Wiggle/iStock via Getty Images

We’ve previously covered Celestica Inc. (New York Stock Exchange: CLS) in March 2024, to discuss how it will benefit from the ongoing generative AI boom, with growing demand for machine learning/AI-related products likely to spur its up/down acceleration Line growth through fiscal year 2026.

Despite an inherently low-margin manufacturing business model, we believed there were still significant growth opportunities over the long term, attributable to the ramp-up of operations in Thailand/Malaysia, where we initiated a buy rating at the time.

Since then, CLS has risen further by +27.5% well outperforming the broader market by +1.6%. However, we’re maintaining our Buy rating here, thanks to promising demand feedback from recent earnings calls for Nvidia (NVDA) and Super Micro Computer (SMCI).

This is further supported by CLS management’s promising guidance for Q2 2024, increasing return on invested capital, and finally, guidance of accelerating year-over-year growth. Annual basis in the coming quarters.

CLS’s investment thesis remains strong, thanks to NVDA’s impressive earnings results

Currently, CLS reports double-digit earnings for Q1 2024, with total revenues of $2.2 billion (+7.8% QoQ/+20.2% YoY), and gross operating margins of 6.2% (+0.2 points). QoQ/+1 YoY/+3.5 from FY19 levels of 2.7%, and adjusted EPS of $0.86 (+22.8% QoQ/+82.9% YoY).

Much of the tailwind was attributable to the strong performance observed in the Cloud and Connectivity Solutions segment, with accelerating revenues of $1.44 billion (+8.2% QoQ/+38.4% YoY) and expanding operating margins of 7% (+0.3 points QoQ/+1.2 YoY/+3.4 from FY19 levels of 2.6%.

This isn’t actually a surprising development, thanks to “continued strength in demand for AI/ML computing and networking products from hyperscale customers.”

Especially since NVDA recently announced an impressive 1Q24 revenue of $26.04 billion (+17.8% QoQ/+262.1% YoY) while achieving 2Q24 revenue of $28 billion (+7.5% QoQ/+107.4% YoY), breaking the consensus. Estimates are $22.03 billion and $26.8 billion, respectively.

The same was reported by SMCI, a complete server solutions provider, with Q1 2024 revenue of $3.85 billion (+5.1% QoQ/+200% YoY) while Q2 2024 revenue stands at $24 to $5.3 billion (+37.6% QoQ/+143.1% YoY).

These developments continue to indicate strong demand for generative AI infrastructures, thanks to their inherent leadership in the data center segments and full server solutions markets.

At the same time, NVDA is already routing new AI chips every year instead of the previous cadence of every two years, which means an accelerating replacement cadence, which naturally leads to more tailwinds for Electronics Manufacturing Service (EMS) and OEM (OEM) companies. ODM), such as CLS.

This is particularly due to CLS’s involvement in the broader technology market, where the AI-generated boom has already led to a notable expansion in sales of cloud-related electronic components.

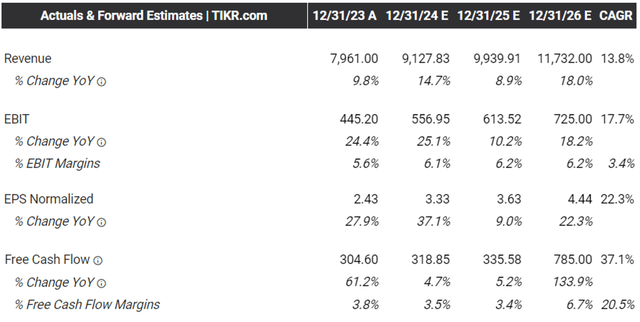

As a result, CLS admittedly raised its guidance for fiscal 2024 to revenues of $9.1 billion (+14.3% YoY), operating margins of 6.1% (+0.5 points YoY), and adjusted EPS of $3.30 (+ 35.8% YoY), and free cash flow of $250 million (+28.9% YoY).

This is up significantly from previous figures of $8.5 billion (+6.7% y/y), 5.75% (+0.15 points y/y), $2.70 (+11.1% y/y), and $200 million ( +3.1% YoY) filed in fiscal Q4 2023. Earnings call, further signaling its ability to capitalize on the AI infrastructure boom.

Consensus future estimates

Taker station

As a result, it is not surprising that consensus forward estimates have been raised once again, with CLS expected to generate accelerated top/bottom earnings growth at a CAGR of +11.6%/+22.2% through FY2025. This compares to previous estimates. of +9%/+15.4%, respectively.

Importantly, despite higher capex associated with ramping up manufacturing at its expanded facilities in Thailand and Malaysia through 2025, management continues to report strong free cash flow generation of $65.2 million (-22.1% QoQ/+608.6% QoQ). YoY) and margins expanded by 2.9% (-1 point QoQ/+2.4 YoY/-2.2 from FY19 levels of 5.1%) in the fourth quarter.

This indicates CLS’s ability to sustainably finance its growing operations while maintaining a healthy balance sheet with a net debt to EBITDA ratio of 0.72x in fiscal Q1 2024, compared to 0.76x in fiscal Q4 2023, And 1.12x in FQ1 2023. And 0.68x in FQ4’19.

CLS Reviews

Seeking alpha

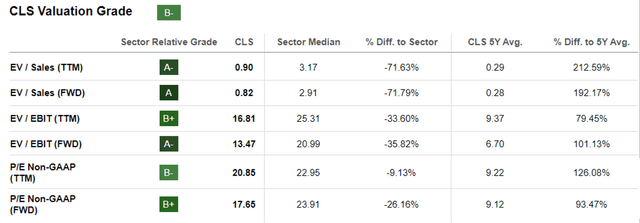

As a result, we can understand why the market is giving CLS premium FWD P/E ratings of 17.65x, which is higher than the previous article’s 16.08x and its one-year average of 10.86x.

It’s undeniable that CLS can be relatively expensive compared to its EMS and ODM competitors, including Flex Ltd. (FLEX) with FWD P/E ratings of 13.87x, and Hon Hai Precision Industry Co., Ltd. (OTCPK:HNHPF)(2317)(TW) at 10.65x, and Quanta Computer (OTC:QUCCF) at 21.80x.

Then again, the premium seems justified at the moment, given CLS’s accelerated profitable growth prospects over the next few years compared to FLEX at +2.7%/+14.2% and HNHPF at +10.5%/+15.1%, while approaching QUCCF at +34.6%/ +24.1% respectively.

So, is CLS stock a buy?Sell, sell, or hold?

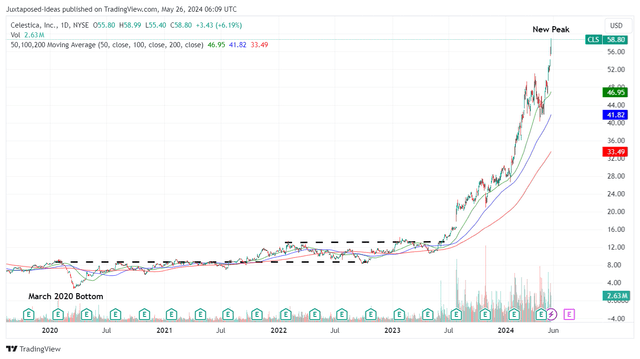

CLS 5Y stock price

Trading offer

Currently, the CLS has charted a new high beyond the highs of early 2024, while also moving away from its 50/100/200 day moving averages.

However, based on Q1 2024 annualized EPS of $3.44 (+22.8% QoQ/+82.9% YoY) and high P/E valuations of 17.65 times, the stock appears to be trading Close to our fair value estimate of 17.65 times. $60.70.

There remains excellent upside potential of +21.2% to our long-term price target of $71.30 as well, as discussed in our previous article.

As a result, we maintain our Buy rating on CLS stock, although there is no specific recommended entry point since it depends on the individual investor’s dollar cost averaging and risk appetite.

With the stock currently supported by promising NVDA and SMCI guidance thus far, we think interested investors may want to wait for a moderate rebound to its previous trading ranges of $41 to $49 to improve the margin of safety.