Matteo Colombo

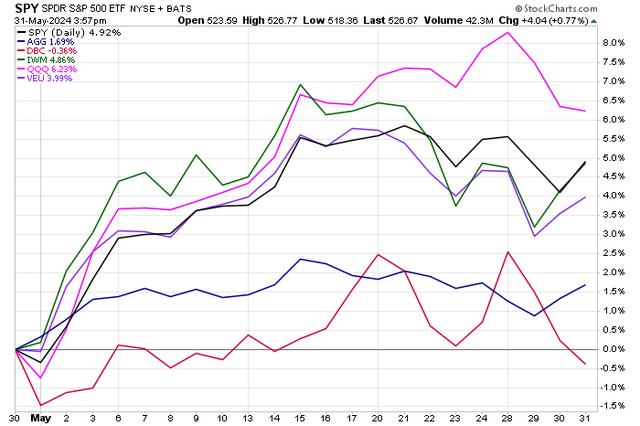

Stocks managed a rebound in May after thatHuge losses in April. althoug Standard & Poor’s 500 The SP500 index gave up some of its gains over the past week, rising by about 5% during the month. Relative strength was seen in Nasdaq stocks – The Invesco QQQ Trust ETF (QQQ) is up better than 6%. In small-cap territory, the iShares Russell 2000 ETF (IWM) rose nearly 5%, roughly on par with the SPX.

Overseas, the Vanguard FTSE All-World Ex-US ETF (VEU) performed well, rising 4% with the US Dollar Index generally flat. Action was seen in emerging markets, specifically China, which jumped significantly at the start of May, but then endured a quick 10% correction, putting pressure on the iShares Emerging Markets ETF (EEM). However, developed markets outside the US performed well amid strength on European bourses and among Japanese stocks.

As for the bond market, returns It fluctuated around the 4.5% mark on 10-year US Treasuries. The Fed’s rhetoric was loud during the month, and inflation data was generally about what economists were expecting, whether or not it was Consumer price index for April Or PCE datasets. Finally, the iShares Aggregate Bond Index ETF (AGG) posted a total return of about 1.7%. Commodities as a whole were roughly flat in May, as measured by the Invesco DB Traded Commodity Index (DBC) tracker.

Stocks and bonds rise in May

Stockcharts.com

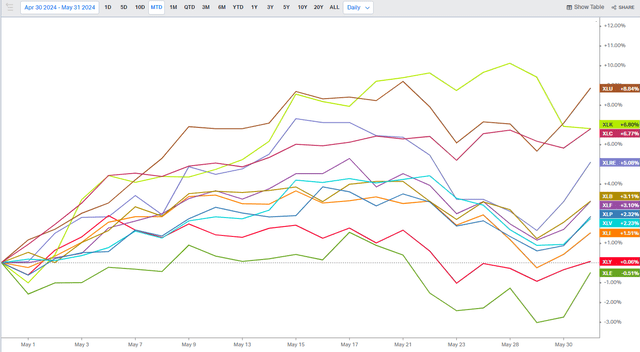

Sector-wise, utilities (XLU) have been the shining star. the Energy production group It has become the latest AI darling, stealing the crown from some tech plays. On the other hand, Energy (XLE) and Consumer Choice (XLY) appeared in the back. Oil (CL1:COM) prices have risen at times over the past few weeks, but still ended May at less than $80 per barrel for spot-month WTI. Gasoline futures settled near three-month lows, so there should be some relief at the pump for summer travelers.

Will this help spending activity in the coming months? It’s hard to say, but consumer stocks have struggled and been in the spotlight for good and bad reasons during earnings season. We’ve seen a lot of blowouts and explosions among small and mid-sized retailers in the reporting period. Tech ended May on a whimper, losing about 3% during the back half of the last week of May. This followed Nvidia’s (NVDA) record-breaking first-quarter report, which included a dividend increase, stock buyback announcements and stock split news.

Utilities led the way in May, and energy is negative

TradingView

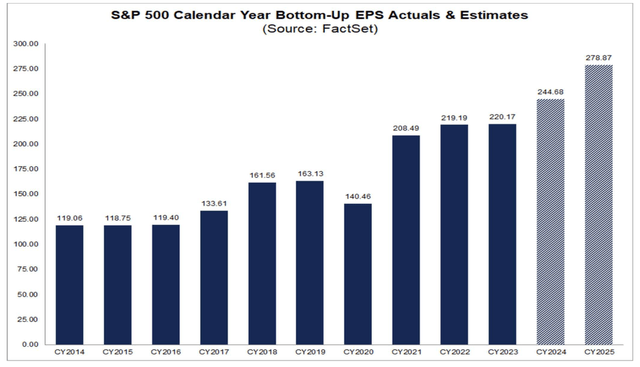

Putting it all together, the S&P 500 now trades at roughly 21 times forward earnings estimates. This may sound lofty, and it is, but we have also seen forecasters raise their full-year 2024 EPS estimates for large domestic companies – something extremely rare. So, while the SPX has been up nicely year-to-date, much of the gains have been through a nice rise in realized and estimated earnings, not just multiple expansion.

S&P 500 EPS higher, near $280 (est.) for 2025

Set of facts

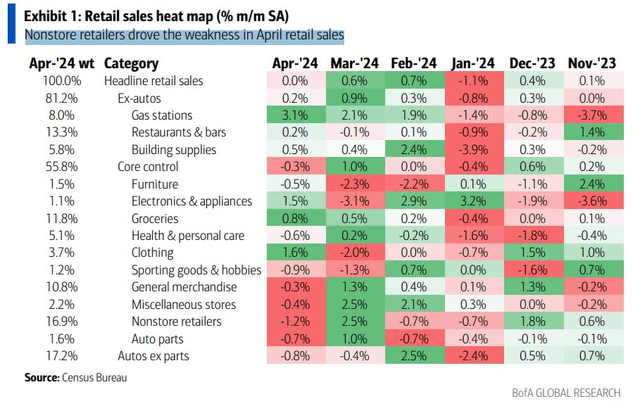

Will there be challenges in the future? A slowdown in consumer spending may be afoot. As we all hear from retailers, restaurants and travel companies about upcoming price cuts, April retail sales report It revealed a softer spending picture. Weakness was particularly noted at non-store retailers (also known as online retail), but most categories were much lighter compared to strong sequential spending trends in February and March.

This is good news in the sense that easing the gas pedal for households could mean lower inflation in the coming months…which is what Chairman Powell and the FOMC want to see before cutting interest rates.

Softer retail sales in April

Bank of America Global Research

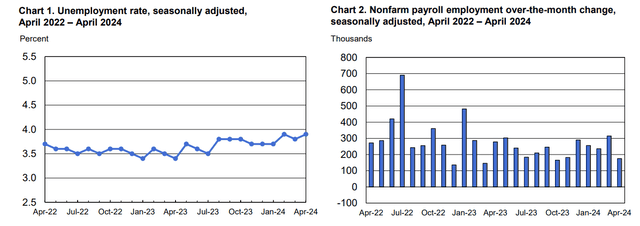

The Fed is also closely monitoring developments in the labor market. April employment report It showed a much slower pace of hiring compared to the non-farm payrolls gain of 300K+ in March. This is another sign that the economy is cooling. We’ll get important clues about the state of the labor market next week from several reports, including the ISM PMI employment sub-indices, the March JOLTS survey, the May ADP special report, and of course the Labor Department’s May nonfarm payrolls report.

US job growth declined in April

Bureau of Labor Statistics

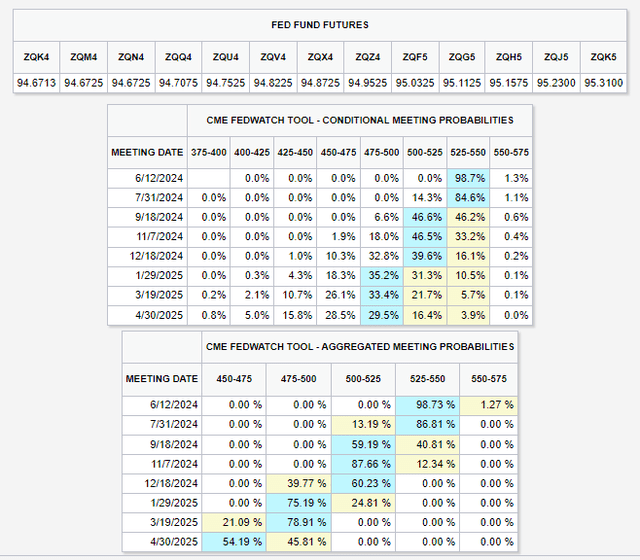

Right now, the market is now pricing in slightly more than a quarter point of a rate cut by the Fed this year. It is highly uncertain when that will happen, but the odds are that the September 18 meeting, less than two months from the general election, will be when the easing will be announced. Could a cut happen in July? Yes, but we have to see a very impressive set of inflation numbers for May and June. Any rise in consumer prices could result in initial easing being delayed until 2025.

28 basis points for cuts until 2024

CME FedWatch tool

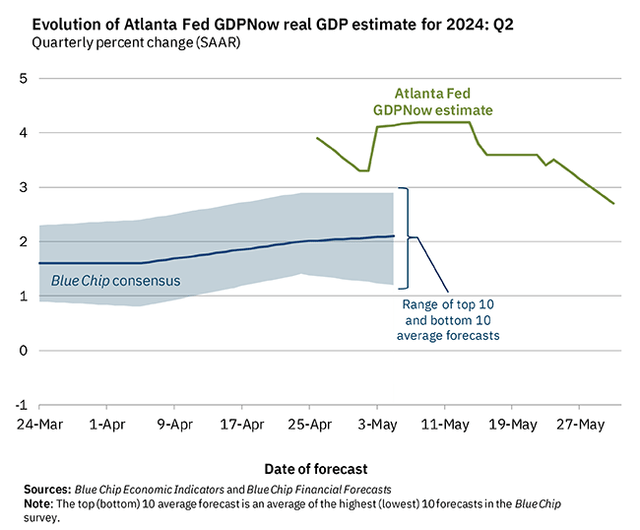

The growth picture looks good. Not too hot, and definitely not cold. According to the Federal Reserve Bank of Atlanta’s GDP Now tool, real GDP for the second quarter is 2.7%, down from 4% as seen during the first half of May. Most signs point to a significant macroeconomic slowdown compared to the hot pace of expansion during the back half of 2023.

Q2 GDP expected to be less than 3%

Atlanta Federal Reserve Bank

Bottom line

After the “Dow Jones 40K” hype a few sessions ago, stocks pared gains through the end of May. However, the “sell in May and go away” advice proved to be very bad advice, as both large and small-cap stocks posted stunning gains. With earnings largely in the rearview mirror and the Fed in a blackout period, the focus turns to next week’s macro data and technical price action.