TZCAPTURES/iStock via Getty Images

introduction

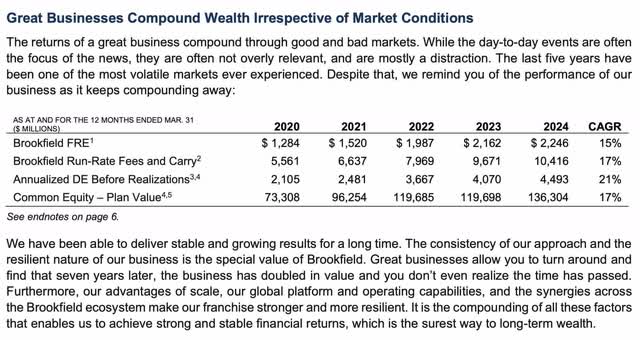

In my February article, Brookfield (New York Stock Exchange: Penn) has important considerations for this. We have new developments since the February article including Q1 2024 numbers. Looking at the 1Q24 letter, we see the value of the plan It has a 4-year CAGR of 17% to reach $136,304 million at the end of March.

Brookfield plan value compound annual growth rate (Message 1Q24)

My thesis is that Brookfield’s valuation continues to increase because they are smart capital specialists.

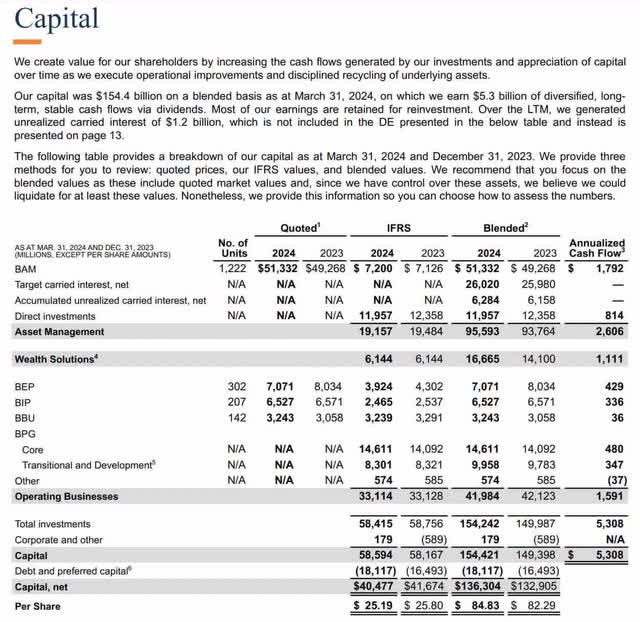

Summary numbers

The additional 1Q 2024 net value of the plan is $136,304 million after deducting $18,117 million of debt and preference from the overall subtotal of $154,421 million. The total plan value of the Asset Management segment is US$95,593 million, representing 62% of the total.

The value of a detailed Brookfield plan (extra 1Q24)

Brookfield Asset Management (“BAM”)

The market has been doing well Recognizing the prowess of Bank Al-Maghrib in allocating capital! Based on the March 28 closing price of $42.02, Brookfield Corporation’s stake of approximately 1,222 million units in BAM is worth just over $51 billion. This is fairly close to management’s sense of value. Looking at BAM’s 1Q24 Supplementarywe have a TTM fee-related earnings (“FRE”) of $2,246 million and a value target of $757 million:

The target interest on capital currently invested is $1.5 billion annually, and $1.2 billion on capital not yet invested. Total targeted carried interest is $2.6 billion, of which $1.6 billion is in our share, and $757 million net of costs.

BAM uses a multiplier of 25-35x for FRE and 10x for target carry. As such, their valuation range is from $56,150 to $78,610 million for the FRE plus $7,570 million for the target load so that the total valuation range is from $63,720 to $86,180 million which comes out to $39 to $53 per Shares of BAM stock based on 1,632.8 million shares outstanding in Q1 2024. Supplemental.

Prior interest

Brookfield has a long history of allocating capital to strong investments so that performance is high and the interest carried is rewarding. Brookfield Corporation gets one-third of the new load from BAM plus all of the old load. Brookfield Corporation estimates its target at $26,020 million and also has $6,284 million of backlog of unrealized carry.

Wealth Solutions – Insurance

Insurance companies collect payments from customers up front, and the payments are invested while claims come in later. Invested payments are called float and float is more valuable when interest rates are higher. The 1Q24 letter emphasizes how adept Brookfield is at allocating capital/float rather than being expert at underwriting (emphasis added):

Our investment experience. Not making money from insurance. Therefore, we have identified and focused on segments of the market from which we can obtain low-risk, long-term obligations (not unlike the long-term debt we use in our real assets business), and then apply our ability to create and underwrite attractive risk-adjusted investment opportunities to maximize returns. The output is a long-term, highly predictable earnings stream that resembles an annuity and is very similar to the cash flows generated by other assets we own.And our asset management business.

The Q1 ’24 letter goes on to say that they expect to do well in this area because the number of American adults ages 65 and older is expected to grow to more than 80 million in the next 25 years. Additionally, long-term interest rates looked exceptionally low in 2020, and Brookfield was right to believe they would eventually rise. Brookfield is now one of the largest annuity providers in the United States. They now hold the top three positions in the life and annuities market in the United States. This business is a natural hedge to their real estate business.

According to a footnote in the Q1 2024 supplement, management is using a 15x multiple on annual distributable earnings of $1,111 million in order to value the Wealth Solutions business at $16,665 million. With the closing of the AEL deal in May, the sector now has more than $100 billion in total assets.

Brookfield Renewable Energy (BEPC) (BEP)

Brookfield Corporation owns approximately 302 million BEP units for more than $7 billion based on a March 28 BEP price of $23.23. Since that time, BEP has announced a major solar and wind deal with Microsoft (MSFT) and BEP’s stock price has risen 14% to $26.53 as of May 29.

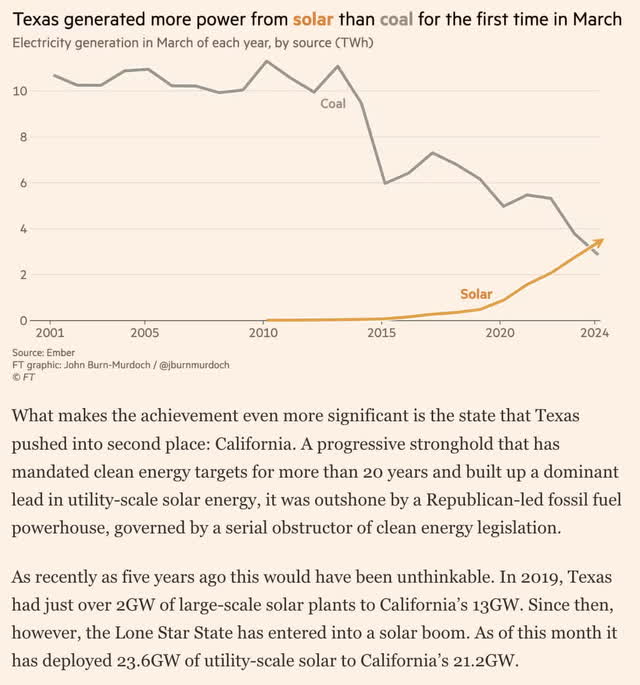

BEP has always been smart in deploying capital, focusing on hydropower until the economics of solar and wind improved. The Financial Times confirms the improved economics of solar energy:

Perhaps the most clear sign yet that the economy has transformed climate change politics in Texas came last year, when several proposed legislative bills aimed at making it more difficult to build new solar and wind facilities failed to pass votes.

Due to the improving economics of solar and the ease of building renewable energy projects in Texas, the state saw more solar capacity than coal in March, according to the Financial Times. The BEP was prescient years ago when they said this kind of thing would eventually happen.

Texas Solar (Financial Times)

evaluation

The upper end of my BN valuation range is what we saw above from management – $85 per share when rounded to the nearest dollar. My low valuation range is 33% below this – $57 per share for a range of $57 to $85 per share. May 29 BN stock price is $42 and I think it is a buy for long term investors.

Disclaimer: Any material contained in this article should not be relied upon as a formal investment recommendation. Never buy a stock without doing your own thorough research.