Dragon claws

Mortgage REITs are poised to become more attractive investments for passive income investors, as the central bank prepares to cut short-term interest rates and provide relief to the highly leveraged sector in terms. From lower financing costs.

Kimera Investment Company (New York Stock Exchange: CIM) It is one of the mortgage funds that I think is worth paying close attention to, as the fund’s shares are being sold at a steep discount to book value. The mortgage REIT just completed a reverse stock split and is paying an 11% dividend yield.

The dividend was covered by distributable earnings in the first quarter, and I still expect a possible rerating once the central bank implements its first interest rate cuts.

My evaluation history

Buy stock rating for Chimera Investment in Q4 2023 due to mortgage real estate investment Confidence implemented a significant dividend reduction resulting in a realignment of its dividend with a reduction in its distributable profits.

As a result of these dividend cuts combined with ongoing book value losses in a rising price environment, Chimera Investment stock is still selling for a significant discount to book value. The mortgage fund also announced a 1-for-3 reverse common stock split.

I believe that the low dividend yield, excessive discount to book value, and reverse stock splits make Chimera Investment an attractive investment option for passive income investors with a high risk tolerance.

Possibility of splitting and repositioning the portfolio in a low interest rate environment

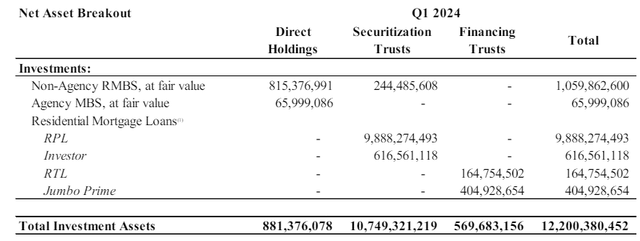

Chimera Investment owns a $12 billion portfolio of residential mortgage loans as well as non-agency residential mortgage-backed securities. The Trust’s residential mortgage loans were $11.1 billion as of March 31, 2024, while non-agency residential mortgage loans were $1.1 billion.

Mortgage-backed securities have the advantage of increasing value in a low interest rate environment, which makes Chimera Investment a compelling rerating play once the central bank lowers short-term interest rates.

Net asset penetration (Kemira Investment)

A major part of Chimera Investment’s portfolio is residential mortgage loans, which are interest-generating assets for the mortgage fund. Mortgage REITs tend to borrow money on a short-term basis and invest the money in high-yielding mortgage assets, including mortgage loans and mortgage-backed securities.

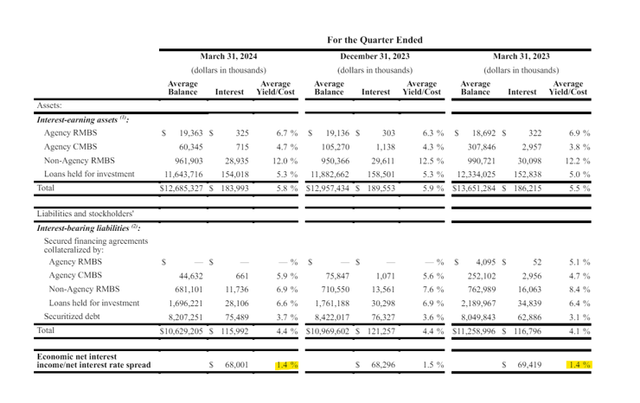

Chimera Investment’s net interest spread, a key measure for mortgage funds that rely on large amounts of debt to earn mortgage security income, was 1.4% in the first quarter, which was unchanged from a year ago.

If the central bank cuts short-term interest rates in the latter half of the year, I would expect the net interest margin to rise due to the availability of cheap debt.

Net interest rate spread (Kemira Investment)

Second straight quarter of healthy earnings coverage

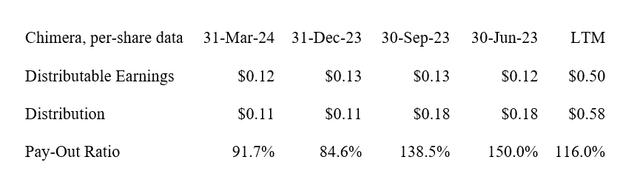

Chimera Investment had $0.12 per share in distributable earnings in the first quarter, which equates to a dividend payout ratio of 92%. Compared to the previous quarter, Chimera Investment’s dividend payout ratio increased by 7.1 percentage points, resulting in a smaller margin of safety in terms of the payout, but as such the dividend is still well covered by earnings.

The 39% dividend cut management enacted in 4Q23 was very effective in putting in place stronger payout metrics, and Chimera Investment has now had two consecutive quarters with a payout ratio below 100%. I believe the dividend is sustainable here, unless Chimera Investment sells assets (and loses associated portfolio income) or its distributable earnings take an unexpected decline.

Dividend (The author created a table using company supplements)

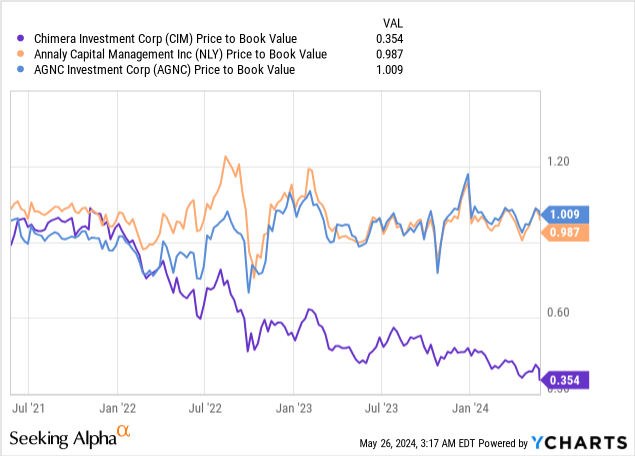

Big discount on the value of the book

A steepening of the yield curve, increased short-term interest rate volatility, and widening spreads for mortgage-backed securities have done real damage to the mortgage real estate investment trust sector in the past couple of years. This pressure on the mortgage funds’ business model has been reflected in significant declines in Chimera Investment’s book value, which is the main reason the stock is selling at such a deep discount right now. The significant dividend cut in 4Q23 is another reason for the significant volume discount.

In Q1 2024, Chimera Investment’s GAAP book value was $7.11 per common share, which is down from $11.44 in Q1 2021. This means that in the past three years, GAAP book value has decreased Generally accepted accounting, which is a measure of Chimera Investment’s intrinsic value, is 38%.

Since Chimera Investment saw its stock price fall significantly as well, the mortgage lender announced a one-for-three reverse stock split that took effect on May 21, 2024. This stock split may improve liquidity in the future.

As a result, Chimera Investment’s discount on book value has risen to more than 50%, making it one of the largest discounts in the market. Analy Capital Management (NLY) And ANC Investment Company (AGNC) It is more focused on higher quality agency investments and has not reduced its payouts recently, which supports higher book value multiples.

Why could I be wrong?

There’s a crucial factor here that passive income investors should take seriously: The central bank may choose to abandon short-term interest rate cuts in 2024 if inflation remains a stubborn issue in the latter half of the year.

Investors have some reason to believe this, as inflation returned to the rise at the beginning of the year. I expect that the central bank will cut short-term interest rates in the fourth quarter, although I could be wrong about this if inflation does not subside.

If the central bank delays interest rate cuts, Chimera Investment may not benefit from lower funding costs in a low interest rate environment. The rerating trigger for the Fund’s MBS assets (which increase in value if interest rates fall) may also be delayed in conjunction with a delay in the central bank’s interest rate cut timeline.

deductive

Chimera Investment just completed a 1-for-3 reverse common stock split. This doesn’t change any of the company’s fundamental metrics, except that the number of shares outstanding has decreased significantly and the stock price has risen proportionately. The goal here is to make Chimera Investment more attractive to investors and potentially improve liquidity.

Fundamentally, the mortgage REIT saw strong performance in the first quarter as well, with Chimera Investment covering its dividend with distributable dividends for the second straight quarter.

If the central bank begins an interest rate cutting cycle in 2024, Chimera Investment will likely face a positive rerating trigger for its underlying MBS portfolio.

With a covered dividend yield of 11% and a significant discount to book value that translates into a high margin of safety, I think Chimera Investment is worth a shot here for passive income investors with an above-average level of risk tolerance.