Capital Potential: Earnings safety and valuation are attractive, but fundamentals are worrying

Mr. Pliskin/E+ via Getty Images

introduction

Prospect Capital (NASDAQ:PSEC) is a BDC popular among dividend investors and retirees as a result of its fixed monthly dividend. But while many of its peers have enjoyed a strong price rise over the past year, BDC has seen its share Prices fell by double digits during the same period, as a result of the quality of its portfolio and weak fundamentals.

Share prices of business development companies (BDCs) with superior underwriting quality have risen, while those with weaker fundamentals have lagged, with some trading at a discount to their net asset value prices. In this article, we take a look at the company’s dividend health, most recent earnings, and fundamentals to see if PSEC is worth investing in at the current price.

Previous thesis

I last covered Prospect Capital last January in an article in which I categorized BDC as a contract titled: Potential capital: Quantity over quality. As profits Investor, I always buy property with a long-term outlook, and just because it pays an attractive dividend or higher yield doesn’t make it a good investment in my opinion.

I discussed BDC’s stagnant earnings growth, which has not grown over the past seven years and tapered in 2017. I also touched on Q1 earnings, which surprisingly saw both net investment and total investment income rise on a quarterly basis.

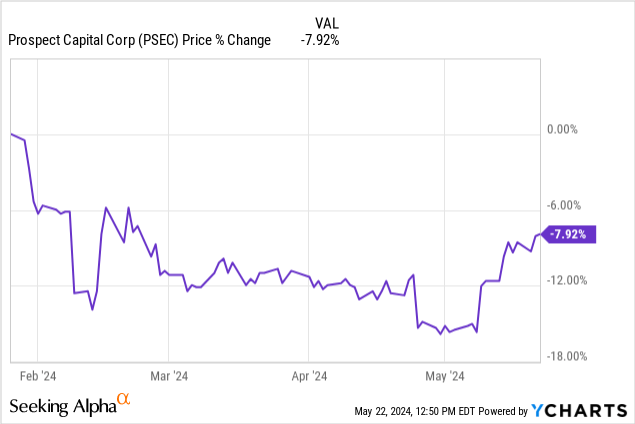

But since then, PSEC has continued to report its second and third quarter earnings but its stock price has fallen by almost 16% to $5.71 where it is currently trading. This is likely a result of its weak fundamentals and portfolio quality. Although their dividend profile and valuation are currently attractive, I continue to rate the stock as flat.

Earnings update

Prospect Capital reported its third-quarter earnings on May 9 with a net investment income beat of $0.03. This came in at $0.23 for the quarter, down one cent from the previous quarter and flat from the first quarter. Additionally, on an annual basis, National Insurance fell to $94.4 million from approximately $102.2 million.

The likely reason for this is the company’s decline in portfolio investments. During the quarter, the number of portfolio companies reached 122 companies, down from 124 in the previous quarter and 128 in the first quarter. PSEC also created assets during the fourth quarter in middle market companies and 29% in real estate. 5.6% of this was in middle market lending and acquisitions.

Real estate currently represents 18.4% of its total investment portfolio. However, to be fair, PSEC targets what I believe are solid properties with most of its investments in triple net leases (all financial responsibilities fall to tenants), multifamily, student housing, self-storage, and senior living facilities. And with the higher and longer environment, management is specifically targeting preferred stock investments which I think is a smart move on their part.

But over the past year or so, the commercial real estate market has been soft, so investors should continue to be wary of it when investing in the downtown business district. PSEC management also mentioned during earnings that it was specifically targeting distressed sellers as there was an opportunity to tap those who needed capital to address other issues within the business. While this can provide short-term gains, this speaks to the quality of their portfolio and is likely to lead to problems if the economy faces further uncertainty such as a recession.

Investing in companies that have struggled as a result of the high interest rate environment means a willingness to lend to lower quality companies, which erodes the quality of BDC’s portfolio over time. This in turn can lead to higher outstanding receivables, PIK income, and may ultimately lead to lower finances in the foreseeable future. So, while lenders can negotiate better deals on the front end, this is a long-term issue of temporary gains.

Total investment income also decreased by 6% year over year from $215.1 million to $202.2 million. This was $210.94 million in the previous quarter. So, financially, PSEC has not been performing as well as many of its peers, which is likely why the share price has fallen over the past four months.

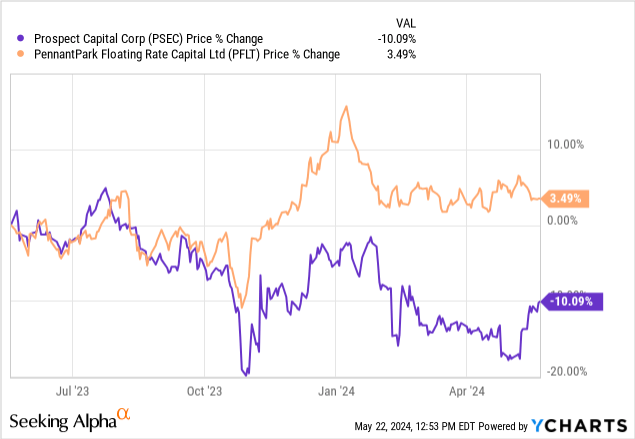

Over the past year, PSEC has underperformed, declining by roughly 10%. This compares to its monthly peer PennantPark Floating Rate Capital (PFLT), which is up approximately 3.5% over the same period. So, while many BDCs have rewarded their shareholders with special and supplemental dividends as well as strong share price appreciation, PSEC has done neither, making it an unattractive investment in my opinion.

Regarding the decline in net navigation value

Another worrying metric apart from the year-on-year decline in their financials is the ongoing erosion of their net asset value. During the third quarter, PSEC’s NAV continued to erode at $8.99. This represents a decline of 2.7% from $9.24 in the first quarter. However, this amount is up from $8.92 in the previous quarter, but it is still something shareholders should pay attention to when investing.

Author’s creation

Some BDCs experience a slight reduction in NAV or National Insurance as a result of dividend payments or the timing of loan repayments. But the continued decline is something that should start worrying investors. This typically indicates the BDC’s underwriting ability and portfolio quality.

Bear, PennantPark’s net asset value grew quarterly and year-over-year from $11.15 to $11.40. High-quality business development firms such as Ares Capital (ARCC), Blackstone Secured Lending (BXSL), and Main Street Capital (MAIN) have seen their net asset value grow year-on-year. Furthermore, if management can turn things around and continue to grow its portfolio at a healthy rate, and see some healthy NAV growth in the next couple of quarters, I would consider upgrading the stock with a buy.

There is some good investment in PSEC

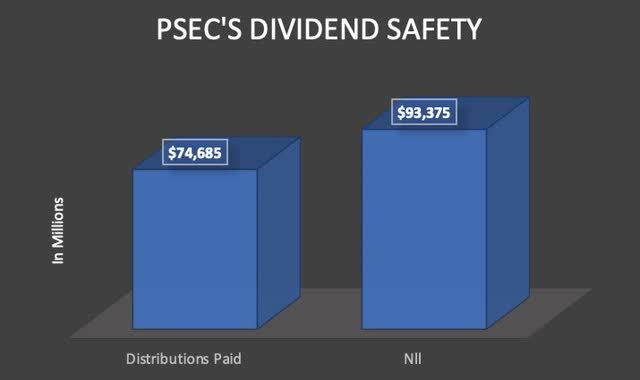

Although BDC’s declining financial position and eroding net asset value worry me, there are some positives when investing in PSEC. First, you get monthly dividends covered by net investment income. During the quarter National Insurance was $0.23 or $94.4 million. This covers a quarterly payment of $0.18, giving PSEC dividend coverage of 127%, which is very comfortable.

That’s actually higher than peers PennantPark, which generated net investment income of $0.31 during its most recent Q2 earnings. Using their monthly dividend of $0.1025, this would give them approximately 101% quarterly coverage.

PSEC also paid out approximately $74.7 million in dividends giving it a safe payout ratio of 79.1% for the quarter. Through three quarters, PSEC earned approximately $317 million in NII and paid out approximately $222 million in distributions, giving it a lower payout ratio. As indicated by the conservative payout ratio, I believe it would be appropriate for management to buy back shares while the company is trading at a significant discount to its net asset value. This will likely not only increase shareholder confidence, but will also boost their dividend payout ratio as well.

Furthermore, management announced dividends for the months of June through September, demonstrating their confidence in their ability to reward shareholders. Therefore, from a dividend perspective, PSEC is an attractive investment as its dividend integrity remains intact despite the erosion of NAV and decline in financials year-on-year.

Author’s creation

Low leverage

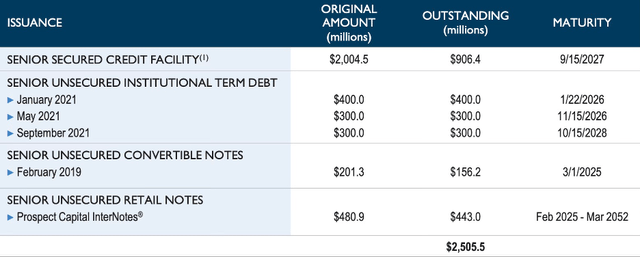

PSEC’s leverage level at the end of the quarter was also low at just 0.46x, leaving it in a financially strong position. This compares to 1.2x for PennantPark at the end of Q2. Its debt maturities are also good and do not mature until 2025. It is also rated investment grade by Standard & Poor’s and Moody’s, giving it cheaper access to capital than its unrated peers.

PSEC Investor Presentation

Undervalued

Another reason PSEC might be attractive is its current share price. At a P/NAV ratio of approximately 0.63x, the BDC is well below the 3-year average discount of 27.66%. Most BDC peers trade at premiums well above their NAV prices. But by seeing the company’s eroding NAV and unimpressive financials, you can understand why the market is pricing it at a discount to its NAV.

But as mentioned earlier, the stock from a dividend perspective is attractive because it is difficult to find many BDCs trading at a discount as a result of the high interest rate environment. Additionally, their discount of approximately 37% is higher than the 3-year average discount as mentioned earlier. Therefore, from a valuation point of view, BDC also looks attractive.

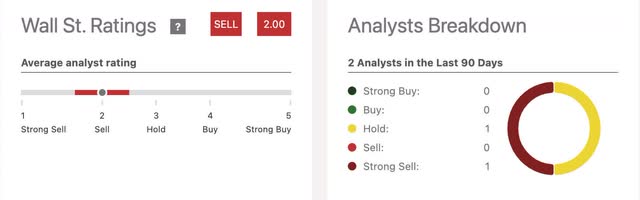

However, Wall Street rates the stock a Sell, likely a result of the ongoing NAV decline and the headwinds PSEC has faced in the rising interest rate environment. Although I’m not ready to give them a Sell rating yet given their strong balance sheet and well-covered dividend, if NAV continues to erode, I think the stock will warrant a Sell rating in my view. But with interest rates likely to peak and financial conditions likely to become more favorable in the next four to six months, I’m willing to give PSEC a chance to recover, hence the hold rating for now.

Seeking alpha

Risks

The high interest rate environment has put downward pressure on business development companies, especially those considered to be of lower quality. As a result, its stock prices lagged. Aside from lower-quality borrowers feeling the effects of higher interest rates in the long term, PSEC exposure to real estate should also be a concern.

However, management has increased its exposure to senior-lien loans, putting the portfolio in a more defensive position. At the end of the quarter, first lien exposure was 59%, up from 54.4% year over year. Another risk the company faces is the continued decline in its net asset value, which will likely negatively impact its stock price in the future.

minimum

PSEC has underperformed the broader market and many of its peers, likely as a result of its declining financial positions, exposure to real estate, and eroding net asset value. But as a result, its share price is now trading at a greater discount to the 3-year average, making it attractive.

Moreover, their monthly earnings remain safe with a payout ratio of up to 70% during the first nine months of the financial year. Moreover, if interest rates remain higher for longer, PSEC will likely continue to face headwinds due to its exposure to real estate and its preference for lending to distressed sellers. Although valuation and earnings are attractive, I continue to rate Prospect Capital as Hold for now.