ilbusca

Elevator pitch

My review for CAPCOM LIMITED (OTCPK:CCOEY) (OTCPK:CCOEF) (9697:JP) is a suspension. Previously, I assessed the underperformance of Capcom’s stock price and assessed the stock’s valuations in my January 5, 2024 editorial.

CCOEY’s fiscal year 2023 is indicated Calendar year ending March 31, 2024 Results presentation slidesI will adopt the definition of a company’s fiscal year for the purpose of this article.

This update focuses on CCOEY’s financial outlook and the company’s latest announcements, which support the Hold rating. On the negative side of things, I’m concerned that Capcom’s operating profits for fiscal 2024 (March 31, 2025) may come in below expectations. On the positive side of things, I have a positive opinion about the company’s increased focus on talent management and the recent update on the launch of a new Monster Hunter game.

The company’s shares are traded on the OTC (over-the-counter) market and the Japanese stock market. Capcom’s TSE-listed and over-the-counter shares feature average 10-day daily trading values of $24 million and $120,000 (Source: Standard & Poor’s Capital IQ data), respectively. Interactive Brokers is an American stock brokerage firm that provides trading services for Japanese stocks.

Uncertainty regarding operating profit expectations

I see there are doubts about Capcom’s financial outlook for the new fiscal year.

Capcom guided for a 12% increase in its operating profit to JPY64.0 billion for fiscal year 2024 as shown in the company’s fiscal year 2023 results presentation slides. CCOEY’s operating income also grew 12% in fiscal 2023, so the company expects it can maintain a similar level of operating profit growth this year.

In my opinion, CCOEY’s actual operating income for FY2024 may be lower than expectations, taking into account two main factors.

One major factor is that Capcom’s most recent fiscal year operating profits came in below the consensus estimate.

The company announced its financial results for the full fiscal year 2023 in early May. CCOEY’s FY2024 operating profit of JPY57.1 billion turned out to be 5% below sell-side analysts’ expectations of JPY60.1 billion according to Standard & Poor’s Capital IQ Data.

In my January 2024 editorial, I noted that Capcom may be “earning relatively lower margins on its older games” due to “pricing improvement initiatives.” In its recent FY2023 results briefing, CCOEY stated that its strategy is to generate revenue from certain games “over the long term as a high-margin catalog title by implementing… Digital discounts are phased.“(my emphasis)

While it’s nice for Capcom to be able to extend the “life” of certain games, this comes at the cost of lower margins for the games as they mature. I think this is why CCOEY had a 5% higher win (Source: Standard & Poor’s Capital IQ) for fiscal year 2023 even though operating income for the last fiscal year was 5% lower.

Another key factor is that achieving CCOEY’s FY2024 operating profit target appears to be highly dependent on the success of new game launches.

Specifically, Capcom’s full-year FY2024 operating income guidance of JPY64.0 billion assumes that the company generates operating profits of JPY20.0 billion and JPY44.0 billion for the first half of FY2024 and the second half of FY2024, respectively. . The company explained in its fiscal year 2023 results presentation slides that the higher operating profits expected for the second half of fiscal year 2024 are due to the “timing of new title releases.”

It would be reasonable to assume that new games will represent a significant portion of Capcom’s expected operating profits for fiscal 2024, based on dividing the company’s earnings guidance by the first half and the second half and its management’s comments. Relying on new games, which have every chance of success or failure, to generate significant operating income implies downside risks associated with CCOEY’s guidance.

To sum things up, I’m not sure CCOEY will be able to achieve its operating income guidance for fiscal year 2024. In other words, my view is that there is a reasonably good chance it will miss operating earnings for the new fiscal year.

Investing in talent and expanding the Monster Hunter game series are major positive developments

I have my doubts regarding Capcom’s operating income growth outlook as detailed in the previous section. On the other hand, I’m encouraged by CCOEY’s recent announcements regarding talent management and the groundbreaking Monster Hunter game series.

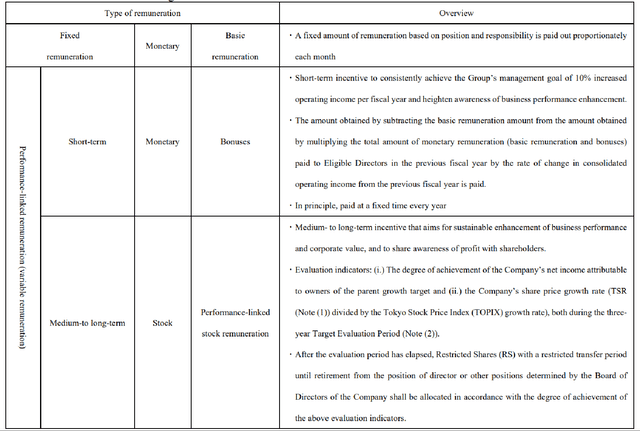

CCOEY announced on May 15, 2024 that it had made changes to allow “remuneration for eligible directors” to “vary according to the degree of growth in business performance” with a “new system of performance-linked equity awards.” The new rewards framework is detailed below.

An overview of Capcom’s new rewards framework

Capcom announcement on May 15, 2024

As shown in its most recent fiscal year results presentation slide, the company has raised average employee pay by +30% since FY 2022. Looking ahead, CCOEY has plans to increase entry-level employees’ monthly pay by approximately +28% for FY 2022. FY 2022 Ending March 31, 2026.

In its previous fiscal 2023 earnings call on May 13, Capcom emphasized that it “seeks to invest in employees as one of our strategic management priorities to ensure (the company’s) long-term growth.” CCOEY has already placed a stronger focus on talent investment and management as seen in its recent actions. This bodes well for Capcom’s long-term growth prospects, as retaining and attracting top talent will help the company remain competitive in the gaming industry.

Separately, Capcom revealed in a May 14 media release that “Monster Hunter Wilds, the newest title in the Monster Hunter series” is scheduled to release in the 2025 calendar year.

Monster Hunter has been a very successful game series for CCOEY. The company’s two best-selling titles of all time are “Monster Hunter: World” and “Monster Hunter Rise,” which have sold 20.1 million and 14.7 million units respectively to date.

But recent unit sales in fiscal 2023 for “Monster Hunter: World” and “Monster Hunter Rise” were down 65% and 60% (source: results presentation), respectively, compared to their unit sales in the first year of launch. . As such, there is an urgent need for Capcom to expand the Monster Hunter series to boost its future revenues. Assuming the new “Monster Hunter Wilds” game is a hit, this will likely contribute to significant sales for CCOEY in fiscal year 2025 (April 1, 2025 to March 31, 2026).

Concluding thoughts

I still have a neutral view of Capcom. I considered CCOEY’s operating income growth forecasts and the company’s latest disclosures before assigning a Hold rating to the stock.

Furthermore, the stock appears to be trading at a reasonable valuation, as its expected operating earnings growth rate is roughly equal to its operating earnings multiple. According to source data Standard & Poor’s Capital IQthe FY2023-2026 EBITDA CAGR estimate and consensus FY2024 EV/EBITDA multiple for Capcom are +14.1% and 13.9x, respectively.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.