Evening pictures

Investment thesis

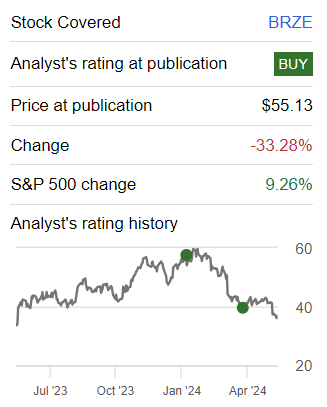

braze (Nasdaq: BRZE), a customer relationship management and messaging platform, saw its shares jump nearly 15% before its market debut as investors breathed a sigh of relief that its results weren’t worse.

But as the dust settles, I’m finding it difficult to stay bullish on this stock. Basically, this is the main problem, BRZE is priced as a long-term growth story, but its growth is fading very quickly.

Why pay 6x forward sales for this unprofitable company, when there is better stock on offer around the same price range? As a result, I move to the margins.

Quick recap

In my previous analysis, this is how I summarized the investment case for BRZE:

Braze’s bullish issue focuses on this company’s rapid progress toward profitability. The bear case looming over the stock is the key question as to whether Braze’s days are the same Is a fast-growing business now in the rearview mirror? Simply put, was Braze just a flash in the pan? Or is there still more juice left in this tank?

Meanwhile, Braze has a very strong balance sheet and operates debt-free. In short, I remain tepidly optimistic on this stock, but I see Braze as needing to improve its growth outlook; Otherwise, this stock is ripe for a sell-off.

The author worked on BRZE

I’ve been bullish on Braze for some time, as the chart above shows. But even though the stock is up about 15%, I’m moving to the sidelines on this.

Braze’s near-term prospects

Braze offers a service that helps businesses talk to their customers in a personalized way through different channels such as emails and app notifications. It’s similar to what companies like Salesforce (CRM) or HubSpot (HUBS) that are rumored to be acquired are doing. Essentially, Braze provides tools for businesses to send personalized messages to their customers, making communication more effective.

Moving forward, Braze’s focus on personalized customer engagement has attracted new clients and notable sales, including Bauer Media Group, Etsy, and Lime, among others.

Furthermore, during the earnings call, Braze pointed to its AI-powered copywriting assistant that aims to boost marketer productivity and create more authentic brand experiences.

However, Braze faces several near-term challenges as well. As a turn investor, I believe the customer adoption curve is the most pressing consideration to evaluate. With that in mind, notice the following numbers for Braze’s overall customer adoption curve.

- Second fiscal quarter 2023: 43% year-on-year

- Third fiscal quarter 2023: 38% year-on-year

- Fourth fiscal quarter 2023: 29% year-on-year

- First fiscal quarter 2024: 24% year-on-year

- Second fiscal quarter 2024: 23% year-on-year

- Third fiscal quarter 2024: 17% year-on-year

- Fourth fiscal quarter 2024: 15% on an annual basis

- First fiscal quarter 2025: 13% year-on-year

The above trend speaks for itself. Then we will discuss its basics.

Braze’s growth rates are expected to be moderate

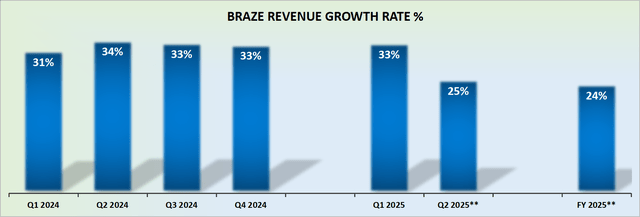

BRZE revenue growth rates

Braze ended fiscal 2024 with 33% year-over-year growth. Now, its guidance for fiscal 2025, although revised higher, indicates a roughly 24% year-over-year increase. This represents a slowdown of 900 basis points in 12 months.

Braze may positively surprise investors and end up with growth rates of around 26% year over year for fiscal 2025. This would still be a 600 basis point slowdown for a software startup seeking a premium on its valuation.

Along these lines, this is what I discussed in my previous analysis:

Naturally, management will strive to be judicious in its guidance. I have no doubt about that. However, there is still a very large gap between the first quarter of the fiscal year and the rest of fiscal 2025.

To put this more concretely, it currently appears that once we get past the first fiscal quarter of 2025, their growth rates will slow significantly. If so, I wonder if this stock is really worth paying attention to?

90 days later, not only are my concerns still present, in fact, they are now more pressing. With these elements in mind, let’s now delve into its evaluation.

BRZE Stock Valuation – 6x sales

As it stands now, investors are looking at rapidly slowing growth rates. Furthermore, its non-GAAP gross margins were compressed by 90 basis points year over year.

BRZE fiscal first quarter 2024

This to me is a concern. I understand slowing growth rates. that’s ok. But I expect to see an improvement in profitability. This is not what we see here.

Does it make sense to pay 6 times the sales for this type of business? It doesn’t make sense to me.

Yes, one can always confirm that Braze operates debt-free, as approximately 14% of its market capitalization consists of cash. However, we’re still looking at at least another 12 months before Braze breaks even with its non-GAAP operating margin.

And then, at that point, what kind of growth rates are investors going to get from Braze? Less than 20% CAGR? I’ve been lukewarmly optimistic about Braze before. But even that was a mistake.

Bottom line

In conclusion, it has become clear that Braze’s near-term prospects appear to be fading fast.

Despite its strong balance sheet and debt-free operations, the current valuation, at 6x sales and non-GAAP gross margin pressure, fails to justify the investment opportunity, especially when compared to other options in the market that I find have more promising prospects. .

So, I made the decision to move away from Braze, knowing that there were better investment opportunities elsewhere.