (Reduce complexity and continue divestment into lower quality assets). On April 2, BHP successfully completed the Blackwater and Donia mines with a total value of $4.1 billion. For this reason, we now expect the debt at the end of 2025 to reach $8.5 billion;

- (Resilience in iron ore and the upside of internal copper splitting) Looking ahead and considering the slight changes in BHP’s forecasts, we now expect $55.5 billion in higher sales with EBITDA of $29.2 billion in 2025. WAIO backs this up. This is the world’s lowest cost iron ore producer, achieving impressive results despite heavy rainfall. The company continues to invest in capital operations of railways and ports and is progressing well to achieve 305 million tons per annum. As a reminder, our assumptions for iron ore are set at $125 per ton. BHP’s EBITDA is skewed towards iron ore, since the commodity represents 60% of BHP’s exposure. Coal, thermal coal and stainless steel materials account for only $8.6 billion in sales in our future estimates. Additionally, following the acquisition of OZ Minerals, the company now has an internal cash cow to generate significant value. In addition towhich remains tied to copper production, Spence is on track toward the higher end of guidance.

evaluation

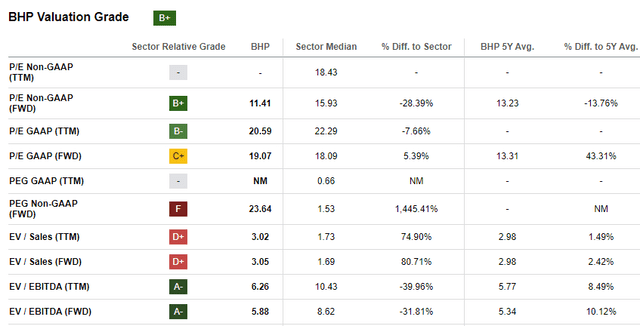

In terms of valuation, given the lower estimates and the spot price of iron ore of $105 per tonne, we decided to lower the EBITDA estimate to $29.2 billion. At our last assessment, BHP’s EV/EBITDA was more than 6x. Following the Anglo merger proposal, the company is now trading at 5.6x. This is in line with its 5-year historical average (5.77x). We therefore rate the company with a price target of A$60 per share (A$42 per share), underscoring a Neutral view.

Find Alpha Data Evaluation

Risks

Downside risks include political, financial and operational. Each has the potential to significantly impact a company’s performance. In addition, lower commodity prices may impact BHP and its earnings sensitivity. Construction or business surge risks are associated with WAIO, specifically with respect to increased costs and delays. The irrational and value destruction of mergers and acquisitions should be considered a relevant downside.

Conclusion

The company has a strong balance sheet and a good dividend policy. In the longer term, this could be good momentum to get into, while on a 12-month basis, iron ore and copper price trends and Samarco settlements will be important catalysts. For this reason, we affirm our view of a neutral rating.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.