Blackread/E+ via Getty Images

American Auto Parts, Inc (Nasdaq: MPAA) has seen its stock prices decline over the past few years, mainly due to a spike in interest expenses on newly added debt. The price is down from around $20 in November 2022 and just over $10 in February 2024 turned most investors against ownership. I can’t really blame them.

StockCharts.com – America’s Auto Parts, 24 months of daily price and volume changes

According to the Motorcar Parts of America website, the company is a leader in remanufacturing/supplying best-in-class aftermarket and undercarriage components, with more than 4,700 employees at 13 locations across 7 countries. Thousands of individual products for virtually every vehicle are sold on- and off-highway to 7,700 auto parts retailers and distributors. Main products include alternators, starters, wheel bearings and axle assemblies, brake calipers, brake master cylinders, brake boosters, rotors, brake pads and turbochargers. In addition, the company designs and It manufactures testing solutions for performance, endurance and testing of electric motors, inverters, alternators and starters as well as belt drive alternators.

Auto Parts of America – May Investor Presentation

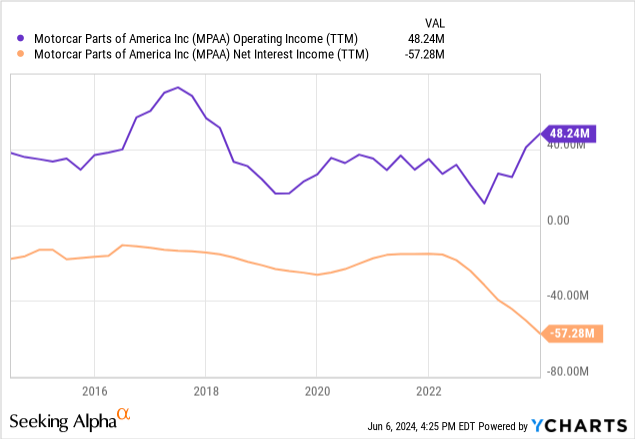

Some good news is that the actual business is performing very well with operating income hitting a 5-year high of $48 million over the last 12 months (partly due to older cars remaining on the road since the pandemic). With lower debt levels, cash earnings per share are expected to improve rapidly starting later in calendar 2024.

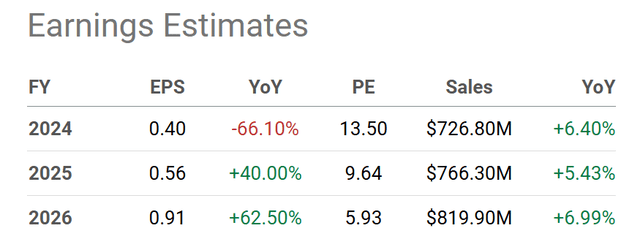

Find Alpha Table – Auto Parts of America, Analyst Estimates for 2024-26, released June 6, 2024

My bullish conclusion is: If we get a soft landing with low interest rates through 2025, the total “enterprise value” of equity plus debt is very low. In fact, the MPAA’s valuation is priced as if we are in a serious recession, as we were in late 2008 and early 2009. To me, this deep value proposition leaves plenty of room for stock prices to rise, given that the economy is not collapsing anytime soon. Let me explain.

Debt problem

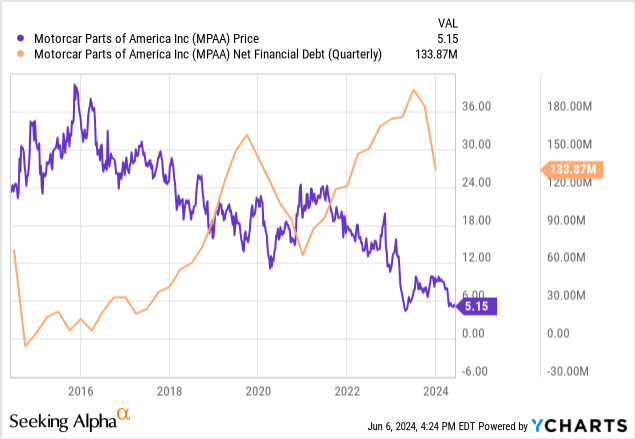

Below is a graph of the inverse relationship between rising financial debt (minus cash, excluding leases and other long-term contract obligations amounting to an additional $280 million at the end of December) and declining stock prices since 2014. The second graph compares operating income at what levels have remained Fairly flat at around $40 million (before interest costs are factored into the equation), while net interest expense has swelled with the jump in borrowing rates since early 2016 (plus contract fees). Note that when Motorcar Parts had almost no debt in 2015-2016, the stock was worth over $30.

YCharts – Auto Parts of America, High Debt Levels vs. Low Stock Price, 10 Years YCharts – Auto Parts of America, Operating Income vs. Net Interest Income/Expense, 10 Years

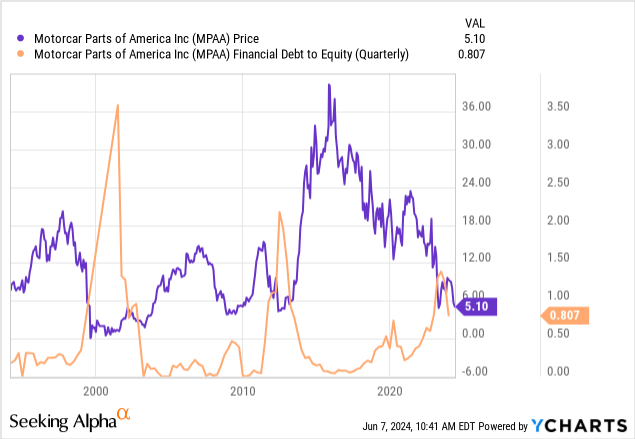

Another way to look at the situation is how the stock price has performed since 1994 as a function of the debt-to-equity reading. Again, when debt is high, stock prices fall. So, if management is committed to future investment gains for shareholders, debt reduction is the name of the game.

YCharts – Auto Parts of America, Debt to Equity, since 1994

Evaluating recession-like trades

With so many moving parts in financial engineering and leverage, including a large one-time charge to make an accounting change in fiscal 2024, my view is that the best way to assess a company’s value is by its total acquisition value including both debt. and total equity. Calculating enterprise value (EV) is what I’m reviewing today.

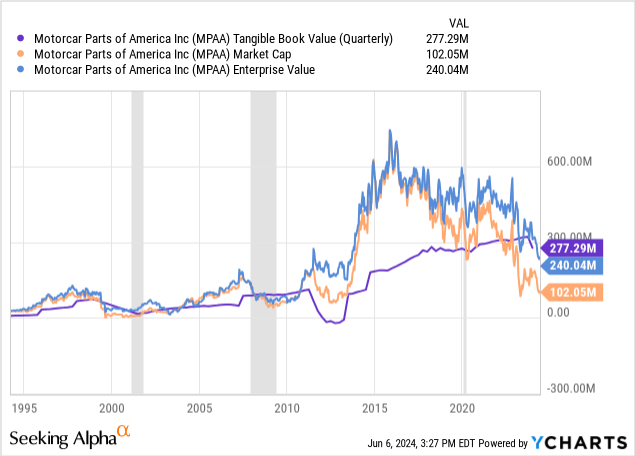

When we compare equity market value or net enterprise value to tangible book value (net fixed assets), you can see that Wall Street is placing an unusual discount on the business versus normal cost/depreciation accounting. We can say that today’s discount is no less massive than the depths of the Great Recession of 2008-2009 or the dot-com recession of 2000-2002. I can make a great buy case from this data set alone.

YCharts – US Auto Parts, Tangible Business Value vs. Market Cap and Enterprise Value, Since 1994

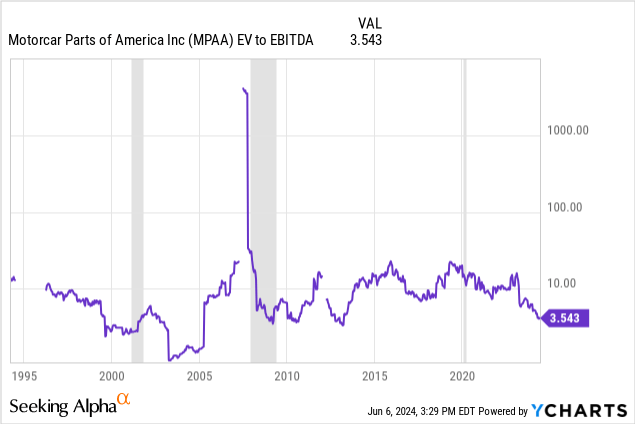

Perhaps better evidence of a long-term bottom can be found in EBITDA and sales-to-enterprise value ratios. The EV of EBITDA statistics over the past 30 years explains that the MPAA is a great buy (assuming the Great Recession is avoided). The current multiple of 3.5x is the lowest since 2013.

YCharts – America’s Auto Parts, From EV to EBITDA, Since 1994, Recession Shaded

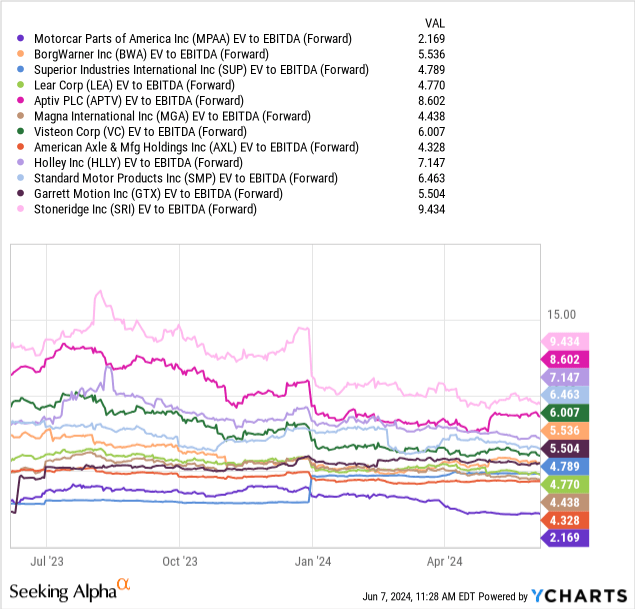

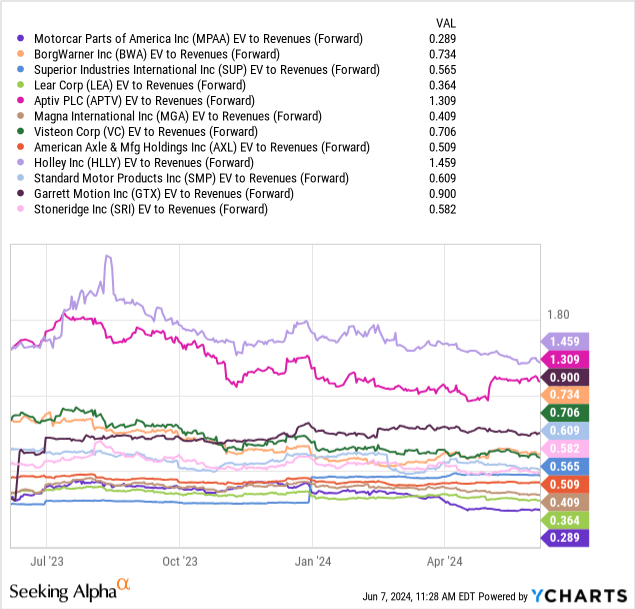

Next, when we compare/contrast Motorcar Parts of America’s EBITDA valuation to its peers and competitors in the auto parts industry, the stock really stands out as a bargain. The 2.1x estimate is well below the industry average of 5.5x (a 60% discount in fact), and a much better deal than it was a year ago. My peer screening group includes BorgWarner (boa), Superior industries (sip), ler (Leah) Aptiv plc (IPTV), Magna International (MGA), vistion (unlock), American axis (Axel), Holly (May I), Standard motor products (SMP), Garrett Motion (GTX), and Stoneridge (secret).

YCharts – Auto Parts of America vs. Industry Peers, EV Forward Estimated EBITDA, 1-Year

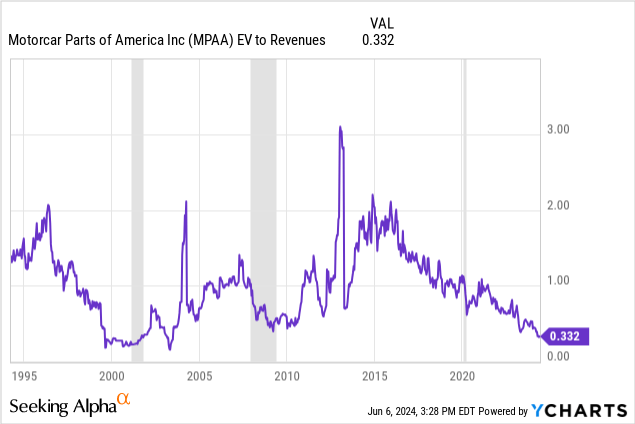

As for the EV to revenue stats, the bullish setting continues to impress. The trailing MPAA figure of 0.33x is actually lower than the significant stock price bottom in 2009. Only a few years including 1999, 2000, 2001 and several months during 2003 provide a more astute assessment of sales over three decades.

YCharts – America’s Auto Parts, Electric Vehicle Revenues, Since 1994, Recession Shaded

Reviewing peer assessments of projected sales for the rest of 2024, the vehicle revenue to forward revenue ratio of 0.29x is roughly half the industry average of 0.6x.

YCharts – Auto Parts of America vs. Industry Peers, EV Forward Estimated Sales, 1 Year

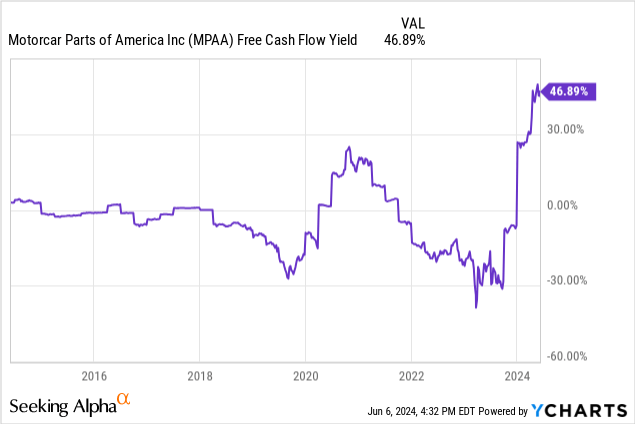

Finally, Wall Street loves free cash flow generation, but not from Motorcar Parts of America. Shouldn’t investors be flocking to FCF’s near-50% yield, the highest in 10 years, on its abnormally low $5 share price?

YCharts – US Auto Parts, Free Cash Flow Yield, 10 Years

Final thoughts

Despite decent fundamental business trends, pessimistic analysts and investors may be overly focused on the MPAA’s debt/interest expenses (which can easily decline over time), worry about the effects of a recession on auto parts demand generally, and only care about printing Negative of one – accounting changes for time.

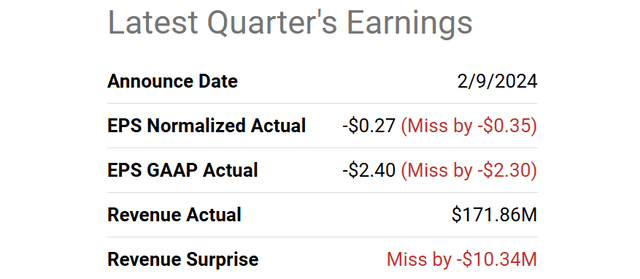

We’ll know more about the health of its operating business on June 11, when the company is due to release its March fourth-quarter earnings. Analyst forecasts call for flat EPS of $0.16 on sales of about $200 million. I will say that it would be difficult to post earnings that were as disappointing as last quarter.

Find Table Alpha – US Auto Parts’ fiscal 2024 third-quarter earnings disappoint

Sure, the auto parts chart is downright ugly. However, the price has maintained the bottom area of $4 in the past year. Indicators of selling fatigue appear in my short-term momentum formulas. However, I cannot guarantee that the final bottom will be reached. Finally, I suggest that the MPAA is a long-term devaluation option, plain and simple.

Recessions and the periods before/after have not been very kind to MPAA investors. This is the main reason to be careful about this name. It is also the next logical excuse for poor stock pricing, after taking excessive use of debt into account.

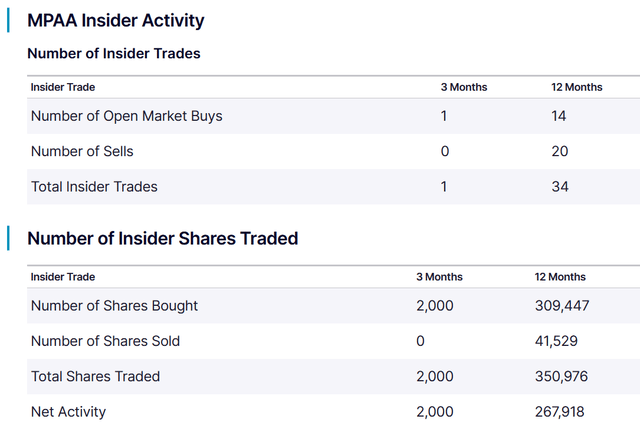

What are other trading risks? MPAA is a smaller group, which means that significant changes in operating fortunes will be noticed by management and insiders before the general investing public. In this regard, I consider the moderate level of insider buying activity a positive. I would remind readers that smaller companies tend to have more volatile stock prices and can experience meaningless short-term fluctuations. This is often the result of one hedge fund or investor taking/liquidating a major position.

Nasdaq.com – US Auto Parts, insider trading activity, June 7, 2024

On the upside, I strongly believe that another auto parts manufacturer would be wise to acquire the company at this low valuation. A takeover offer of up to $10 per share would be very beneficial to a variety of large players in the industry. The total acquisition value of approximately $350 million, including debt cancellation, will allow a single owner to capture up to $75 million in EBITDA and more than $50 million in operating income before… Tax deduction in 2025.

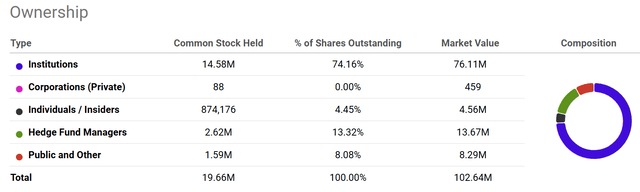

The ownership structure of insiders and management owning less than 5% of outstanding common shares should give any blue-chip acquisition high odds of success, especially an offer price that is nearly double the current price, near 52-week highs.

Find Table Alpha – Auto Parts of America, Shareholder Ownership Distribution, March 2024

When weighing the risks of a recession against the potential rewards in a growing macroeconomic environment, I believe Motorcar Parts of America stock is too cheap to ignore. I rate stock A He buysAnd having a small position. With a market capitalization of about $100 million, the MPAA is a speculative security, which advocates keeping weights on the low side in portfolio construction.

Thanks for reading. Please consider this article as a first step in your due diligence process. It is recommended to consult with an experienced, registered investment advisor before making any trades.