Imagine golf

Thesis article

Cenovus Energy Company (New York Stock Exchange: CVE) is a Canadian energy company that just increased its profits by a whopping 29%. But due to low debt levels and very strong free cash generation, it is very likely that we will be In the early innings of a very long earnings growth story. Cenovus is far from expensive and can be attractive to total return and dividend growth investors.

Past coverage

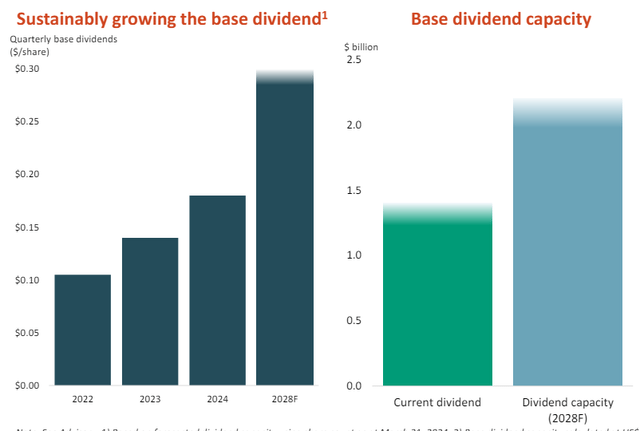

Cenovus Energy Inc. has you covered. In the past here about Seeking Alpha, most recently in 2022, in this titled article Cenovus: Buy now for a much higher dividend yield in 2023. I argued that Cenovus would increase its dividend in 2023, and it actually happened: Dividends rose from C$0.105 per share per quarter in 2022 to C$0.14 per share per quarter in 2023, resulting in a healthy 33% increase. in In 2024, Cenovus Energy increased its dividend again, raising it by another 29% to C$0.18 per quarter, which works out to just over US$0.13, yielding a dividend yield of 2.8% at current prices. Since my last article, Cenovus Energy has generated a total return of 8%, including a share price decline of nearly 10% over the past month. In today’s article, we’ll take a look at what’s happened at Cenovus in the recent past while also taking a look at what investors can expect going forward.

Macro image

Oil prices rose well over the first three to four months of 2024, but have since stabilized. After peaking at $87 per barrel for WTI (CL1:COM), oil prices have fallen, especially over the past couple of days, with WTI falling below $70 per barrel, meaning oil prices are now slightly higher. Just compared to the previous period. the beginning of the year. There are many factors at play when it comes to the recent decline in oil prices, with expectations of higher OPEC+ oil production being the most important. While OPEC+ recently extended its agreement, the voluntary cuts will be smaller during the second half of the year, as the 2.2 million barrels of oil per day in voluntary cuts continue until the end of the second quarter only. Supply from OPEC+ could therefore increase for the foreseeable future, although some cuts would still be in place – so supply would not rise significantly. However, even a moderate increase in supply can lead to an oversupplied market – and the market appears to be taking this fact into account at the moment, as oil prices have fallen over the past couple of days.

An uncertain macroeconomic picture could also play a role in the recent decline in oil prices. US GDP growth during the first quarter was revised downwards, suggesting that the economy is not in a particularly strong position. The demand for oil is driven by economic growth, so a slowdown in economic growth may negatively affect the demand for oil.

At least in the very near term, the outlook is not very strong when it comes to oil prices. However, oil prices remain at a very strong level and producers with lower break-even costs, such as Canadian oil sands companies, should generate attractive cash flows even with WTI trading in the 70s rather than the 80s.

Cenovus: Strong cash generation

Cenovus’s primary oil production assets are its oil sands operations. These have high initial costs, as building new mines and all the necessary infrastructure takes a long time and a lot of money. But once these assets are operational, they can produce oil for a very long time. The initial costs have already been paid in the past, which means that Cenovus now only has to pay for ongoing maintenance and operating costs, for example, energy and personnel costs. However, these ongoing costs are fairly low, which means that break-even prices for ongoing oil sands assets are very low. The good spread between the oil price and the company’s production costs means it can generate attractive cash flows in the current environment.

Cenovus reported its most recent quarterly earnings results in May, showing adjusted funds from operations of C$2.24 billion, or C$9.0 billion annually. Adjusted funds from operations include operating cash flows and changes in working capital, as working capital increases or decreases during a quarter can affect reported operating cash flows. Supporting these working capital changes gives us better visibility into the underlying cash flow trend. Cenovus has to invest some money in its existing assets, for example, to modernize its refineries (mostly in the US) and to maintain its asset base. However, Cenovus Energy is also investing in new assets, for example the West White Rose project in the Atlantic Ocean which is now 80% complete and will start generating positive free cash flows in 2026, according to management.

During the first quarter, these capital investments totaled C$1.04 billion, meaning the flow of free money — what is ultimately available for debt reduction, dividends and buybacks — totaled C$1.2 billion, or C$4.8 billion annually. Cenovus Energy is currently trading with a market capitalization of C$50 billion, which translates to a free funds flow multiple of 10x, or a free funds flow yield of 10%, which is very attractive.

Cenovus Energy’s capital return framework stipulates that all of the company’s excess free cash flows will be returned to shareholders once the company reaches a net debt level of C$4.0 billion – which should happen soon. At the end of the first quarter, net debt totaled C$4.8 billion, down from C$6.6 billion at the end of the previous year’s quarter. Hence, it took Cenovus Energy one year to reduce its net debt by C$1.8 billion, reducing its quarterly debt pace by C$450 million. Of course, this number will vary somewhat from quarter to quarter, depending on working capital movements, commodity price movements, etc., but it gives us a good hint about how long it might take Cenovus to reach its net debt target. Paying off the C$800 million of additional debt would therefore take a little less than two quarters, so Cenovus Energy could reach its net debt target at the end of the third quarter, or about three months from now. This is great news, because it suggests that Cenovus Energy can increase shareholder returns even further at the end of the current year.

With free money flows reaching around 10% of market capitalization at the current level, and with just under a third of that going to dividends, Cenovus Energy has enough cash for buybacks. At current valuation, I think these will be quite accretive.

Between declining shares due to the company’s future buybacks, rising production — Cenovus Energy plans to increase its output by 150,000 barrels per day by 2028 thanks to the West White Rose project and other investments — and tight controls on costs, and cash flow every year. The share should rise significantly in the coming years. This will allow the company to increase its profits at an attractive pace. The company is guiding for a dividend per share of about C$0.30 per share per quarter four years from now:

CVE Earnings (CVE View)

This would result in an annual growth rate of around 13% to 14%, which I find very attractive, especially when combined with an already very strong dividend yield of 2.8%. If Cenovus Energy actually pays C$0.30 per share in 2028, the return on cost for someone buying today would be 4.6%. If dividends were reinvested every now and then at an average return of 3%, the return on cost would grow to more than 5%. I think it’s very likely that dividend growth won’t stop in 2028. Instead, the dividend payout ratio should remain fairly low in 2028, which means Cenovus should be able to maintain a healthy pace of dividend growth beyond 2028.

Cenovus: An attractive investment for dividend growth

Although I think Cenovus Energy is not the best-run Canadian oil company (I think it’s Canadian Natural Resources Limited (CNQ), Cenovus Energy remains on the right track. Net debt is being reduced at a solid pace and the company will reach its net debt target Soon, which I believe will allow much higher returns to shareholders at the current level, buybacks will be highly accretive and will help boost future earnings growth, as a lower share count means lower overall dividend costs, all other things being equal.

I think Cenovus Energy trading at just 10x free funds flows and with significant production growth (and therefore future cash flow growth) in the coming years, is an attractive investment here.