Jacobs Stock Photography Ltd/Digital Vision via Getty Images

Every investor makes mistakes. Sometimes, these are small errors. Other times, it can be quite large. An example of a mistake I made in 2022 was in my analysis Clear Outdoor holding channel (New York Stock Exchange: CCO). For those who don’t know the company, it operates as one of the largest out-of-home advertising companies in the world. The company was larger than it is today. However, in order to streamline operations, the management has sold several international assets. However, by the end of 2023, the company had more than 325,000 print and digital displays spread across 19 different countries.

In theory, this is a market I find very attractive. They are versatile, as such, require very little maintenance and, in theory, their cash flows should be fairly strong. However, such companies tend to do so Take on a large amount of debt in order to promote growth. And that’s exactly what happened here. Of course, I knew this when I was there Books about the company In April of 2022. In this article, I felt as if the pros and cons were well balanced, leading me to rate the company a ‘hold’ to reflect my view that the stock’s performance is likely to be more or less in line with the broader market. However, the stock has actually fallen 51.9% since then, which is much worse than the 19.3% increase the S&P 500 saw over the same time period.

Given this decline, you would think I would finally turn bullish in business. However, while stocks have become cheaper during this time, and while revenues continue to grow at a respectable pace, the bottom lines are showing signs of deterioration. It’s gotten to the point where I think there are definitely better opportunities to be had elsewhere. For this reason, I have decided to downgrade the company to ‘sell’ because I believe the stock will likely underperform the market in the future as well.

When growth isn’t worth it

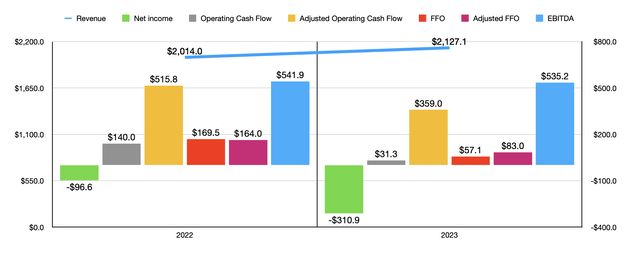

Fundamentally, Clear Channel Outdoor Holdings has been a mixed bag over the past couple of years. First, we should cover the results for fiscal years 2022 and 2023. From 2022 to 2023, the company’s revenue increased 5.6% from $2.01 billion to $2.13 billion. This increase, according to management, was driven by higher revenues in the airport segment, as well as in the Northern European segment with increased demand and as the company continues to invest in digital infrastructure. The company reported some weakness in its Americas segment as a result of pain in the San Francisco/Bay Area market associated with its media/entertainment operations.

Author – SEC EDGAR data

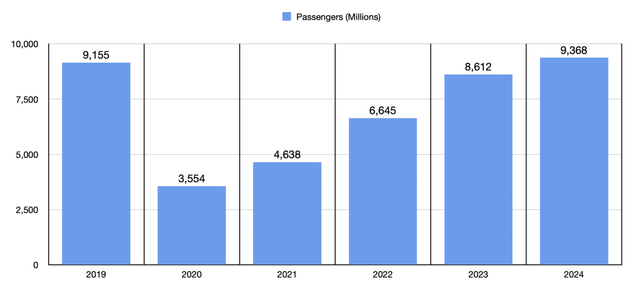

Some of this justifies more detail. For example, let’s look at the airport sector first. During 2023, this segment’s total revenues reached $311.6 million. That was 21.5% higher than the $256.4 million reported for 2022. It was also nearly double the revenue of $160.3 million generated for the segment in 2021. The fact of the matter is that the aviation industry has been severely negatively impacted by the virus. corona. Covid-19 pandemic. This is a topic I have written about before. In the chart below, for example, you can see the global spread during the pandemic compared to before. Naturally, with the pandemic long over, air traffic has returned. In fact, this year is expected to exceed the levels of 2019. So it makes sense that this sector will perform exceptionally well as a result.

Author – Airports Council International

Meanwhile, the Europe & Nordics segment reported revenue growth of 9.4%, with sales rising from $566.1 million in 2022 to $619.6 million last year. This increase was driven by overall strong demand, particularly for the company’s street furniture operations. The deployment of additional digital displays, as well as new contracts, has certainly helped. In fact, management said digital revenue alone jumped 13% year over year. Thus, the amount increased from $299.5 million to $338.4 million.

Although revenues improved well, profitability suffered. Net income fell from negative $96.6 million to negative $310.9 million. Part of this pain can be attributed to interest expenses rising from $360.6 million to $421.4 million. This came as net debt rose from $5.28 billion to $5.38 billion. In addition, the effective interest rate the company had to pay, on a net basis, jumped from 6.87% to 7.83%. This was a result of rising interest rates globally. Even if we took interest expenses out of the equation, the company would be worse off on an annual basis. Depreciation and amortization costs increased from $217.8 million to $241.8 million, other operating expenses increased from $2.1 million to $11.8 million, and decreased tax benefits attributable to continuing operations from $80.4 million to $17.2 million, in addition to other factors. It hit the company’s bottom line quite a bit. It is true that if we excluded discontinued operations, the decline in profits would have been more modest, from negative $47.3 million to negative $157.1 million. But even that is painful to see.

Author – SEC EDGAR data

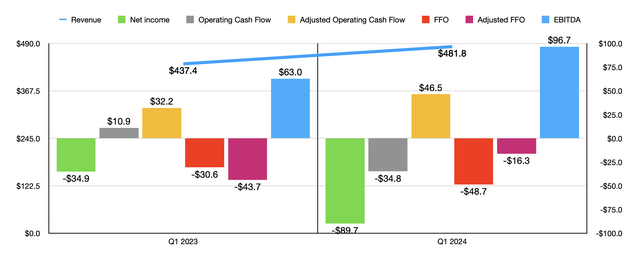

Other measures of the company’s profitability declined across the board. Operating cash flow decreased from $140 million to $31.3 million. If we adjust for changes in working capital, we get a decrease from $515.8 million to $359 million. Funds from operations decreased, from $169.1 million to just $57.1 million. On an adjusted basis, this metric fell from $164 million to $83 million. Finally, EBITDA decreased from $544.9 million to $535.2 million. As you can see in the chart above, the company’s struggles have continued into fiscal year 2024. While revenue increased in the first quarter compared to the same period a year earlier, every one of the company’s profitability metrics, with the exception of adjusted operating cash flow and EBITDA, worsened. On an annual basis.

With results like these, it’s no wonder the stock has taken a hit, too. When it comes to the full fiscal year 2024, management expects revenue between $2.20 billion and $2.26 billion. This should represent a year-on-year improvement of between 3% and 6%. When it comes to profitability, images are also expected to improve, but only marginally. For example, adjusted FFO should be between $80 million and $105 million. Meanwhile, EBITDA is expected to grow to between $550 million and $585 million. These numbers suggest FFO of about $63.6 million and adjusted operating cash flow of about $380.7 million.

Author – SEC EDGAR data

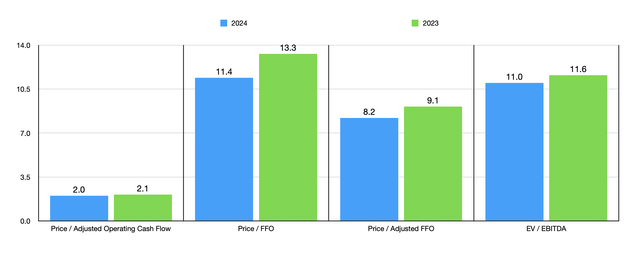

In the chart above, you can see how stocks are priced. Normally, I would consider these levels to be very attractive, especially for a company in this space. But sometimes, a lower multiple is justified. It is worth noting that the shares are still cheap compared to two similar companies, as shown in the table below. On a price-to-operating cash flow basis and on an EV-to-EBITDA basis, Clear Channel Outdoor Holdings ended up being the cheapest of the group.

| a company | Price/operating cash flow | Value added/EBITDA |

| Survey of the external holdings of the canal | 2.1 | 11.6 |

| Lamar Advertising Company (LAMR) | 15.7 | 15.9 |

| External media (out) | 8.8 | 12.6 |

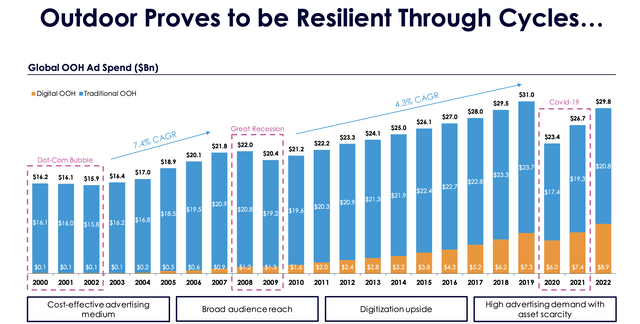

As I wrap up this article, there is something else I would like to touch on briefly. Those who disagree with my decision to downgrade the stock might point out that there is likely to be continued improvement in this area. I agree with this assessment. In fact, we’ve already seen some good improvement, as the image below shows. Global spending on out-of-home advertising peaked at $31 billion in 2019. This represents an annual growth rate of 4.3% from 2010 through 2019. However, industry revenue fell to just $23.4 billion in 2020. Management did not provide data Industry for the year 2023 after. This should come out in September. But by 2022, the industry had recovered and generated $29.8 billion in revenue. Much of this growth has come from traditional out-of-home advertising revenue. However, the company continues to benefit from rapid growth and growing market share associated with digital out-of-home spending. In the long term, I fully expect this trend to continue. But until we see Clear Channel Outdoor Holdings’ bottom line improve, it’s hard to be very optimistic.

Survey of the external holdings of the canal

Away

As much as I hate the idea of downgrading a company that I find attractive from an operational perspective, the fact of the matter is that Clear Channel Outdoor Holdings is highly leveraged and its bottom line is suffering. I would bet that lower interest rates must be somewhat of an upside for the company. But what management should really be doing is paying down the debt. Until we see some improvement in profitability, or some significant debt reduction, I think downgrading the business to ‘sell’ makes sense.