Buena Vista Images/Digital Vision via Getty Images

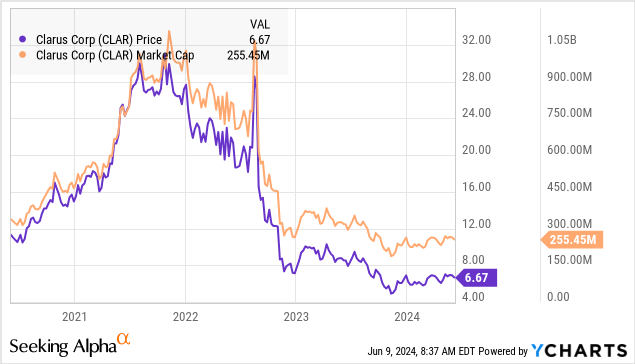

Clarus shares (NASDAQ:CLAR) struggled after a short-lived pandemic-era rally in which shares briefly reached a $1 billion market cap. The stock is down more than 25% over the past year, with the decline even deeper Down from 2021 all-time.

The outdoor and adventure gear specialist, known for its leadership in niche categories such as rock climbing equipment, four-wheel accessories and vehicle roof storage devices, is trying to manage shifting demand and weak sales.

The good news is that some early signs of a turnaround have highlighted the company’s latest results. Efforts to refocus the business towards core strengths to support margins indicate an improving outlook. With a debt-free balance sheet and growing profitability, CLAR is worth a closer look.

CLAR’s Q1 earnings summary

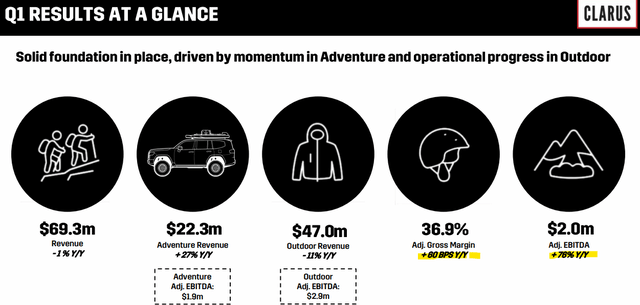

Clarus reported first-quarter earnings in early May, with a GAAP EPS of $0.57, up from $0.04 in the previous quarter. Revenue of $69.3 million decreased 1.3% year over year.

Even with weaker gross profit, the story was a stronger adjusted gross margin of 36.9%, an 80 basis point improvement from Q1 2023. This trend was driven by a changing sales mix and a leaner inventory strategy. The effort to control costs was evident as general and administrative services expenses decreased by 4.1% year over year.

The result is that adjusted EBITDA of $2.0 million in the quarter was up 78% from $1.1 million in the year-ago period.

Source: IR Company

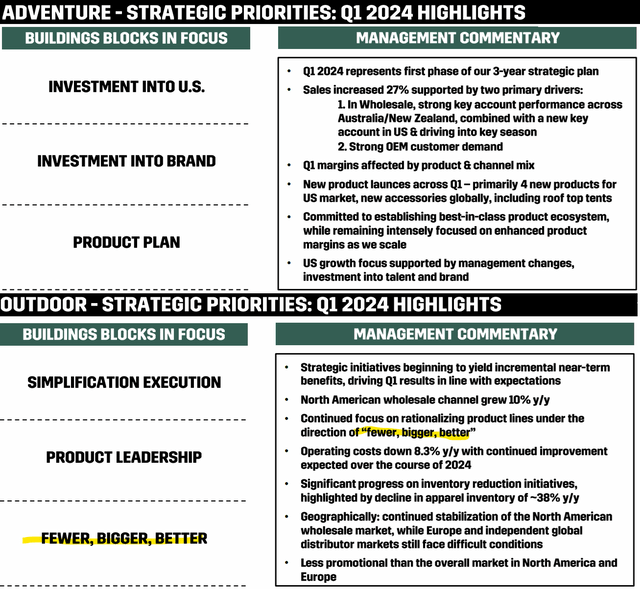

Clarus is trying to make a bigger push into the United States than its historically stronger position in Europe. Domestic sales in the first quarter rose 17%, helping to offset an 11% international decline.

Clarus is trying to move away from the apparel business to prioritize value-added categories instead. This trend falls within the company’s “Less, Bigger, Better” initiative, which is a strategic priority and appears to be paying off. It is worth noting that wholesale activity has rebounded, with signs of improvement emerging in North America.

Source: IR Company

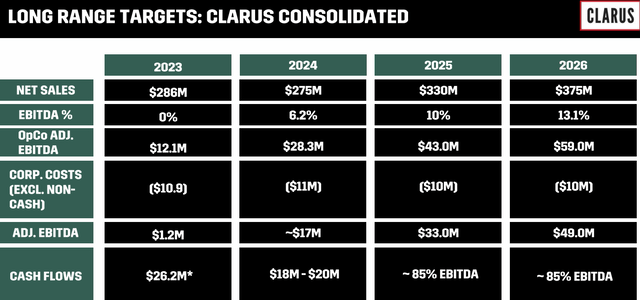

Management’s comments during the earnings conference call were optimistic about improving conditions. In terms of guidance, Clarus is targeting full-year revenue between $270 million and $280 million, representing a 4% decline in mid-2023. This takes into account the continued rationalization of the product mix, with a new round of operational momentum expected to enter in 2025.

More positively, the company expects 2024 adjusted EBITDA to be between $16 million and $18 million, a sharp improvement over a result of $1.2 million in 2023 with higher margins.

Clarus benefits from a strong balance sheet, with $47.5 million in cash and virtually zero debt. Keep in mind that the company also pays a regular quarterly dividend of $0.025 per share, which represents an approximate annual dividend of $4 million, yielding a modest 1.5% yield.

What’s next for CLAR?

When considering where Clarus Corp’s stock price is headed, the first step to a sustained rally would be signs of a growth recovery. Although the company appears to have had some success raising earnings to start 2024, stronger operating momentum will be important as evidence of the health of the brand.

The attraction here is the company’s full exposure to unique product categories in the outdoor and adventure markets. Ultimately, the opportunity is to position itself as a premium consumer choice, combining loyal customers and a reputation for high quality.

Through the strategic initiatives implemented, Clarus has set a target to increase sales by more than 30% until 2026 with higher cash flow conversion and increased profits.

Source: IR Company

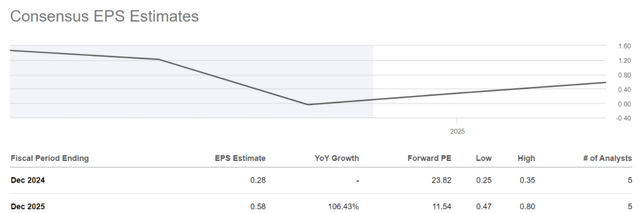

These forecasts begin to shape the current consensus, with the market expecting 2024 EPS to double $0.28 to $0.58 by fiscal 2025.

A one-year forward P/E of 11.5x stands out as compelling for a company with this kind of potential growth momentum. Of course, if this path plays out, the trend could be a strong tailwind for the stock as part of a bullish thesis.

Source: IR Company

At the same time, we believe some caution is warranted given the level of work Clarus has done and still needs to be done. Setting lofty goals is always welcomed by investors, but achieving these goals is easier said than done.

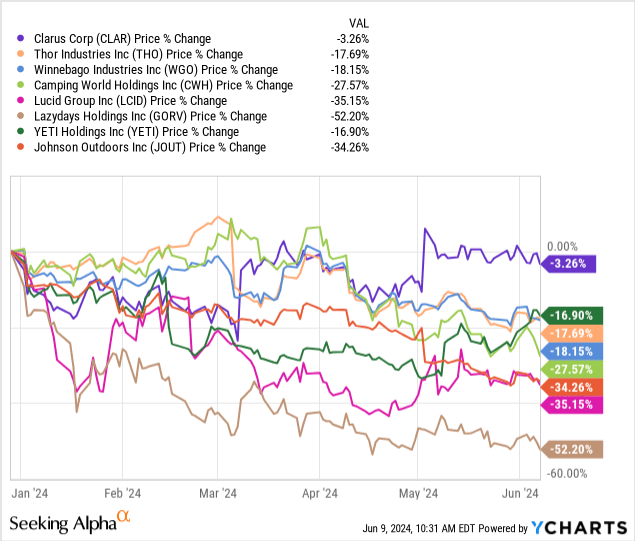

We can point to the challenging background of the related “outdoor lifestyle” such as the recreational vehicle (“RVs”) market, where leaders such as THOR Industries, Inc. (THO) lowered their forecast for annual shipments. The point here is that high interest rates and stubborn inflation continue to squeeze consumer demand for these kinds of discretionary purchases.

Stocks in this sector including names like Camping World Holdings, Inc. (CWH), and Johnson Outdoors Inc. (JOUT), and even YETI Holdings, Inc. (YETI) underperformed the broader market. The risk to consider for Clarus is the potential for economic conditions to deteriorate, forcing a reassessment of the earnings trajectory.

Final thoughts

Clarus is off to a strong start in 2024, but that’s not enough for us to build bullish conviction on the stock.

We would like to see trends continue over the next few quarters to confirm growth has stabilized towards more sustainable profitability. For now, we rate the stock as Hold and will keep it on our radar for signs of stronger trends ahead.