Michael VI

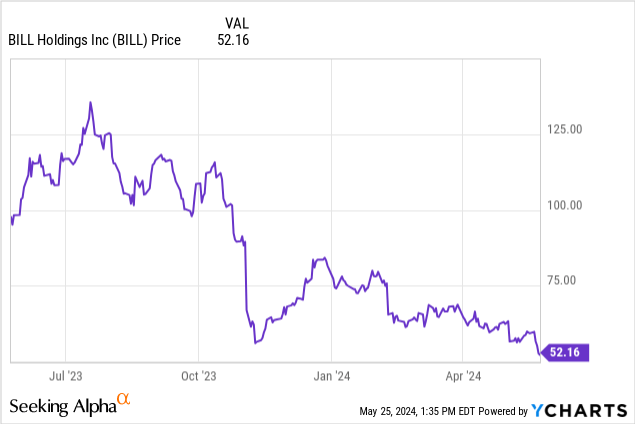

With markets hovering nervously around all-time highs, this is a good time to be a stock picker and invest in companies whose stock prices and individual fundamentals are in complete turmoil. Bell Holdings (New York Stock Exchange: Bell) great Case in point: A small business invoice management software company saw its valuation fall sharply this year. Although it hasn’t been entirely smooth sailing for the company itself, the stock price suggests a struggling company: in reality, it’s not.

Year to date, Bill.com’s price is down more than 30%, bringing the stock to all-time lows for the year (in fact, the last time Bill.com traded at around $50 was in early 2020). It’s hard to imagine that this company was once a Wall Street darling commanding double-digit valuation multiples, and now the stock has been taken to… Penalty basket. It’s a great time, in my view, for investors to reevaluate the bull case for this name.

Don’t worry because Bill.com is moving up a bit; Reconsider the bull case

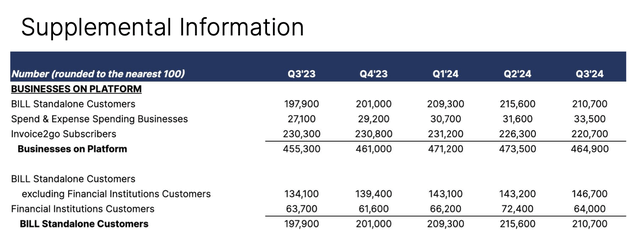

Let’s address the elephant in the room first: Why is Bill.com collapsing? One of the primary reasons the stock has come under pressure is that not only has customer growth slowed, but the number of customers has actually declined. In the company’s most recent quarter, Q3 (the end of Bill.com’s March quarter), total independent customers fell by almost 5k to 210.7k (although up 6% year over year):

Number of Bill.com customers (Bill.com Q3 Contributor Group)

But what we should note is that the company did just that Deliberately go into market changes. The company has pulled back on marketing spending on smaller customers and placed this customer segment largely on a self-service model; At the same time, the number of customers is decreasing because the company is removing active customers.

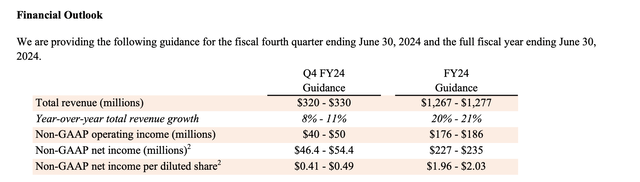

But at the same time, revenues continue to grow well above expectations; In fact, the third quarter was an “over-and-over” quarter, and the company raised its full-year forecast to 20-21% YoY growth (versus a previous forecast of 16-18% YoY growth). This is due to the fact that larger enterprise spending is higher than expectations, offsetting the weakness of SMEs. Take a look at the company’s latest forecasts below:

Bill.com Forecast (Bill.com Q3 Contributor Group)

I wrote my last bullish opinion on Bill.com in February, when the stock was still trading at $66 per share. Given the increase in guidance and the corresponding decline in the stock price, I am now upgrading my view on Bill.com to Solid deal.

Here’s my full long-term case on Bill.com:

- Wise management of growth Despite already reaching an annual revenue run rate of $1B+, Bill.com has still managed to grow revenue at an impressive 20% year-over-year growth rate (and note here that the company’s recent major acquisitions of Invoice2Go and Divvy are now fully completed). Also note that the company is deliberately withdrawing marketing spending from small customers and moving into the high-end market.

- Massive global TAM. In its latest shareholder roundup, the company estimates that small and medium-sized businesses spend $344 billion on software, and that business-to-business transaction flows reach $125 trillion annually.

- Floating revenues will benefit from a higher interest rate environment. Float now contributes just over 10% of the company’s revenue, from almost nothing during a period of low interest rates, and this is a “free” way to help boost BILL Holdings, Inc.’s margins.

- Automation push. Today, while artificial intelligence and automation are hot topics, there is a growing interest in automating manual processes and chasing as much efficiency as possible – all of which are part of BILL Holdings, Inc.’s core DNA.

- Very high gross margins. BILL Holdings, Inc.’s gross margins are… That reaches into the 80s is unparalleled in the industry. As the company continues to grow its customer base and capture a larger portion of those customers’ transactions, the fact that BILL Holdings, Inc.’s revenues Almost flowing to the bottom line will help the company expand its profitability significantly.

All in all: Stay long here and take advantage of the fact that Bill.com is trading at multi-year lows to buy the dip with confidence.

Download Q3

Let’s now review Bill.com’s latest quarterly results for its fiscal third quarter (March quarter, released in early May) in more detail. It should be noted that Bill.com stock has fallen significantly since these earnings were released, and that the stock has been trading In the mid-60s (about 20% higher) before earnings.

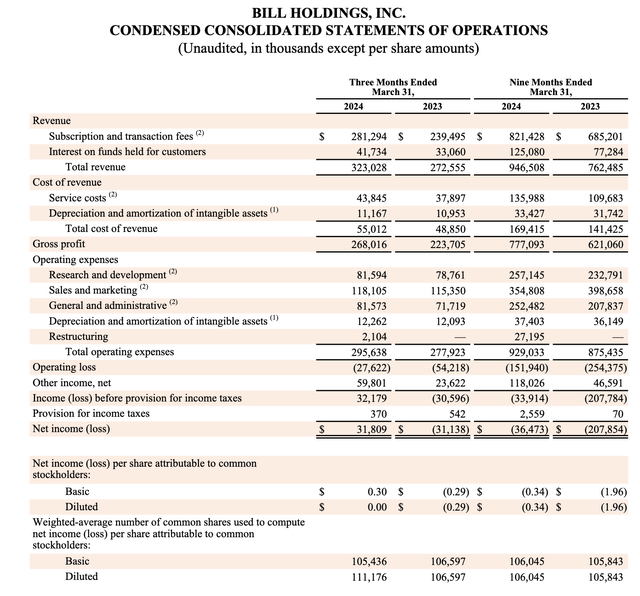

Bill.com’s third-quarter results (Bill.com Q3 Contributor Group)

Revenue grew 19% year-over-year to $323.0 million, well ahead of Wall Street expectations (+12% year-over-year) by a whopping seven-point margin. Also note that as usual, Bill.com guided the low end for the quarter with a growth range of 10-13%, and the company came in six points above the high end of that midpoint. Likewise for Q4, investors are critical of the company’s guidance for 8-11% year-over-year growth, but Bill.com has a long track record of beating its conservative forecast.

Also note that the flotation continues to be a big tailwind for Bill.com, as interest income increased 26% year-over-year to $41.7 million in revenue for the quarter. In this way, Bill.com could be a great hedge against the possibility that interest rates will remain higher (which is generally bad for valuation multiples, but great for Bill.com’s revenues).

The good news this quarter: Although SMBs declined as expected, institutional purchasing patterns showed signs of normalizing. According to CFO John Rettig’s remarks on the third-quarter earnings call:

The aggressive execution of our top priorities showed early positive signs in the third quarter. Net new customer additions for both BILL’s spending and standalone XFi solutions are back at historical levels. The B2B spending environment has shown signs of stabilization. Our focus on companies with a higher propensity to spend has led to an upside in our spending and expenses business. BILL standalone payment monetization has been serially expanded. All of these factors translated into profitable growth in the third quarter (…)

We are raising our 2024 financial outlook to reflect the progress we have made in strengthening our core while remaining cautious regarding ongoing macro headwinds that could negatively impact SME spending. While there have been signs of stabilization in the corporate spending environment, SMEs are still under pressure due to high inflation and interest rates.

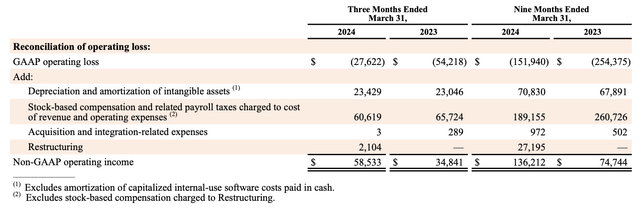

In my view, Bill.com’s gradual upmarket shift is a lever for more profitable growth and should be applauded. Also notice, as shown in the image below, that pro forma operating income jumped 68% year over year to $58.5 millionrepresenting a pro forma operating margin of 18% – up from 13% in the same quarter last year.

Bill.com’s operating income (Bill.com Q3 Contributor Group)

Clearly, lower marketing expenditures on smaller customers lead to positive results. Also note that with revenue growth of 19% and pro forma operating margins of 18%, Bill.com is within striking distance of the so-called “rule of 40.”

Evaluation, risks and key takeaways

At current stock prices at under $50, Bill.com is trading with a market cap of $5.54 billion. After we deduct $1.79 billion in cash and $966.2 million in convertible debt from the company’s most recent balance sheet, the result is Enterprise value: $4.72 billion.

For next fiscal year 25 (the year Bill.com ends in June 2025), Wall Street analysts expect the company to generate revenue of $1.44 billion, or 13% year-over-year growth. This puts Bill.com’s rating at 3.3x EV/Revenue FY25 – Very low for a company with pro forma gross margins over 80%, pro forma operating margins near 20%, and multiple enablers for continued revenue growth.

There are risks here, of course. Institutional buying patterns are highly cyclical, and although Bill.com has noted signs of normalization, other software companies have continued to point to tight budgets — which could upend this narrative in the near term. We also note that Bill.com faces competition from other AR/AP automation companies like Stripe and NetSuite.

Overall, I think the sharp decline Bill.com has seen over the past few months has created a massive buying opportunity: stay here long and buy the dip.