petekarici/iStock Unreleased via Getty Images

As the stock market continues to show resilience at all-time highs, I have continued to warn of incredibly high valuations and in turn take safety measures in my own portfolio to protect against any broad downward movement.

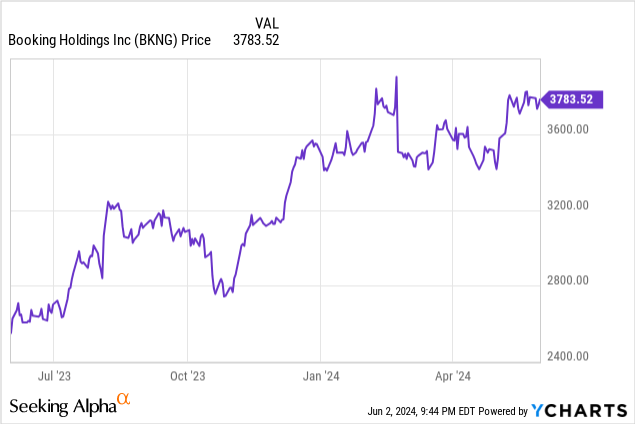

I have one share My portfolio has been seriously downsized which is Booking Holdings (Nasdaq: PKNG). The travel giant has had massive outperformance, especially post-pandemic — with the stock more than doubling from late 2022 to date. But gains have stagnated this year to “only” high single digits, while the S&P 500 posted gains in the mid-teens. In my view, Booking will continue to trade sideways and will disappoint further from here.

Reservations are very expensive to keep

I last wrote a neutral opinion on Booking in March, when the stock was trading at around $3,600. I traded it Beyond the name as a short-term play, but now with the hold extending towards the ~$3800 level again, and after printing Q1 earnings that showed, to me, mostly disappointing metrics, I am now exiting my position and downgrading the hold rating to bearish.

Now, I’m still a long-term deal with the travel industry and especially OTA giants in general. I continue to believe travel demand will continue to be strong as more and more wallet share of discretionary spending goes toward experiences and travel. But my pick in this space is Expedia (EXPE): Although execution for Expedia was more choppy as the company noted weak Vrbo bookings in the first quarter, there’s no doubt that Expedia is winning on the valuation front.

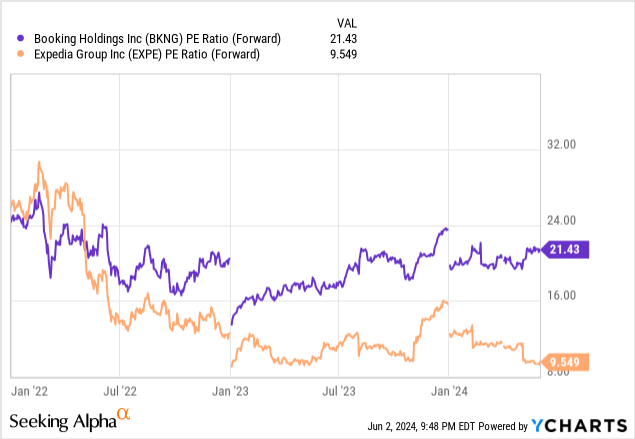

But booking is strikingly expensive. It’s ~21x Forward P/E It falls at nearly double the Expedia rating. It’s worth noting that Booking’s market cap is roughly $128 billion versus Expedia’s $15 billion, despite the fact that on a gross bookings basis, Booking is only about twice the size of its competitors.

The simpler question to ask is how much of a premium should we be willing to pay for quality: and I’m not willing to pay that much.

In addition to valuation risks, there are also a number of key risks related to booking:

- The mix of loyalty programs may not seem attractive compared to Expedia’s One Key program. While both Genius and One Key offer tier-based benefits, only One Key offers ~2% cash back per booking. We also note that while Expedia has consolidated rewards for all of its programs under One Key, the other major Booking site, Priceline, uses a completely different rewards program called Priceline VIP.

- The lightning rod of criticism and price competition. Hotels have long complained about the exorbitant commissions paid to online travel agencies. In a time of heightened sensitivity to commissions that were once thought to be untouchable (just look at what’s happening to real estate commissions with the recent ruling against NAR), the business model of online travel agencies may soon be upended. Also note that Booking is mired in a number of regulatory entanglements, including with the Spanish government, which fined the company $530 million.

- A slowdown in bookings may result in multiple booking valuation pressure. The last two summers saw very strong travel demand as people went on holiday post-coronavirus, but does this mean demand has been pushed forward from future seasons? First-quarter bookings slowed sharply relative to reservations, which could be a precursor to a weaker summer.

For me, now is the perfect time to make gains on Booking while it sits near its YTD highs at around $3,800. I’m parsing my position here and recommending investors do the same.

Download Q1

Let’s now review Booking’s latest quarterly results in more detail. Key highlights from the first quarter are presented below:

Book the main directions (Book the first quarter earnings release)

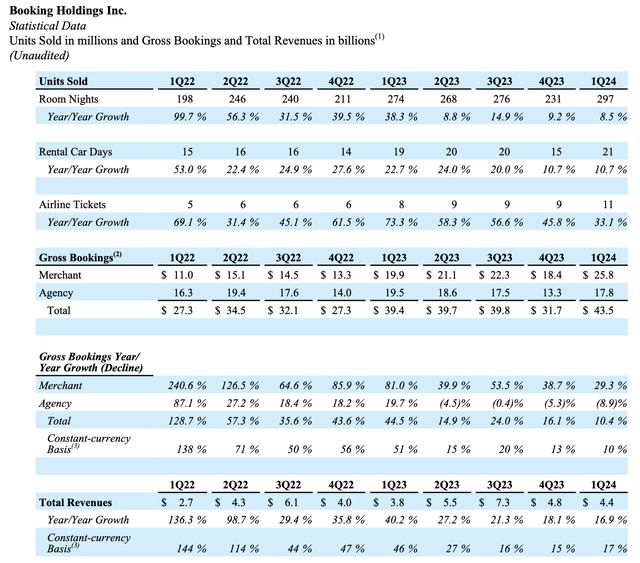

Across the board, the theme was slowing bookings – despite accelerating revenues. Revenue grew 17% year over year on a constant currency basis to $4.42 billion, beating Wall Street expectations of $4.26 billion. But as a reminder here, Booking recognizes revenue when flights and stays are completed — which means revenue is entirely based on prior bookings, with many travelers booking their stays well in advance of this quarter. We’ve seen strong bookings performance in 2H FY23 which seems to be translating into flights here: but new bookings aren’t coming in at quite the same rate.

Total bookings of $43.5 billion in the quarter slowed to 10% year-over-year constant currency growth, down from 13% year-over-year in Q4 and 20% year-over-year in Q3.

As a reminder to new investors in Booking, like Expedia, the company has the lion’s share of bookings from hotels. Booking has placed a strong focus on selling packaged travel to boost revenues from airfare and car rentals, which are seeing stronger growth. CEO Glenn Vogel’s remarks on the first quarter earnings call:

Connected transactions represented a high-single-digit percentage of Booking.com’s total transactions in the first quarter. It’s great to see more of our travelers choosing to book connected transactions. We believe that by providing greater value and a better overall experience to these travelers, they may choose to book more trips with us and be more likely to book directly with us in the future. Flight is the most frequently booked sector in a connecting transaction outside of accommodation. It is an important component of many of the trips our travelers book.

In the first quarter, flight tickets booked on our platforms rose 33% year over year, primarily driven by growth in Booking.com’s travel offerings. We continue to see a good number of new customers to Booking.com through the aviation sector, and we are encouraged by the rate at which these and returning customers are seeing the value of other services on our platform (…)

Beyond flights and accommodation, we are seeing strong growth from car rentals and attraction bookings that are part of a connected transaction.”

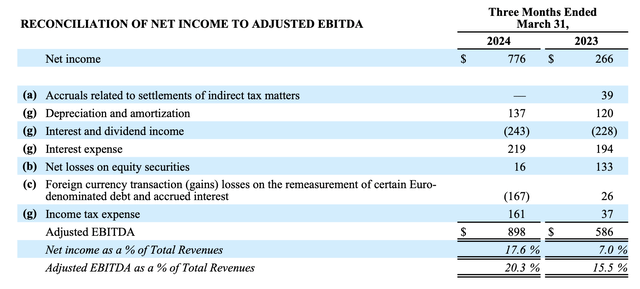

We’ll admit that on the bright side, Booking is still seeing healthy profitability, with adjusted EBITDA up 53% year over year to $898 million in the quarter. Adjusted EBITDA margins jumped 480 basis points year over year to 20.3%.

Book Adjusted EBITDA (Book the first quarter earnings release)

Main sockets

For me, the combination of high valuation plus slowing bookings is the impetus for me to de-risk my portfolio and exit my short position in Booking. While I still have confidence in the growth of the OTA industry, I would rather support Expedia with its much lower valuation and accept some execution risk along the way than continue to hold Booking at an extraordinary valuation premium.