Richard Drury

Financial bread (New York Stock Exchange: Bahrain Financial Harbor) is a depository bank specializing in consumer loans. The bank differs from some consumer lenders such as OneMain Financial (OMF) who get their money from external debt to depositors. Lender The stock has seen a strong rise in price over the past six months and is currently sitting near a 52-week high. Based on Bread’s current financial performance, I believe further upside in the stock price is likely.

Bahrain Financial Harbor’s first quarter earnings performance

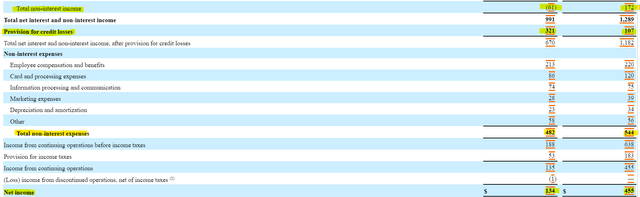

Bread Financial deals with many of the same challenges as other banks where high interest rates hurt the financing expense side and low demand for loans hurts the income side. Interest income decreased slightly in the first quarter compared to the same period last year and interest expense increased by approximately 15%. Ultimately, net interest income (interest income minus interest expense) decreased by $65 million To $1.05 billion. When it comes to non-interest income and expenses, non-interest expenses decreased year over year as the company was able to control labor and overhead expenses very well, but the variance resulting from gains from the sale of assets a year ago resulted in net income of less than $300 million. To 134 million dollars.

10-h seconds 10-h seconds

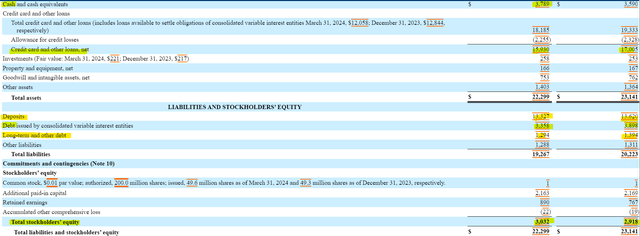

Bread Financial’s balance sheet highlights the lender’s capital structure and what makes it unique. The lender gets more than $13 billion of its $19 billion liabilities from depositors, a cheaper source of funds than external debt, which represents $4.6 billion (down from $5.2 billion at the end of 2023). Bread Financial saw its overall loan portfolio decline by $1.1 billion, but built its cash balance to $3.8 billion and has more than $2.2 billion in provisions for credit losses. Shareholders’ equity in the first quarter rose to more than $3 billion.

10-h seconds

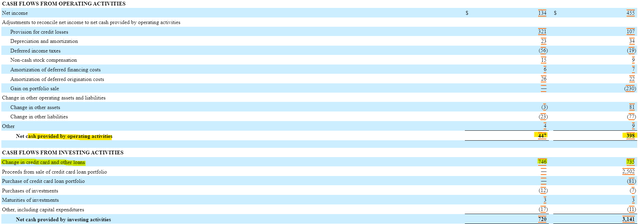

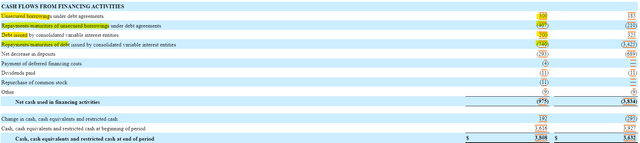

The cash flow statement highlights the company’s use of its cash in the first quarter. During the quarter, Bread generated approximately $1.2 billion from a combination of lead transactions and payments on personal credit loans. Of the $1.2 billion, Bread used $600 million to pay off debt, $300 million to cover a decline in deposits, and $300 million to build its cash balance. While many investors may worry when a bank experiences a decline in lending and deposits, Breed shows it can manage these shifts in liquidity with ease.

10-h seconds 10-h seconds

Navigating the interest rate environment

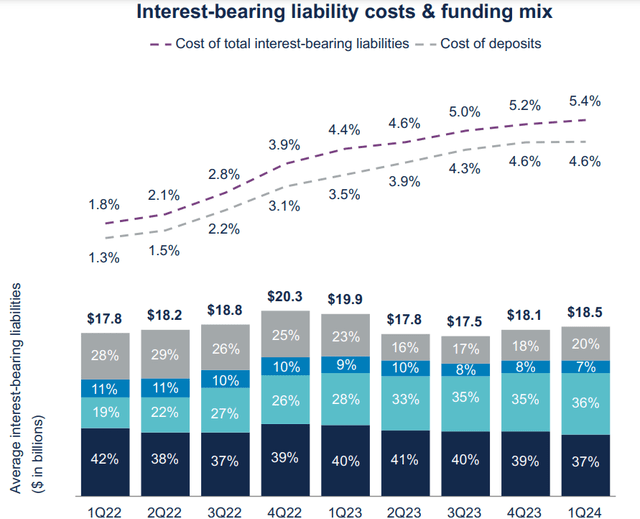

Bread Financial has a somewhat unique position in the banking industry. The company can purchase low-interest expense funds through depositors and make high-interest loans using credit cards and personal loans. Despite the decline in deposits, Bread has been able to compete with the interest rates it offers to depositors and control its total liability costs, which are still less than 5.5%.

View earnings

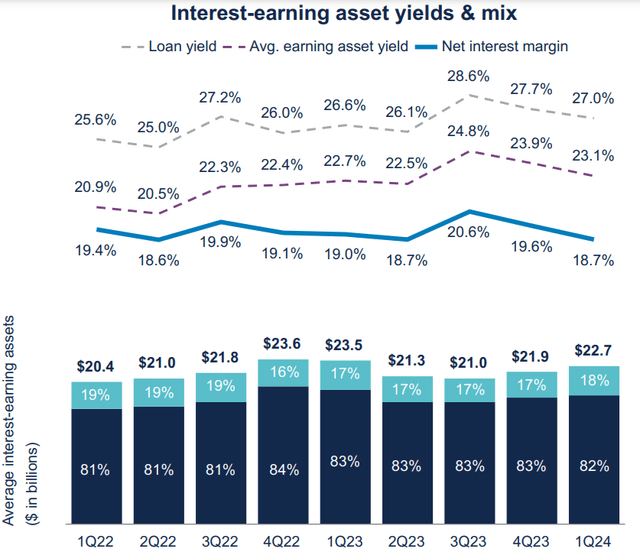

Despite the increase in interest rates, Bread Financial has been able to lend to its clients at fixed interest rates with loan yields rising modestly over the past two years. As a result, the lender was able to maintain stable net interest margin over the same period. Analysts are not concerned about the potential for higher interest rates to impact earnings as they expect Bread Financial’s earnings to rise to $6.47 per share in 2025.

View earnings Seeking alpha

Delinquency and losses are the main risk

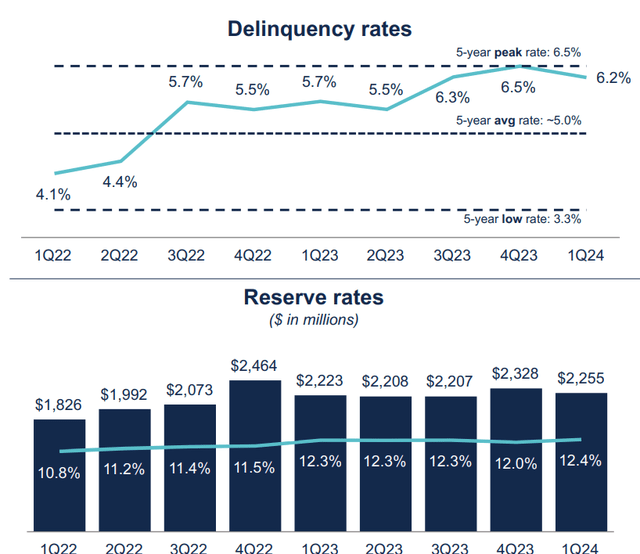

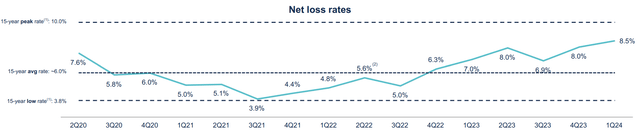

The biggest risk to Bread Financial’s earnings outlook is delinquencies and losses on its loans. When the economy slows and unemployment rates rise, credit cards and consumer loans tend to be the first and hardest-hit lending areas. Bread Financial has had earnings success despite a slow rise in delinquencies to 6.5% at the end of 2023, which eased in the first quarter. Net loss rates continue to rise above their 15-year average, but remain 150 basis points below their 2009 levels.

View earnings View earnings

One indicator that gives some relief to the growing concern about non-performing loans is the analysis of borrowers by credit score. Currently, 56% of Bread Financial loans are made to customers with a credit score above 660, which is considered healthy. Only 17% of the lender’s loans are for customers with credit scores below 600.

10-h seconds

Two ways to take a long position

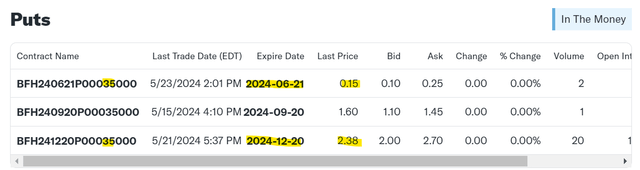

While many investors may be okay jumping right in and buying stocks near the 52-week high, others may be a little more hesitant and want to wait for a pullback. One way to wait and continue to collect income is to sell guaranteed put options for cash. For Bread Financial, guaranteed cash puts are currently being sold at a strike price of $35 per share.

While the June and September options have little to no liquidity, there is some volume in the December options, with a recent trade of $2.38 per share. That’s not bad considering it represents a 5.68% return on the current share price in less than seven months or a 12% annualized return based on the cash that secures the trade.

Yahoo Finance

Conclusion

Bread Financial has been unfazed by interest rate fluctuations over the past two years. The company has been able to achieve strong profits and cash flows while not having to borrow excessively or raise lending rates significantly. The lender easily managed through lower deposits and borrowings in the first quarter by paying down debt and increasing its cash position. The options market also provides an opportunity to reserve a place at a lower price while generating income at the same time. Whichever option investors choose, Bread Financial provides them with a good opportunity to achieve long-term returns.