microstockhub

We’ve previously covered Celsius Holdings, Inc. (Nasdaq:Sila) in March 2024, to discuss why it could be the next big thing in the global energy drink market, which can be attributed to its impressive stock gains versus established companies, such as Monster Beverage Corporation (MNST).) Red Bull.

A large portion of these driving factors are attributed to successful marketing efforts, strategic partnerships and expansion of distribution channels, which support management’s commitment to achieving high growth.

Despite this, we rate the stock as a Hold at the time, with the outstanding growth ratings and high short interest likely to lead to near-term share price volatility.

Since then, CELH has fallen -11.7% as the broader market trades sideways at +1.8%. We believe the correction is indeed a gift as it results in a lower entry point and expands the upside potential against the company’s profitable growth rhythm.

along with With its growing domestic share, untapped international market, and richer balance sheet, it remains well positioned for strong growth in the future. Besides the support level identified at $70, we upgrade CELH as a buy for growth-oriented investors.

CELH continues to present a compelling growth investment thesis

Currently, CELH has announced a mixed earnings call for Q1 2024, with revenue of $355.7 million (+2.3% QoQ/+36.8% YoY) and EBITDA of $88 million (+ 34.9% QoQ/+80.6% YoY).

Part of the quarter-over-quarter headwind was attributable to “inventory volatility observed at its largest distributor,” which constituted approximately 62% of its total North American business in the fiscal first quarter of 2024, resulting in a $20 million windfall impact. on its sales.

Despite the warning that volatility may continue into 2024, we are not actually overly concerned, as CELH continues to report an impressive All Commodity Volume (ACV) ratio of 98.4% last quarter (+0.4 points QoQ/+ 3 on an annual basis). Which allows its products to reach a greater number of consumers across most flavors and size options through different channels.

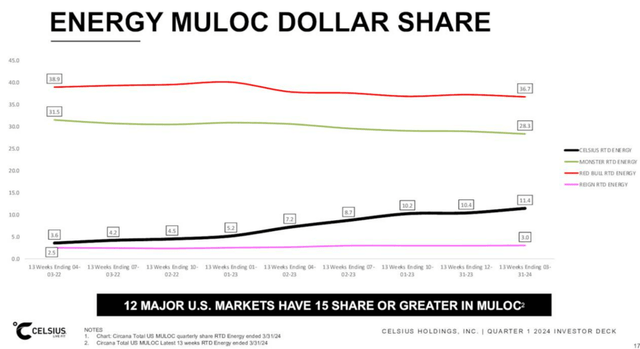

Multiple CELH Outlets with Convenience Store Market Share (MULOC).

Seeking alpha

This comes in addition to the strong growth observed in CELH’s share of the US MULOC market to 11.4% by Q1 2024 (+1 point QoQ / +4.2 YoY) and a further +0.1 point increase to 11.5% for the period of weeks The four ending April 14, 2024, according to Circana.

It is clear from the above graph that the company has been able to grow its market share at the expense of the two market leaders, MNST with a market share of 28.3% (-2 points y/y) and the privately owned Red Bull GmbH with 36.7% as of Q1 2017 2024 (-0.8 points y/y).

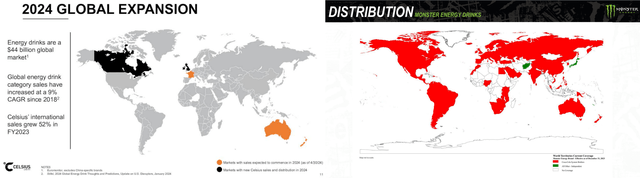

Readers should also note that international sales include only $16.2 million (+10.9% QoQ/+43.4% QoQ) or 4.5% of Q1 2024 sales (+0.2 points QoQ / +0.3 y/y), indicating the tremendous opportunity for CELH growth moving forward, assuming a similarly successful marketing effort.

The emerging presence of CELH globally, compared to MNST

Silah, Manset

For context, MNST recorded $0.63 billion in energy drink sales for Q1 2024 internationally (+12.5% QoQ/+16.6% YoY), with CELH management already highlighting a promising total global market Addressable value of $44 billion.

With CELH recently launching in Canada in Q1 2024, along with plans to expand into Australia, France, Ireland, New Zealand and the UK in 2024/2025, we believe the brand has great opportunities to disrupt established companies as it has. in the United States.

This is especially true given that management was able to report an impressive Canadian MULOC market share of 5.5% as of February 29, 2024, despite only launching on February 01, 2024.

In addition to its strategic partnership with PepsiCo, Inc. (PEP) and strong growth in the club, e-commerce, foodservice and convenience/gas channel, we believe CELH may continue to record incremental market share growth in the future.

At the same time, the same profitable growth trend was reflected in an expanding gross profit margin of 51.2% (+3.4 points QoQ/+7.5 points QoQ) and EBITDA margins of 24.7% (+6 points QoQ /+6 y/y) in the first fiscal quarter. ’24.

This was due to easing raw material/supply chain pricing issues coupled with relatively efficient operating expenses of $99.01 million (-7.7% QoQ/+43.7% YoY).

Our first quarter 2024 results show why we are increasingly optimistic about CELH’s future.

CELH is reasonably valued here – thanks to an accelerating profitable growth trend

CELH Reviews

Taker station

Right now, as the market overreacts to Nielsen’s supposedly softer May 2024 data, we’ve observed a notable moderation in CELH’s ratings for FWD EV/EBITDA of 41.16x and FWD P/E of 62.84x. This is compared to the 1Y average of 45.32x/75.24x and the 5Y average of 109.16x/312.43x respectively.

While recent valuations are still high compared to the sector average of 10.81x/17.49x, we believe the premium is fairly reasonable as CELH is still expected to deliver strong net profit/income growth at a CAGR of +34 %/+35% until the fiscal year 2026, in line with the previous article.

This compares to its direct peer, MNST, which trades at a FWD EV/EBITDA of 21.41x and a FWD P/E of 29.03x, with the consensus estimate to grow the cap/minimum at a CAGR of +10.3%/+14.6% through FY2026. .

Based on these comparisons, CELH looks very attractive here, especially due to its very healthy balance sheet with net cash of $879.49M (+16.3% QoQ/+47.6% YoY) and virtually zero debt as of Q1 2024. This was driven by incremental free cash flow generation of $130.1 million (+30,155.8% QoQ/+1,112.4% YoY) and rich margins of 36.6% (+36.5 points QoQ/+42.8 YoY).

The same was also observed in MNST at cash/short-term investments of $3.55 billion (+9.5% QoQ / +16.3% YoY) and zero debt, meaning its ability to finance its growth opportunities internally.

So, is CELH stock a buy?Sell, sell, or hold?

CELH 4Y stock price

Trading offer

Currently, CELH has been recording a sideways trading pattern over the past three months, between the $98 resistance levels and the $70 support levels.

For context, we provided a fair value estimate of $66.60 in our last article, based on FY2023 EBITDA of $1.24 (+300% YoY) and FWD EV/EBITDA valuations of 53.73x .

We also offered a long-term price target of $159, based on a similar calculation using the same valuations, consensus FY2026 EBITDA estimate of $702.2 million, and forecast FY2026 adjusted EBITDA before EBITDA per share of $2.96.

Even when factoring in the currently low FWD EV/EBITDA ratio of 41.16x, there is still more than excellent upside potential of +64.4% to our updated long-term price target of $121.80.

Based on these developments, it is certainly worth being patient, since the recent correction of CELH has resulted in a potential improvement to the upside of our updated long-term price target.

Due to the improving risk-reward ratio and strong support for the stock at $70, we are cautiously upgrading CELH to a buy price here.

Risk warning

It goes without saying that CELH may remain volatile in the medium term, due to short interest rising to 6.81% at the time of writing, although moderating from March 2024 levels of 10.58%.

Insiders have also increasingly released their gains over the last 12 months, with US$330.81m worth of shares already sold (+79.6% sequential) as they potentially cash in some long-term stock options.

At the same time, with CELH remaining in high growth mode and currently, securing premium valuations compared to its energy drink peers, readers should note that there may come a time when its growth/stock price appreciation eventually slows down and the energy drink market deteriorates. Mature.

The same phenomenon was already observed in the more stringent year-on-year comparison, where “it’s all about distribution and velocity growth since PEP distribution began,” and the subsequent market overreaction over the past week. It is clear from these developments that their premium valuations naturally come with higher expectations, with any earnings miss and/or disappointing forward guidance likely to lead to painful corrections.

This comes on top of potential inflation in its operations, with CELH management driving 3x growth in sales headcount in FY2024 – attributed to international expansion, with the potential to be a drag on the bottom line in the near term.

As a result, investors may want to monitor its implementation closely.