Editor’s note: Seeking Alpha is proud to welcome MarketGauge as a new contributing analyst. You can become one too! Share your best investment ideas by submitting your article to our editors for review. Get published, earn money and get exclusive access to SA Premium. Click here to learn more »

com. primaryimages

Originally published on June 2, 2024

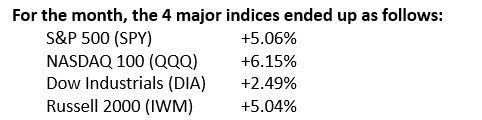

Welcome, readers, to our weekly Market Outlook as we head into the new month of June. This is now the beginning of the summer months and is typically a quieter market environment. More on that later.

We hope that last May was a profitable month for you in your trading and investment accounts. May continued the bull market trajectory that began in October 2022 and has now produced positive returns for 4 out of the first 5 months from 2024, a move that many of Wall Street’s best and brightest analysts did not see as possible. Recently, many of them have raised their stock market price forecasts for the end of 2024.

All of this came with enhanced volatility, as we have been suggesting throughout the past four to six weeks of market forecasting. There are current headwinds, including declining economic numbers and the potential for this to occur No interest rate cuts by the Federal Reserve until later in the year. The betting pool now has cut odds with the highest probability of arriving in November and two weeks after the election so as not to influence the vote.

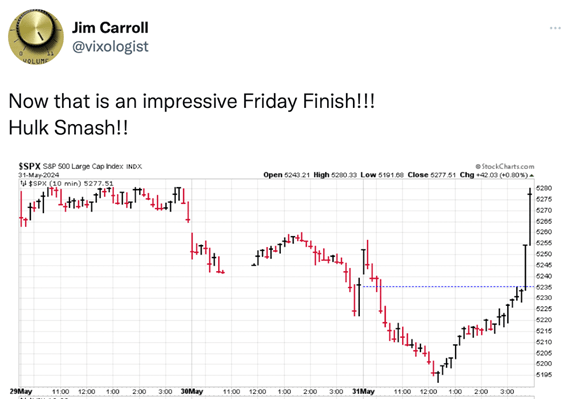

In fact, if the stock market closed at 2:00 PM on Friday instead of at 4:00 PM as regularly scheduled, market returns, especially the S&P 500, could look very different relative to monthly returns. The Japanese yen fell 0.80% before mid-afternoon on Friday and reversed trend and closed down 0.80%, representing a 160 basis point reversal. If yields had been flat earlier in the day, the S&P would have risen 3.46% during the month instead of 5.06%.

big difference. As you will soon see, this could have changed some of the positive expectations of what would happen if the market closed with a 5% or better return for May (instead of 3.4%). See some charts below that show this shift late Friday.

Market measurement strategies

Many of our investment strategies rose significantly during the month as our systematic quantitative trading continued to uncover popular opportunities across various stocks, sectors and commodity-related instruments. The GEMS strategy’s model ETFs (comprising a global mid-cap and macro sector) were up over 9% during the month, as semiconductors, metals and mining, including gold and silver miners, helped contribute to those returns.

Large-cap stocks rose more than 6.9%, with technology (semiconductor) and utilities/energy stocks helping to lead the way. Then there’s our primary tactical strategy, Profit Navigator, which is up 7.8% for the month in the risk-managed 2x SPY ETF strategy.

The bull continues

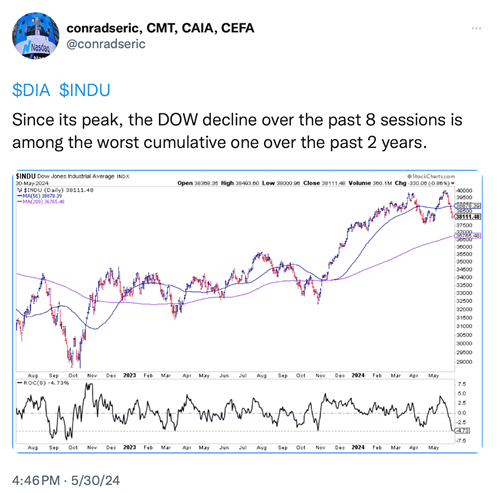

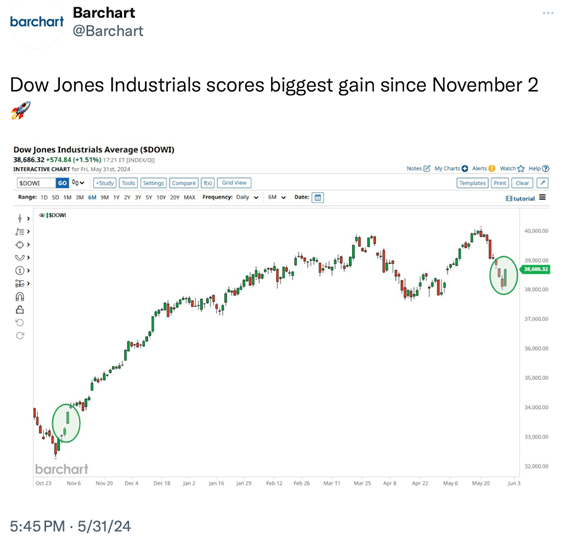

We’ve reiterated several times recently that earnings have been the main driver of our strong performance numbers so far in 2024. This is in the face of persistent inflation, rising interest rates and signs of a slowing economy. This has started to show in some recent gains that have taken the Dow Jones down 8 of the last 9 days on the market. See charts on the Dow Jones below:

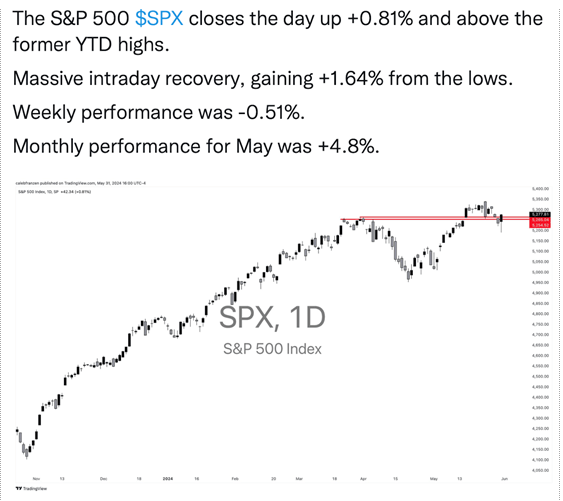

But on Friday, the Dow Jones came back strong. Is this a preview of something more positive in June? (Don’t count on it). See graphs below:

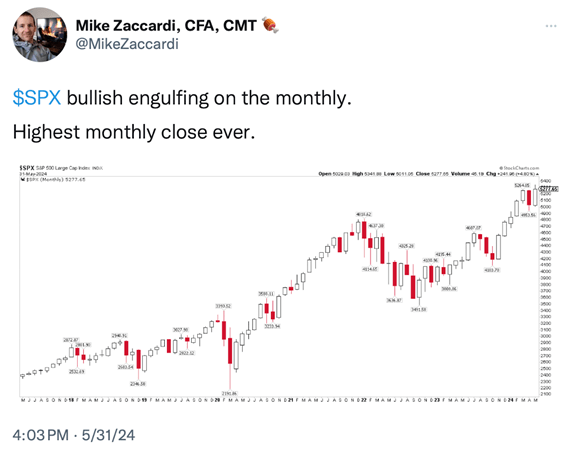

The S&P 500 finished at its highest monthly close never. In addition, a positive sign is that the S&P 500 also ended the month at… rising Sweeping candle. see below:

It’s all about profits

As we mentioned during the previous two weekly market forecast bulletins, markets behaved positively on the back of better than expected earnings.

The stock market is enjoying a period of exceptional success. Investors were feeling positive, especially as stock indices hit all-time highs. That the Dow recently crossed the 40,000 mark only helps boost confidence.

There are several key factors that help contribute to this market euphoria. The core PCE inflation figure fell on Friday by 0.1%, indicating that inflation is moderating. A resilient and strong economy coupled with impressive corporate earnings have helped create a positive environment for investing in stocks in the United States.

Michael Arone, chief investment strategist at State Street Global Advisors, this week highlighted the economy’s unexpected resilience as a major diving force. Despite predictions of a recession, the economy continued to expand, driven by consumer spending and a strong labor market. Aroni also noted that although GDP growth has slowed slightly, estimates for the next quarter remain more promising.

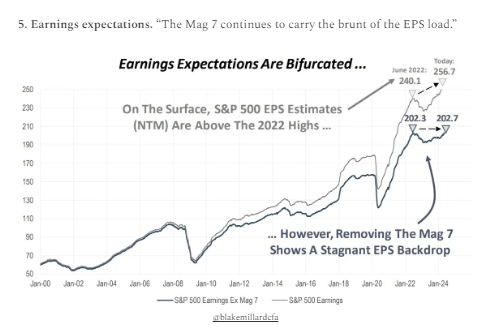

This writer maintains his belief that corporate profits were the main driver of stock market performance, as the majority of companies in the US Morningstar Market Index announced positive surprises. However, the latest chart shows that without Magnificent 7’s stellar positive earnings, earnings may have stagnated. See chart below:

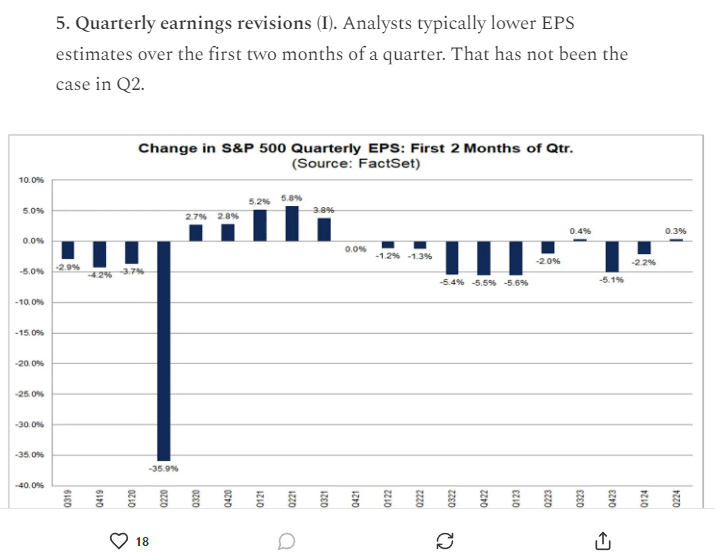

Earnings revisions were non-existent

Typically, after the first two months of a quarter, analysts start revising their earnings forecasts. This is not the case for 2024. This bodes well going forward.

It’s been mostly about growth

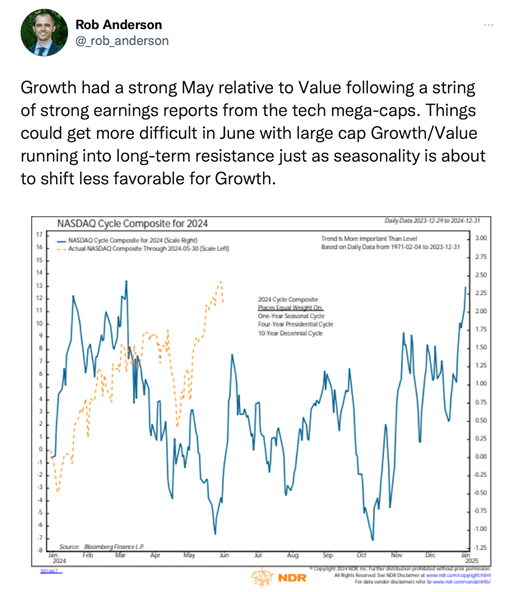

So far in 2024, growth stocks have a huge advantage over value stocks. VUG (Vanguard Growth ETF) is up 12.8% versus VTV (Vanguard Value ETF) up just 7.8%. However, analysts are beginning to believe that the appreciation of growth stocks may be slowing and that value may be catching up, especially with the Federal Reserve likely to cut interest rates later this year. Growth stocks, as shown in the Nasdaq cycle chart below, are starting to encounter some resistance compared to value stocks.

Will the bull market continue?

We don’t know, but there is plenty of empirical evidence to suggest that this is an election year, along with the positive economic factors mentioned above. It can continue.

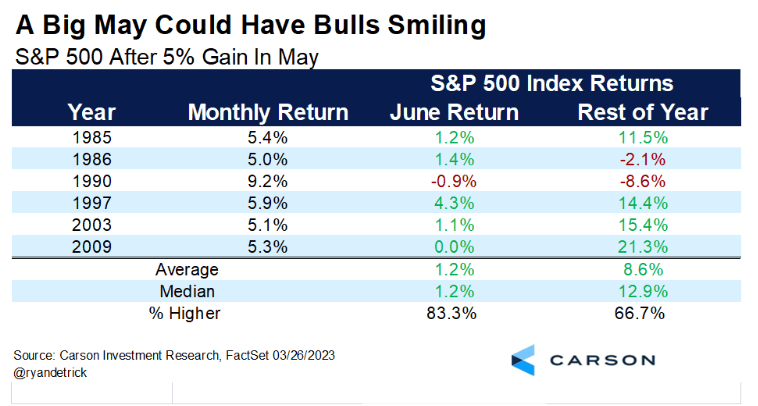

Instead of talking about why corporate profits, consumer spending and a tight labor market could remain strong and provide tailwinds for investors, we present what typically happened with a positive 5% result in May, an election year and other factors that could indicate we will. . Continue to see the bull market prevail.

Better than 5% might keep bulls smiling

We love the charts and graphs that Ryan Detrick provides for Carson Wealth Management. We appreciate that he produces these. Now that we know that the S&P 500 (SPY) underperformed by 5% or more, this chart has new meaning. see below:

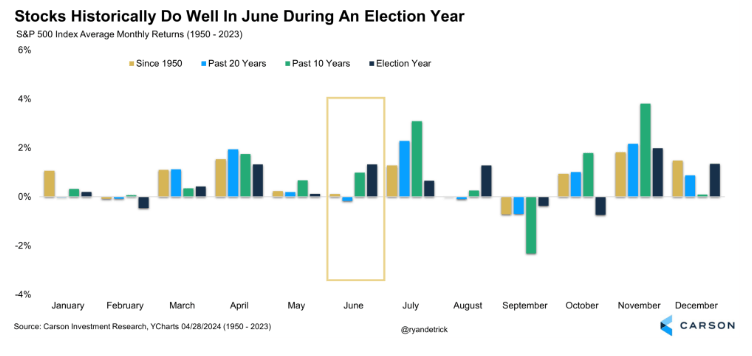

Positive forecast for the summer months

All indications are that since this is an election year and because we have seen a positive market so far 5 months later, we may not see the June swoon that investors may be anticipating. See chart below:

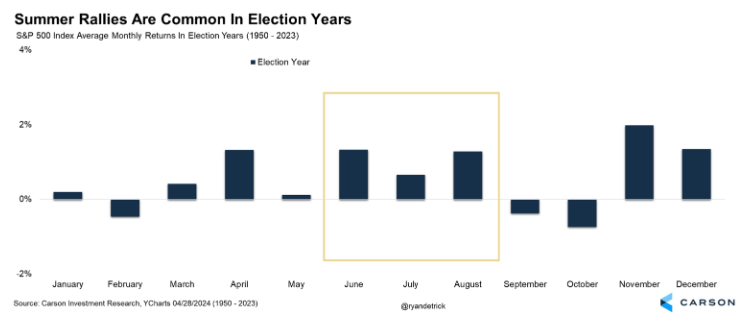

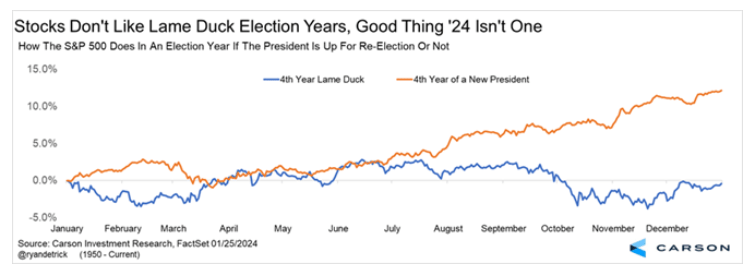

Here’s a close-up of the above chart for election years only:

Stocks perform better in the election cycle when the president is not lame

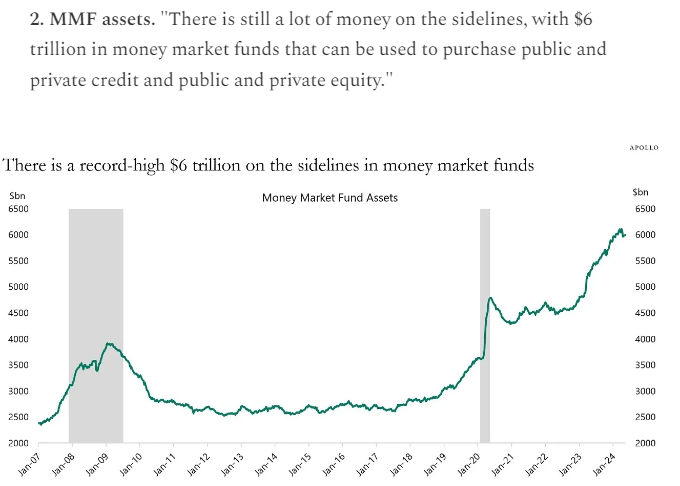

Which may help contribute to a positive market for the remainder of the year next to Election cycle? There is still an abundance of money market funds sitting on the sidelines. See chart below.

How do you know when to take some money off the table?

Naturally, we are biased because we have the best tools to evaluate the investment environment.

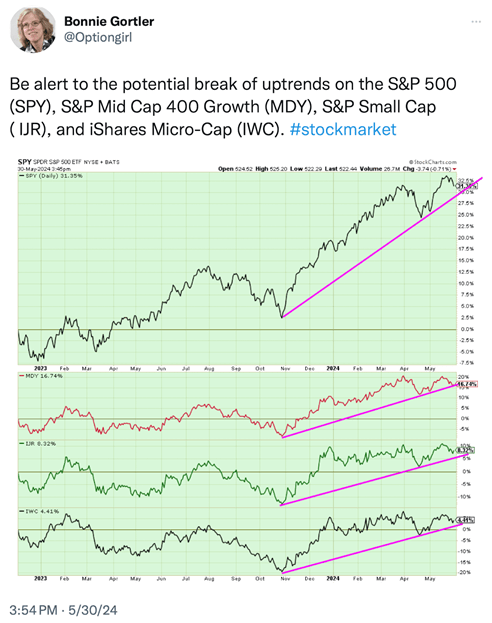

Another thing you can do, is to monitor trends and draw trend lines that will keep you on the right side of the market. I saw this chart yesterday, which identified some of these trend lines just this week, and I thought it might be helpful to review them below:

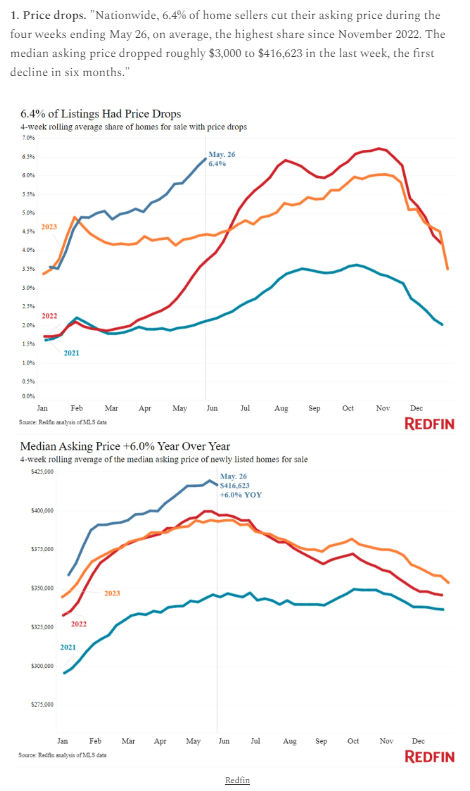

A quick update on the home prices we discussed last week

There has been a historical pattern over the past few years in housing prices. The chart below is an excellent depiction of what our housing markets look like compared to the past few years. Will we see another period of housing price declines? see below:

I now hand it over to Keith and his team who built the BIG VIEW bullets below. Powered by OPTUMA charting service, these charts provide a clearer, more precise appearance. This upgrade has enabled us to expand the analysis types and increase the number of charts for better analysis, unique perspectives, and better context.

Enjoy, and I hope you have a good week ahead in your investment accounts.

Risk

- Only three sectors declined during the week, with the strongest sectors being utilities and retail. (+)

- Strong week for energy overall, led by clean energy TAN and PBW. (+)

- Risk metrics were unchanged during the week and remain risk appetite. (+)

- The 1-month versus 3-month volatility ratio continues to improve. (+)

- Despite jumping back into the bull phase for value stocks by Friday, growth stocks are still outperforming in the long and short term. (+)

- 5 of the 6 modern family members recovered or maintained their bullish phase by the end of the week, with the carriers finally reclaiming their 200-day moving average. (+)

- A possible double top in gold with a loss of its leadership against the S&P in the short term and possibly crossing the 50-day moving average and recent lows around 210. (+)

Stop risks

- Distribution days are greater than accumulation days on volume patterns across the board.(-)

- The McClellan Index remains in negative territory. (-)

- The NYSE new high and new low ratio are negative across the board, while the Nasdaq is improving in the medium term. (-)

- The number of stocks above the major moving averages, despite Friday’s bounce, continues to deteriorate overall. (-)

neutral

- The Dow Jones slid into a strong warning phase, while the IWM recovered nicely after testing its 50-day moving average and rebounding to a full bullish phase by Friday’s close. (=)

- The CBOE Volatility Index saw a big jump and a major reversal pattern, which, if it crosses Friday’s high, would be an indicator of risk aversion in the market. (=)

- Interest rates jumped during the week and are back in the bearish phase, but remain within the long-term trading range. However, in the short term, prices are back in the recovery phase. (=)

- Emerging markets were hit hard, closing in a warning phase, and losing their lead over US stocks, as more established markets hold up better and remain in a bullish phase. (=)

- DBA has regained its bullish phase and maintains its leadership against the S&P. (=)

Editor’s note: The summary points for this article were selected by Seeking Alpha editors.