Yuzayo/iStock via Getty Images

the Long/Short Equity Convergence Fund (CLSE) stands out as an actively managed exchange-traded fund, or ETF, that uses an alternative investment strategy typically reserved for institutional investors. The fund invests across a range of stocks while also… Short sell another set of stocks.

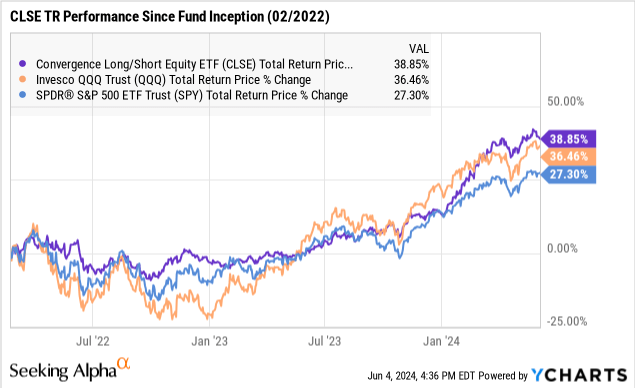

The idea here is to benefit from rising prices for long positions while taking advantage of falling prices for short positions. Impressively, CLSE has managed to outperform both the SPDR S&P 500 ETF (SPY) and the Invesco QQQ Trust (QQQ) since its 2022 listing.

The caveat is that the actual strategy has been operating since 2009 as an institutional fund, where historical data shows it has lagged its benchmark based on cumulative returns over the past five and 10 years.

The fund is doing a good job It is expected to achieve risk-adjusted returns, but there is also room for caution before jumping to any conclusions from its more recent performance.

What is the CLSE ETF?

There is a long history of academic research suggesting that a long-short strategy can generate excess returns “alpha” while reducing downside risk and adding portfolio diversification. There is an understanding that compared to long-only strategies, long-short strategies provide the portfolio manager with more flexibility and opportunities to identify more areas of market imbalances.

The Convergence Long/Short Equity ETF is trying to do this with $106 million in assets under management.

According to the fund, Convergence Investment Partners uses a “proprietary dynamic quantitative model” to identify attractive long and short opportunities. The fund’s goal is to generate long-term capital growth. The group further explains its investment process:

Convergence uses a systematic rating method in a factor-based investing approach. The rating ranks stocks within their industry groups based on relative attractiveness. The strategy invests in stocks that have favorable quantitative scores while short selling those that have poor quantitative scores.

Across the portfolio, its current exposure is approximately 115% long versus a short exposure of 49% using portfolio leverage. The net of these two trends of 65% is guaranteed for a significant amount of cash which is part of the risk management process.

There aren’t many surprises among long positions covering major technology companies including Nvidia Corp (NVDA), Microsoft Corp (MSFT), and Amazon.com Inc (AMZN) as the top long holdings.

On the other hand, short names are becoming more interesting, with convergence looking bearish on Intel Corp (INTC) as the largest short position with a weight of -0.8%. Other short ticks include Texas Instruments Inc (TXN) and Palo Alto Networks Inc (PANW).

With 315 total holdings, the understanding is that individual stock performance will be less important than the overall sector condition and sentiment factors. Keep in mind that as an actively managed strategy, all investments are at the discretion of the investment management team and are subject to change.

CLSE performance

We reported that CLSE in its ETF model has outperformed both SPY and QQQ since the fund became listed in February 2022. With a cumulative return of 38% over this period, the strategy has benefited not only from the ongoing bull market and momentum in stocks , especially this year. year, but also a lower loss in 2022.

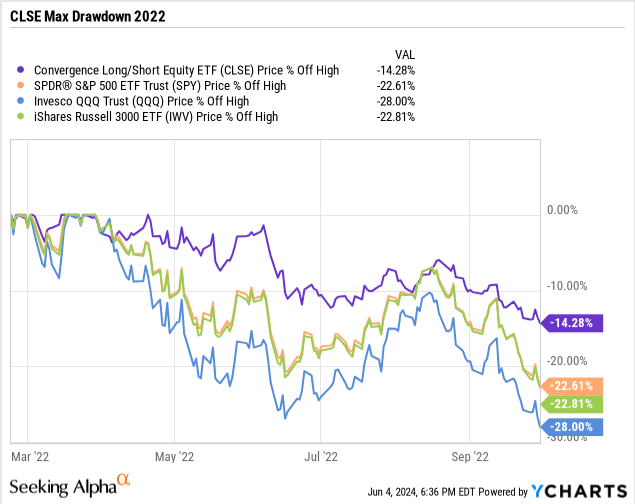

In fact, perhaps the long-short strategy and the Fund’s strongest point is the ability to minimize volatility as major market sell-offs will be offset by gains from short positions.

This dynamic is evident as the CLSE faces a maximum drawdown of 14% in 2022, and about half of the selling saw a decline in QQQ that year, as well as a significant improvement compared to the 23% decline in SPY in the same time frame. By this measure, the CLSE has performed as intended by providing downside protection.

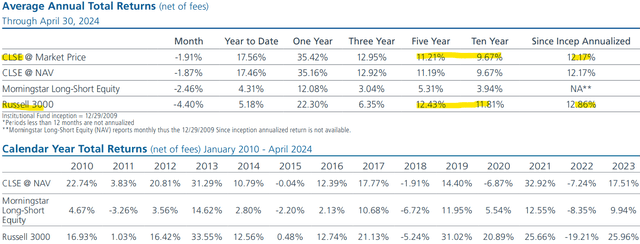

However, focusing solely on ETF performance does not tell the whole story. Convergence shares of institutional fund registry have generated an annualized return of 12.17% from inception in December 2009 through April 30, 2024. This is lower than the 12.86% annualized return the Russell 3000 uses as its benchmark.

The difference is more pronounced and covers a 10-year look-back period, where the fund’s annual return of 9.67% is lower than the Russell 3000 comparison of 11.81%. This may not sound like a lot, but the difference of 214 basis points averaged annually over a decade translates into a spread of about 24% which the CLSE has lagged behind.

On a calendar year return basis, the CLSE strategy has been hit or miss with some years like 2021 and 2022 representing an improvement over the Russell 3000, while it lagged in 2020 and into 2023.

Source: Convergence

Again, total return is not the only metric on which a fund should be analyzed. Sometimes the ability to reduce volatility is just as important, as data such as the 3-year Sharpe ratio of 0.81, which is much higher than the 0.19 in the Russell 3000, indicates the value of the strategy on a risk-adjusted basis.

CLSE also appears to have performed well against the “Morning Star Long-Short Equity” peer group it tracks historically, which at least means the fund is one of the better options in this category. It simply becomes a problem for potential investors to understand exactly what they are getting.

Final thoughts

We expect the CLSE to remain broadly correlated with the market. If stocks rise, there is a good chance of a positive return for the CLSE. A scenario in which the US economy remains resilient with room for interest rates to fall could provide a boost to corporate earnings, triggering the start of the next phase of the bull market.

At the same time, it is unclear whether the CLSE will outperform to the upside given its effective hedging exposure. Conditions since 2023 have played into its strengths, but there is a risk that a market rotation away from growth and technology stocks will lead to a wider tracking spread.

The other consideration here is the fund’s total expense ratio of 1.55%, which includes a management fee of 0.95% plus the cost of short positions of 0.6%. In general, we will need more time to evaluate the value of the CLSE during the next full market cycle. We believe it could be useful to some investors in the context of a broader portfolio strategy as a diversifier in an alternative vehicle.