Blue Bird Soars as Funding for School Bus Replacement Growth, Starts Buying (NASDAQ:BLBD)

FamVeld/iStock via Getty Images

BLBD’s investment thesis remains strong, thanks to the moat in the school bus market

Blue Bird Company (Nasdaq:PLPD) is the new small-cap stock that has enjoyed an astronomical ride in stock price appreciation so far, thanks to pent-up demand for replacement school buses after several delays due to the COVID-19 pandemic and global supply chain issues.

This is also supported by the company’s strategic offerings across electric and low-emission school buses, capitalizing on the huge electrification trend over the next decade, especially since more than 60% of its sales are non-diesel school buses compared to its competitors’ around 20%. %.

Readers should also note that BLBD’s vertically integrated operations across manufacturing/assembly and distribution/dealer networks in the UCAN region, aided by its core partnership with over 10,000 school districts and 3.4,000 independent school bus owner-operators, further underscore its goal In the school bus market with a high barrier to entry.

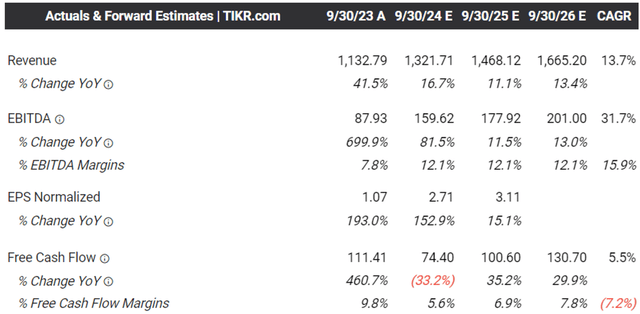

These developments directly contributed to BLBD’s double-digit earnings per share in Q2 2024, with revenue of $345.9 million (+8.8% QoQ/+15.3% YoY) and adjusted EPS of $0.79 (-13.1% QoQ). QoQ/+259% YoY).

Most of the tailwinds were attributable to the increase in units sold at 2.25K (+125 units qoq/-50 yoy) and higher average prices at $153.73k (+2.5% qoq/+17.9% yoy YoY/+66.2% from FY19 averages of $92.48K), implying consumers are willing to pay an increased premium now.

Higher prices during the pandemic clearly worked as intended in the face of higher inflationary pressures, as observed in BLBD’s expanding gross profit margin of 18.3% in the latest quarter (-1.7 points QoQ / +6.5 points YoY / + ) 5.3 from FY19 levels of 13%), with quarter-on-quarter variations attributable to ongoing inflationary pressures and changes in product/channel mix.

This is in addition to limited operating expenses of $27.57 million (+7.6% QoQ/+18.8% YoY) against accelerated overall growth, expanding operating margins to 10.4% (-1.5 points QoQ/+ 6.3) YoY / +6.1 from FY19 levels of 4.3%.

While manufacturing companies typically post lower margins, as noted in “average growth in the past five years,” we believe BLBD’s management has performed admirably despite the challenging times, with higher prices likely to lead to further expansions in margins. Profit coming.

Why a growing backlog led to the release of management’s FY2024 guidance and consensus to raise forward estimates

At the same time, we should also remind readers that BLBD’s growing backlog of 5.9K units (+1.3K units qoq/+0.2k yoy) carries cumulative sales price increases since 2021, with another Prices of +$2.5K per bus are expected for orders after April 1, 2024.

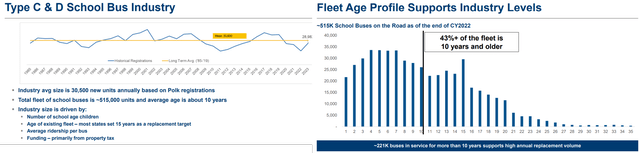

The old school bus fleet in the UCAN area

BLBD

At the same time, we believe there are still significant tailwinds in the medium term, thanks to the school bus fleet profile aging an average of twelve years (as of 2024) versus the typical replacement cycle of every fifteen years, based on ~515K Unit on the road

This comes in addition to new funding for heavy-duty electric vehicles/buses, as the US government looks to replace many of its current school buses from those that use internal combustion engines to electric/low-emission platforms to meet “stricter emissions.” The standards go into effect in 2027.”

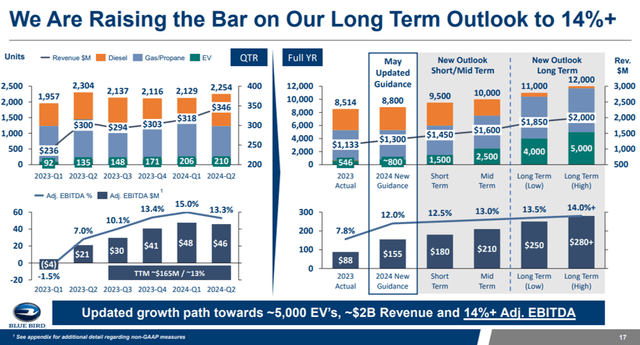

High growth targets for BLBD

BLBD

As a result of these developments, it is undeniable that BLBD is likely to achieve its bullish internal growth targets as presented in its Q2 2024 earnings call.

This was further validated by management’s elevated guidance for fiscal 2024, with revenue of $1.3 billion (+15% YoY) and EBITDA of $155 million (+76.2% YoY) at the midpoint. , up from original guidance of $1.15 billion (+1.7% y/y) and $85 million (-3.3% y/y) given at our September 2023 Investor Day presentation, thanks to increased growth in its manufacturing capacity and expansion of Backlog.

Consensus future estimates

Taker station

As a result of the improved outlook for its medium-term performance, we can understand why the consensus raised their forward estimates with BLBD expected to achieve top/bottom CAGR growth of +13.7%/+31.7% until FY2026.

This compares to historical growth of +2.8%/-1.3% between FY16 and FY2023.

Despite extensive capex/production facility upgrades to meet its annual manufacturing target of 12,000 buses, BLBD also provided relatively promising FY2024 free cash flow guidance of $75 million (-38% YoY), implying its ability to reduce… Its size is constantly moving the balance sheet forward.

For context, management actually reported a healthier balance sheet last quarter, with long-term debt down $97.32 million (-22.6% y/y) and cash/equivalents rising to $93.09 million (+17.8% y/y), With the promising increase in free cash flow generation likely to increase funding for future growth investments.

So, is BLBD stock a buy?Sell, or hold?

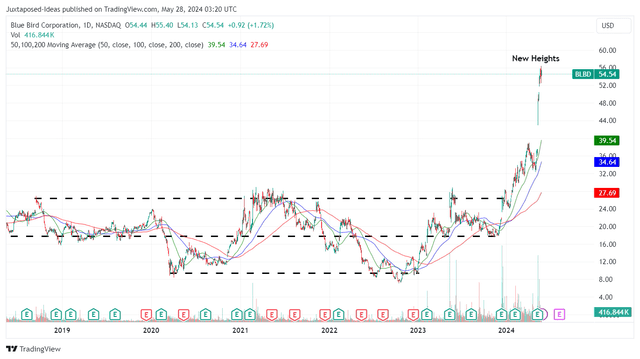

BLBD 5Y stock price

Trading offer

Currently, BLBD is already up +45.2% since its last earnings announcement, while moving away from its 50/100/200 day moving averages.

BLBD Reviews

Seeking alpha

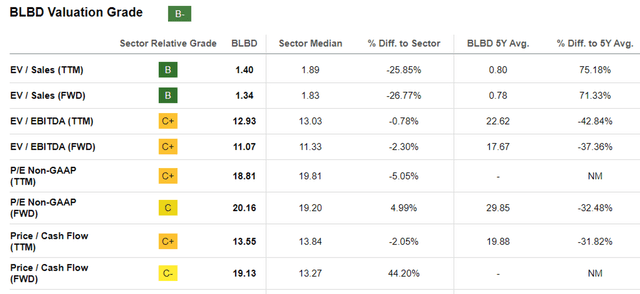

At the same time, we can understand why the market has temporarily given BLBD outstanding FWD EV/EBITDA ratings of 11.07x and FWD P/E ratings of 20.16x, compared to the 1-year average of 9.04x/16.80x and the 3Y pre-pandemic average. 7.87x/11.87x respectively.

Even when compared to its direct competitors, such as Thomas Built Bus, a subsidiary of Daimler Trucks North America (OTCPK:DTRUY) at 7.86x/7.99x and IC Bus, a subsidiary of Traton SE (OTCPK:TRATY) at 6.03x/4.69x. BLBD is clearly not cheap here.

However, with BLBD’s cap/net growth forecast at +13.7%/+31.7% through FY2026 far exceeding that of DTRUY at +3.7%/+5.4% and TRATY at +3.5%/+0.5%, the premium appears to be The FWD EV/EBITDA valuations of 11.07x assigned to the former are justified at the moment, largely supported by the growing backlog and price increases to date.

Based on BLBD management’s FY2024 adjusted EBITDA guidance of $155M at the midpoint (+76.3% YoY) and latest share count of 33.07M, we are looking at EBITDA per share of 4.68 USD (+72.6% y/y).

Combined with FWD EV/EBITDA valuations of 11.07x, it’s clear that BLBD is trading close to our fair value estimate of $51.80.

Based on a similar calculation based on consensus FY2026 EBITDA estimates of $201 million and resulting EBITDA per share of $6.07, there appears to be excellent upside potential of +23.2%. For our long term price target of $67.20 as well.

As a result of the relatively attractive risk-reward ratio, we have initiated a Buy rating for BLBD, although there is no specific entry point since it is based on retail investors’ dollar cost averaging and risk appetite.

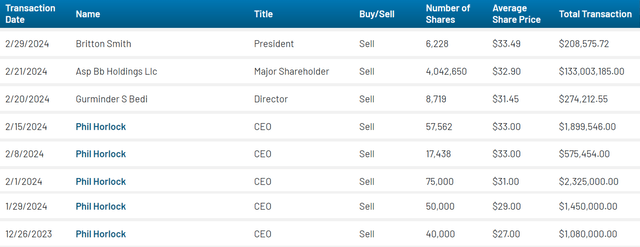

BLBD Insider Selling

Market win

It goes without saying that as a penny stock with a small float, there may be near-term volatility in BLBD’s share prices, exacerbated by the extreme rally and massive insider selling to date, with management likely cashing in on some of its long-term operations. -Term stock options.

With the stock already charting new highs at the time of writing, interested investors may want to monitor its movement for a little longer before adding a moderate bounce to improve the margin of safety.

At the same time, while BLBD has reported a growing backlog, persistently high prices may put its future bookings at risk, with its region/owner-operator partners likely to diversify their partnerships with competitors to save costs. As a result, interested investors may want to continue monitoring this aspect moving forward.