Tinnakorn Jorruang/iStock via Getty Images

Main message & background

The purpose of this article is to evaluate BlackRock Income Trust (New York Stock Exchange: BCT) as an investment option at the current market price. This box is the one I wrote About several times, it is I managed By BlackRock (Black), with the goal of “managing a portfolio of high-quality securities to achieve capital preservation and high monthly income,” primarily through exposure to mortgage-backed securities.

While I had been using agency MBS as an equity hedge in my portfolio for years, I switched to other options (such as municipal bonds) and liquidated my BKT positions. However, I keep this fund under my radar because I’m always willing to change allocations when necessary. When I looked at BKT at the end of last year, I saw quite a bit Negative background. In fairness to me, the fund saw a sharp decline immediately after that review. However, it has risen strongly and thus made a fairly good return despite stumbling over the past couple of months:

BKT price action (Searching for Alpha)

However, it goes without saying that we live in a much different macro environment today. So this has led me to consider whether I should raise my rating on BKT – and agency MBS more broadly – for the second half of 2024.

After reviewing, I still see a mixed picture of this particular box, but I think the bear case is a bit dramatic here. This leads me to believe that the upgrade to “suspension” is justified. There are some headwinds – which I will discuss in this article – but there are also some positives that lead me to believe that a modest return is what will ultimately happen for the rest of the year. Therefore, I’m putting the “hold” rating in place, and I’ll explain why in more detail below.

Let’s start with the good

I like to open most reviews by discussing the most convenient aspects of the box — even if I don’t recommend purchasing it. This is useful in providing some balance and also a counterargument to my overall thesis. I feel this helps readers make the most informed decision.

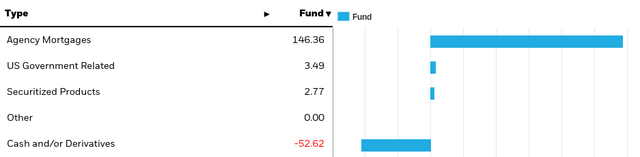

In the case of BKT, there are actually some positives. To make sense of it, I would remind my followers that this fund is highly leveraged in only one area. These are agency MBS (which primarily expose investors to the US residential housing market):

BKT makeup (Black stone)

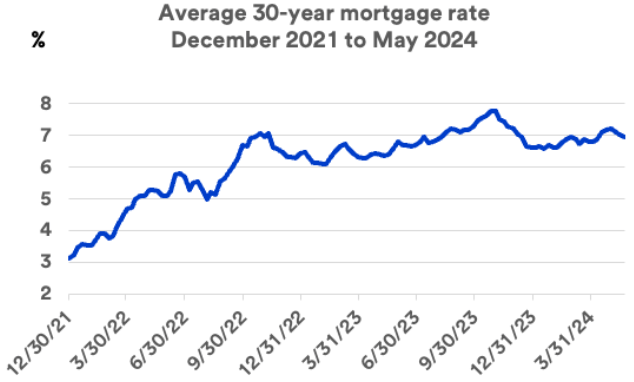

This sector has been flashier than in recent memory because interest rates have been historically high compared to the past two decades. This means that mortgage rates are also high – allowing BKT to generate an above-average income stream for the fund’s owners. This means that the “safe” and boring MBS sector is posting returns in the 6-8% range. Not too shabby:

Mortgage rates in the United States (us bank)

This extends to funds (such as BKT) that hold the securities backing these mortgages. BKT’s current distribution rate is 9% (I’ll explain why I don’t think this is sustainable later), which is a product of how the mortgage market has changed dramatically since I started as an investor in the early 2000s:

BKT distribution (Black stone)

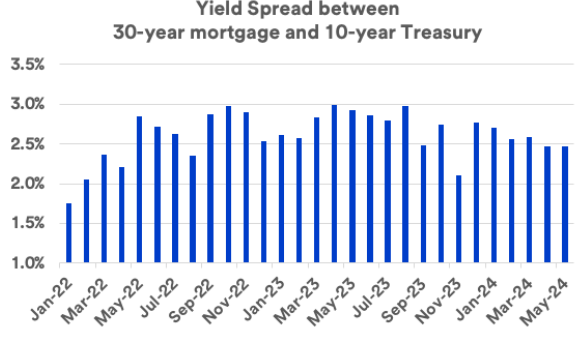

This has led to MBS being a great opportunity for even the most passive investors. Since these securities are backed by federal agencies (protecting investors from mortgage delinquency and foreclosure risk), they are generally considered risk-free products in line with Treasuries in my view. However, the spread between MBS and US Treasuries is large enough to attract a lot of buyers into the space:

MBS offer additional return (CNBC)

As you can see, this metric is starting to trend downward, but it still presents investors with a positive delta. This is not going away in the near future, so the opportunity is still here. I think this provides some support why a bearish view on BKT is no longer the right decision – investors will see a positive spread and rotate at some level. This is especially true if the trend changes and the spread with Treasuries widens. This probability is enough to conclude that the “wait” is as low as one should go with this option.

The valuation is still reasonable

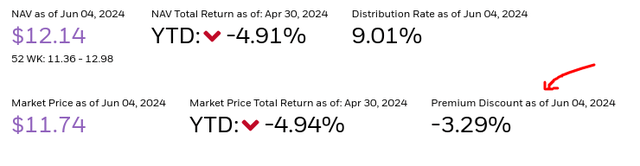

Another positive attribute of BKT is the fund’s valuation. As with all mutual funds, this is an ever-evolving metric, but at the time of writing, the market price of the fund offers a discount to NAV of over 3%:

BKT Evaluation (Black stone)

It’s fair to say that I like discounting, all other things being equal. One above 3% is actually reasonable. But while I see this as a positive trait, I do so modestly. BKT often trades at much larger discounts than this current level. In fact, they’ll sometimes offer discounts in the double-digit range!

So, while investors get some value from opening a position here, it is not type I value truly I want to see — the best discount in both isolations and the broadest discount in terms relative to the fund’s trading history. Without this dynamic here, I don’t see this as a supportive buy, although it does suggest that the fund is not overpriced at the moment.

Where are the risks? Refinancing in the future

Now I want to turn to some of my interests. The first is to refinance future risks. This could be a drag on future income flows, because as homeowners refinance, old debt is reissued at prevailing (and perhaps lower) interest rates. This puts pressure on the income stream offered by the sector and will spill over to mutual funds like BKT that hold those securities.

But hey, you say, refinancing is at historic lows – isn’t that a positive thing? The answer to that is definitely yes at present. I am no Saying this is an immediate headwind. In fact, low levels of refinancing activity are actually a reason why BKT has performed so well over the past six to twelve months. Mortgage rates are high and borrowers have not been able to take advantage of falling rates to change that.

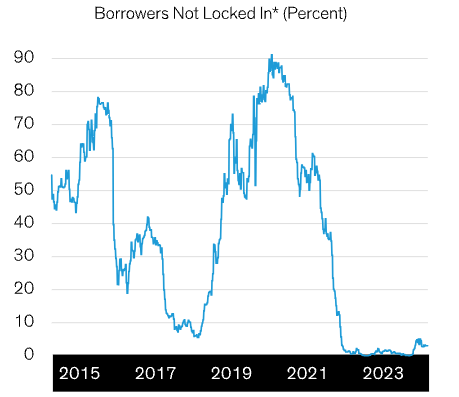

Furthermore, borrowers who purchased homes before interest rates rose remain locked into those lower rates and have no incentive to refinance (because the new interest rate will be higher). Currently, over 95% of the mortgage market is “out of the money” from a refinancing perspective:

There is no incentive to refinance (Bernstein Alliance)

So why do I have this as a concern in the future? My idea here is that refinancing activity will increase in the future. Honestly, I think it’s almost impossible to go down. Mortgage rates are unlikely to rise from current levels, and I expect interest rates to be lower than we see today in 6 to 12 months. The impact will be that homebuyers of the last couple of years will finally be able to refinance to lower their mortgage burden, and that’s certainly something I see happening as we wrap up 2024 and head into 2025.

This really isn’t meant to be alarming. If so, I would put a more bearish rating on this fund. Furthermore, I don’t see this as an immediate risk as investors need to make big moves now. My forecasts are a long way off – likely starting in Q4 – so there is time to make adjustments.

But that’s the point of investing. Being forward-looking. I don’t want to buy something that will see a less favorable college background in the following semesters. I’m not opposed to making short-term trades, but it should be for a better reward offer than BKT can offer. The truth is that the prime time to buy agency MBS (and BKT by extension) may have passed. Instead of chasing returns here, I will simply look for more value elsewhere. This supports my “commentary” point on this product.

The Fed/banks are not the buyers they used to be

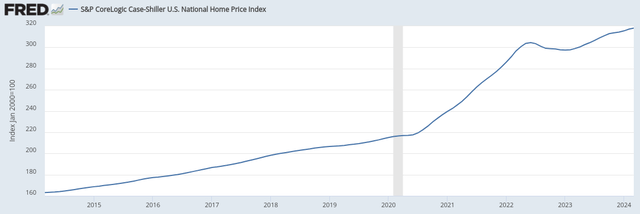

The other macro headwinds facing the agency MBS sector come from the demand side of the equation. Specifically, lower Fed/Treasury purchasing, which has risen in recent years with government intervention in the mortgage market. Now, with home prices rising and the Fed hoping so amazing Housing prices, the net effect will be less aggressive buyers outside of Washington, D.C.:

S&P CoreLogic Case-Shiller US National Home Price Index (St. Louis Federal Reserve Bank)

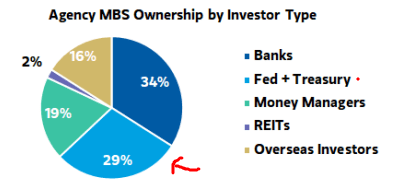

This begs another question – how important is this dynamic? In my view, this is very important, because the Fed and the Treasury combine to account for roughly a third of the demand for agency MBS:

MBS agency owners (Standard & Poor’s Global)

The challenge here is that the Fed was once the largest buyers of agency MBS, and now they are allowing the securities to mature and reducing their demand to buy new issues. According to the latest FOMC statement, the maximum redemption of agency debt and MBS will be

“Unchanged at $35 billion.”

Source: Federal Reserve

This means that investors in this space cannot continue to rely on the Fed to raise asset prices. Other buyers will have to step in.

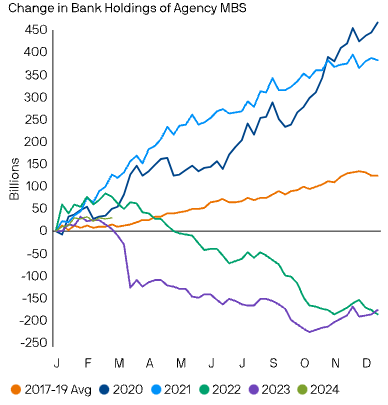

And there is a problem because the other big player – the big financial institutions/banks – are also pulling back on their demand. This is due to a number of factors that I will not go into here, but the end result is that demand and holdings among large US banks have declined significantly from years past:

Bank of America’s MBS holdings (by year) (JP Morgan)

The general idea for me is that two of MBS’s biggest agency buyers are out of business and will remain more modest players in the space for the foreseeable future. Can others intervene? Certainly, retail and other institutional buyers could. But will their purchase be enough to make up the entire difference? It’s hard to say this, but I’m inclined to say no because it will be difficult to match what the Fed and the big US banks can do. This will likely put downward pressure on the prices of BKT’s underlying securities and is a fundamental reason why I am not a buyer here.

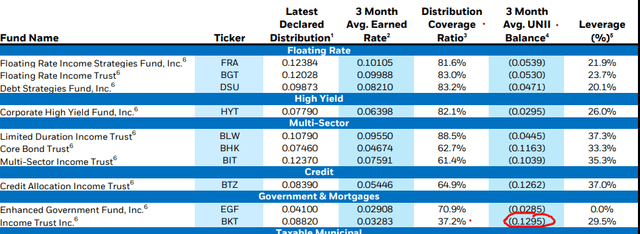

Income metrics are still scary

My final point is about income production. While BKT’s return is high on the surface, its sustainability is what I would raise questions about. In my view, a “high” yield is no good if it’s not sustainable because it leaves investors wondering when the distribution-reduction sell-off will happen – as they often do. This is a headwind for me when evaluating BKT because I believe a cut is a matter of when, not if.

The reason is that the fund’s income metrics are very worrying. The distribution coverage ratio is poor and the UNII measure shows that the fund has not received enough income to cover the current payment:

Latest income metrics (Black stone)

It is difficult for me to extract anything positive from this report. In fairness to BKT, its metrics in this regard have been weak for a while, it continues to pay out its compensation and the price has been fairly flat. But my view is that this will change at some point this year. And I don’t want to be “holding the bag” when that happens.

minimum

BKT had a great run until it concluded in 2023, but its performance since then has been poor. However, I see good justification for upgrading my view because the discount to NAV remains intact, and because agency MBS has a positive spread on Treasuries, this fund pumps out a yield that will appeal to income-oriented investors. Although I personally wouldn’t want to own it here, I see enough supporting elements for that Others You may like it.

Of course, there are headwinds, which is why the “hold” is as high as I will go. Refinancing activity is certain to rise in the future, which will put pressure on income production in this fund, which is already facing an earned income shortfall. Additionally, the discount to NAV isn’t attractive enough based on its trading history to get me excited. Finally, major buyers of MBS, including the Federal Reserve and US banks, are pulling back on their exposure and that remains a major positive catalyst for the sector. When I put it all together I don’t see a compelling buying case and I think caution is warranted on some level at this time.