Da cook

In my recent thesis on the ProShares Bitcoin Strategy ETF (NYSEARCA: BETO) titled “Uptrend Likely to Continue Until Halved Amid Volatility” On March 6, I had a bullish position that materialized, but only to some extent when the stock price rose from $30.83. To a peak of $33.65 one week later. However, volatility later prevailed and it is now trading at around $27.

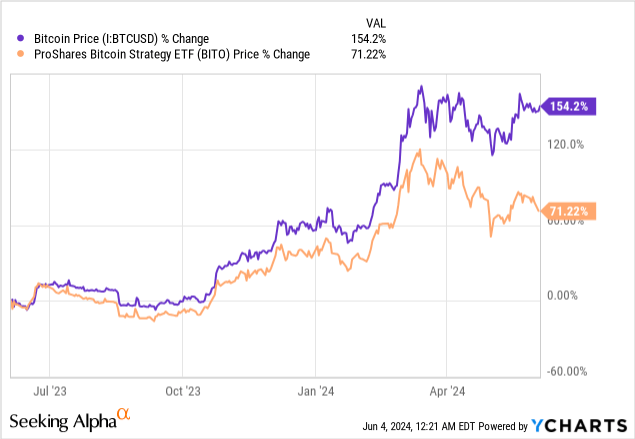

Also, the chart below shows that BITO’s underperformance compared to Bitcoin (BTC-USD) may get worse raising the issue of capital preservation.

Against this background, this thesis aims to show that BITO is a property for shareholders due to its profits, but for potential investors, it is better to wait until the period of turmoil is over. For this purpose, I will explain how market dynamics have changed dramatically this year and compare ETFs and alternative investment funds Investments that allow exposure to cryptocurrencies without actually owning the coins.

First, I provide reasons why BITO’s momentum was not maintained after its initial rise to $33.65.

Understanding price action

After the SEC approved 11 Bitcoin spot funds on January 10, the demand for the cryptocurrency increased, but its price did not reach $79.3 thousand according to my expectations. Instead, it only reached a peak of around $73,000 before falling. One reason for this is that the total daily trading volume of the 11 ETFs fell from $4.47 billion on March 6 to $2.87 billion at the end of April. Since this period also saw BTC lose 13% of its value, this means that the decline in trading volumes was accompanied by a decline in demand for cryptocurrencies.

In this regard, unlike BITO which holds Bitcoin futures contracts, newly issued ETFs must be backed by actual Bitcoin or require fund managers to purchase coins on the open market. So, as the price of Bitcoin fell, so did the Bitcoin-linked ProShares ETF as shown below.

www.proshares.com

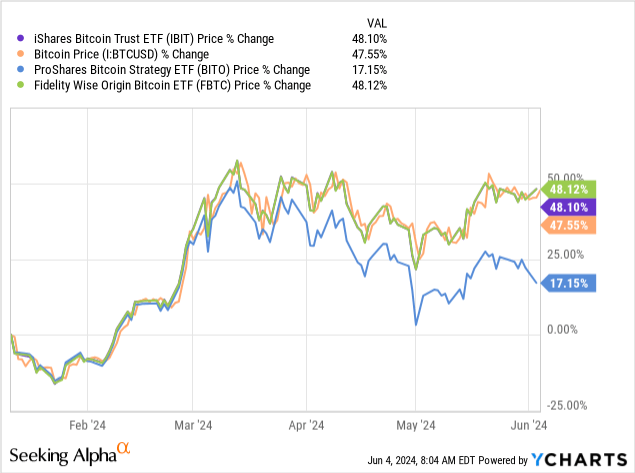

The second reason that explains the poor performance of the ProShares ETF is the departure of some investors. In this regard, for those who want direct exposure to Bitcoin without having a cryptocurrency exchange account or wallet, the 11 new ETFs, two of which are iShares Bitcoin Trust (IBIT) and Fidelity Wise Origin Bitcoin ETF (FBTC) represent an alternative. Investments in BITO. Thus, with more options, investors may have turned to these spot ETFs which closely track the price of Bitcoin as shown below.

Furthermore, an added advantage of these new funds is that their fees remain much lower than BITO’s fee of 0.95%. However, these fees are largely offset by their dividend yields of over 20% which are particularly attractive to income seekers.

Generating profits from investment income and capital gains

Looking further, it may seem strange how a fund that invests in financial derivatives (or futures) related to Bitcoin can pay dividends. To achieve this, fund managers sell Bitcoin futures contracts for cash each month, generating profits or net investment income, which is then distributed to shareholders as dividends. Moreover, distributions are also made from capital gains.

However, as explained below, dividends tend to vary and there is no guarantee that the payments will be made each month as in September 2023 and in January and June of this year. However, the dividend yield is about ten times higher than the 2.57% average for all ETFs.

Earnings/History (seekingalpha.com)

Hence, with a dividend grade of A+ coupled with superior momentum and liquidity scores, BITO is rated a Strong Buy by Quantitative ratings. However, given the volatility after the halving and for those wondering if this is the right time to position their positions, it is better to wait as it may fall further.

Futures held hints of a further decline

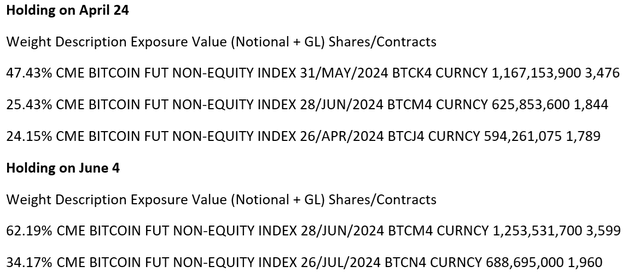

Looking deeper into the investment income strategy, the image below shows BITO’s holdings on April 24. In this case, the 24.15% of CME Bitcoin futures contracts, which were scheduled to expire on April 26, tend to show that fund managers expected short-term gains, or a rise in cryptocurrencies following the halving that occurred only in April. 19.

BITO Bitcoin Futures Holdings (www.proshares.com)

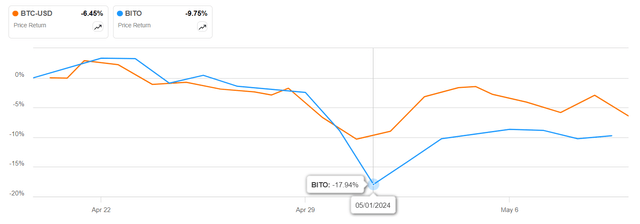

However, this did not happen, on the contrary, the cryptocurrency lost about 10% in April. However, the fact that BITO paid a higher dividend of $1.68 on May 1 as shown above shows that it may have sacrificed part of its capital appreciation. This is confirmed by the fact that BITO reached a low of $23 on the same day while, at the same time, varying significantly compared to BTC as shown in the blue chart below.

seekalpha.com

So, in addition to the possibility of some investors shifting away towards spot ETFs to gain more direct exposure to cryptocurrencies, BITO’s income strategy appears to have played against its price performance.

Going forward, the fact that holdings on June 4 hold futures contracts expiring on June 28 and July 26 (top image of holdings) shows that fund managers have switched to a relatively long-term strategy, perhaps because they do not expect a short-term period. BTC price rise.

This long-term strategy is in line with the possibility of cryptocurrency prices coming under pressure as miners adjust to halving/aggregate difficulty issues in the short term. In this regard, one of the factors weighing on Bitcoin prices is miners emptying their treasury of HODLed BTCs to counter the halving event that reduced the perceived rewards for each block mined. At the same time, increasing mining difficulty makes it take longer to produce the same output of current computing power (hash rates). Thus, they may have to liquidate approximately $5 billion worth of Bitcoin to fund their operating expenses, which is a large amount especially considering that they were mostly holding it before the halving event.

I’m looking for a middle ground in the turmoil

Miners selling crypto assets may also be motivated by the economic environment characterized by rising costs of capital as interest rates continue to remain above 5%. In addition, operating costs remain high with inflation remaining above 3%. Thus, any news that increases the chances of the Fed turning dovish is welcomed by crypto enthusiasts, and this was the case on June 3 when both BTC and BITO rose more than 1% each. This followed news of weak manufacturing which in turn led to a downward revision in GDP growth from 2% to 1.8% through May. However, making an investment based solely on interest rate cuts by the Fed due to the economic slowdown is speculative, as the related upward trend is unlikely to continue.

Furthermore, the value of Bitcoin must rise sustainably such as in 2023 to allow BITO to fund its distributions through futures trading or use of investment income, in a way that does not impact capital appreciation. In the absence of such a possibility at this point, this means that the stock price may continue in a downward trend, a possibility also indicated by momentum indicators: the stock price is below the 10-day and 50-day moving averages.

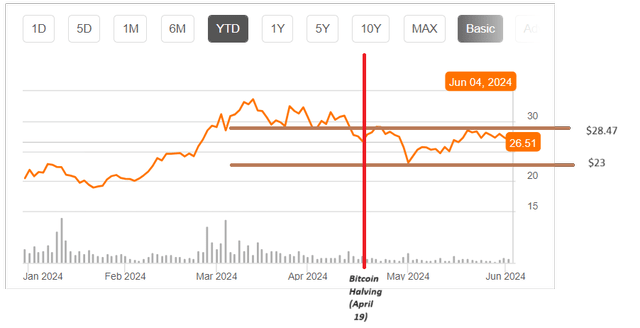

Therefore, the price could once again touch the $23 level last reached in May as shown below, along with potentially falling further for three reasons. Firstly, this is the lowest price BITO has reached after the halving, which as I mentioned above, is a period also synonymous with more miner-led supply. Second, inflows into spot ETFs appear to have stabilized as mentioned earlier, which may prevent further capital outflows from BITO. Third, to counter further downside, fund managers have the option to fund dividends only using investment income, and this appears to be the case on June 1 when no dividends were paid, thus not putting BITO’s share price under further pressure.

The graph was prepared using data from (seekingalpha.com)

In these circumstances, $23 can be considered the support price in the current period of turmoil.

Main sockets

In conclusion, this thesis showed that market dynamics changed radically in 2024. While 2023 was a more normal environment with Bitcoin rising by 153%, which made it easier for BITO to generate investment income from trading futures to pay regular monthly payments, it appears This year is completely different. It is worth noting that the cryptocurrency rose by 56% but its path was more volatile, with three factors affecting the supply and demand equation, starting with the emergence of spot ETFs, followed by the halving without forgetting the difficulty of mining.

To complicate matters further, the SEC has approved Ethereum Spot ETFs (ETH-USD) that could attract up to $4.8 billion in net inflows. Now, that money could come from investors wanting to diversify away from Bitcoin as was the case during previous post-halving periods, where crypto enthusiasts chose altcoins like Ethereum over Bitcoin for several months. Therefore, the period of turmoil is likely to continue, which means that this is not a good time to invest.

In such circumstances, the income justification makes a lot of sense for existing shareholders, as BITO has already paid a total of $3.9 in dividends per share this year compared to just $3.1 for all of last year. However, the risk is that severe future volatility may prevent fund managers from using the derivatives trading mechanism to generate sufficient investment income.

Finally, for those considering putting new money in the long term, $23 could constitute an entry price, but keeping in mind that BITO is likely to be range-bound at an upper limit of $28.47 for some time to come, unless the Reserve Bank cuts Federal Reserve rate. Interest rates or Bitcoin miners are quickly adapting to the post-halving landscape.