Klaus Wiedefelt

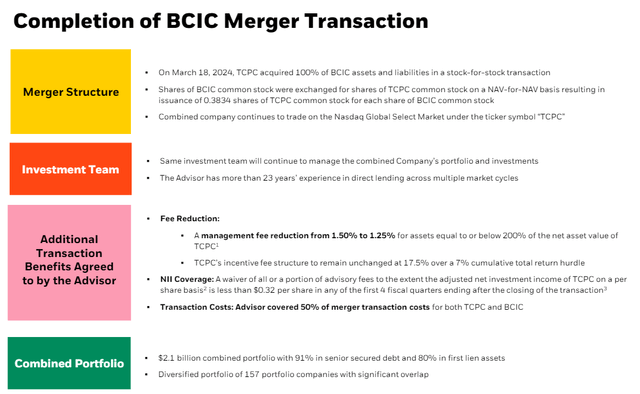

BlackRock TCB Capital Corp (Nasdaq: TPC) It recently completed its business combination with BlackRock Capital Investment Corporation, which was previously a separate, publicly traded business development firm.

BDC announced that it will reduce its management fees, which I believe It can lead to an increase in dividends as well. BlackRock TCP Capital also comfortably covered its dividend with net investment income in the first quarter and the stock is still selling for a discount to net asset value.

I believe BlackRock TCP Capital has rerated post potential merger as the company sorts out some of its remaining credit issues.

My evaluation history

My Hold stock rating for BlackRock TCP Capital stock as of January 2024 was supported by relatively good dividend coverage, which was offset by a heavy focus on variable rate loans.

Focus on the variable rate in particular This was a turn-off to me at the time, primarily because the consensus that had emerged showed that the central bank would cut short-term interest rates in the near term.

Variable rate BDCs like TCPC still have attractive earnings prospects in a high interest rate environment (which is driven by the central bank’s reluctance to cut interest rates at the moment).

Considering that the merger between BlackRock TCP Capital and BlackRock Capital Investment is completed in Q1 2024, I think the value proposition is compelling.

Review the portfolio and change the management fee structure

BlackRock TCP Capital and BlackRock Capital Investment combined their portfolios in a merger deal in March 2024, resulting in a jump in the value of TCPC’s portfolio in the first quarter of 2024. In the first quarter, BlackRock TCP Capital’s total portfolio value was $2.1 billion, compared to the value of its investment In the fourth quarter of 2023, it reached 1.7 billion US dollars.

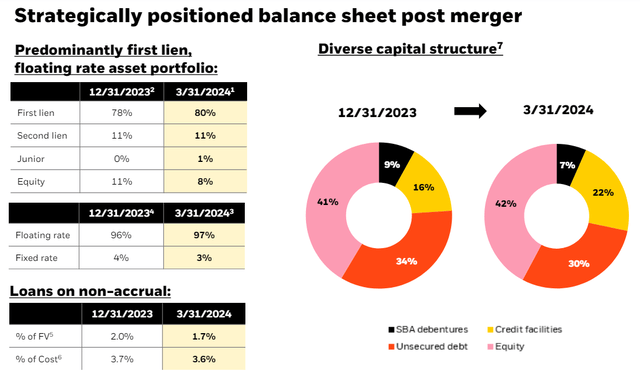

BlackRock TCP Capital, following the transaction, remains a leading business development firm focused on secured debt and has a significant investment in First Liens.

As of March 31, 2024, TCPC had 80% first liens and 11% second liens. Other investments of the recently combined business development company include equity (8%) and junior debt (1%).

Post-merger balance sheet (BlackRock TCP Capital)

As part of the merger agreement, BlackRock TCP Capital agreed to reduce its management fee from 1.50% to 1.25% (for assets equal to or less than 200% of TCPC’s net asset value), allowing BDC, in theory, to return a higher amount. The percentage of net investment income to shareholders going forward. I looked a little more into the benefits of the merger in my article about BlackRock Capital Investment.

BCIC (BlackRock TCP Capital) merger completed

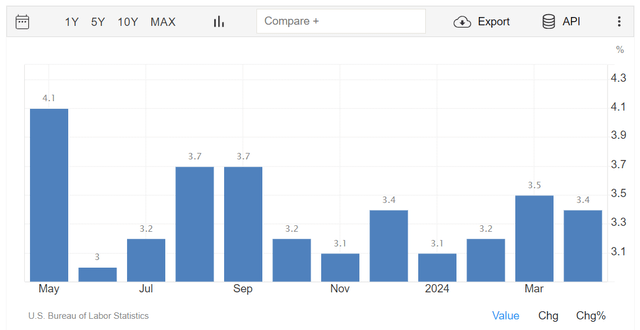

The return of inflation supports the setting of the TCPC’s variable interest rate

Inflation is not slowing down as quickly as expected, creating a favorable environment for BlackRock TCP Capital. The inflation rate rose by 3.4% last month, after rising by 3.5% in the previous month.

Inflation (U.S. Bureau of Labor Statistics)

In January, I expressed concerns about headwinds impacting net investment income growth due to the company’s significant investments in non-fixed rate loans. The BDC currently has 97% exposure to variable interest rates and I believe, contrary to my previous estimate, that the variable rate BDC deals with a more accommodating central bank.

Of course, higher long-term interest rates are poised to support BlackRock TCP Capital’s dividend coverage, which is already looking good.

Reasonable excess profit coverage, and the possibility of increasing profits after the merger

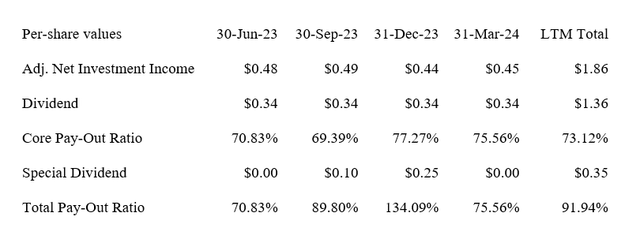

BlackRock TCP Capital has a strong history of consistently outperforming its dividend through adjusted net investment income. In Q1 2024, TCPC earned $0.45 per share in adjusted net investment income, which easily exceeded the company’s current dividend of $0.34 per share.

With the merger just completed and BlackRock TCP Capital directing it to reduce management fees, I can certainly see BDC giving shareholders a dividend boost.

From a hedging angle, BlackRock TCP Capital can easily withstand a dividend increase, as it only paid out 76% of net investment income in Q1 2024.

I also expect synergistic effects to emerge, and combined with a strong variable rate position, TCPC is in a great place to see NII growth in 2024.

Earnings (the author created a table using BDC information)

Discount on net asset value

The situation around BlackRock TCP Capital is a bit unique, considering that the business development firm had just merged with BlackRock Capital Investment and that the latter has been dealing with some non-accrual issues. TCPC had a non-accrual ratio of 1.7% as of March 31, 2024 (debt investments in five portfolio companies were on a non-accrual basis, including one carried over from BlackRock Capital Investment).

In the previous quarter, 2.0% of loans were on a non-accrual basis (representing debt investments in four investment companies). Longer term, I think TCPC could probably re-rate to NAV ($11.14 as of March 31, 2024) if BlackRock TCP Capital resolves some of its outstanding credit issues and lowers its nonaccrual ratio (while maintaining excellent dividend coverage).

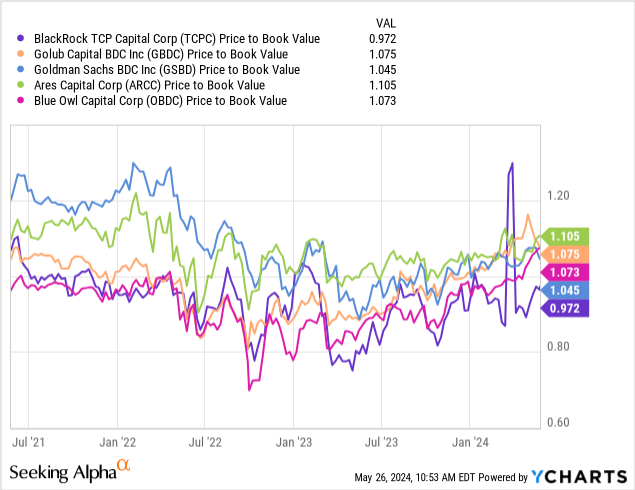

TCPC is currently selling at a 3% discount to net asset value, and that discount may disappear if BDC convinces passive income investors of its post-merger performance.

Other business development companies including Golub Capital BDC (GBDC), Blue Owl Capital (OBDC), Goldman Sachs BDC (GBDC) or Ares Capital Corp (ARCC) They are better understood, have longer track records or lower non-accrual ratios, and therefore sell for higher NAV premiums.

Why your investment thesis may be disappointing

A weaker outlook for net investment income growth in a bearish rate environment will work against BlackRock TCP Capital as the company is exposed to a 97% variable interest rate as of the end of Q1 2024. Deteriorating loan quality is also a potential issue, but I don’t see any specific reason for concern. about it so far.

deductive

BlackRock TCP Capital is promising to grow the business post-merger, with management saying it will reduce its management fees and the portfolio remaining heavily concentrated in First Liens.

Coupled with a positive outlook for interest rates (the central bank is not backing down to push for rate cuts), BlackRock TCP Capital is well positioned to benefit from the current interest rate environment.

The dividend payout ratio looks strong, and I wouldn’t be surprised if the business development company raises its regular dividend as a thank you to shareholders after a successful merger deal.

The discount to book value, while small, complements BlackRock TCP Capital’s value proposition.