Monty Racusin

Investment thesis

I recommend selling Companhia Siderúrgica Nacional (New York Stock Exchange: Mr) shares after the release of the results of the first quarter of the year 24 on May 8. The company released weak results, and I don’t see any catalysts for improvement in the short term.

As I said at the beginning of the coverage, the company faces fierce competition from Chinese steel in the domestic market. Another risk is the high leverage of 3.1x, which is much higher than peers who have leverage between 0x and 1x.

Review of the results of Companhia Siderúrgica Nacional in the first quarter of 2024

Companhia Siderúrgica Nacional’s results failed to meet already low market expectations. Revenues were 5.3% lower than expected, and the company reported a loss in the period.

Forecasting (investment)

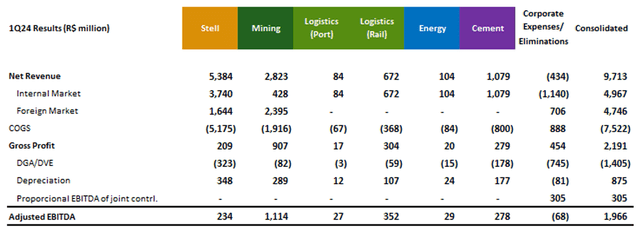

Now we will talk in detail about the company’s results. In my reports, I usually cover revenues, operating results, debt, investments, and profits in a sequence. However, Compania Siderúrgica Nacional It is a holding company and has related businesses such as mining, steel and cement, so I will comment on how the results in each of the companies.

Steel – is no longer the main business of the holding company

It is unbelievable how the corporate divisional sector is suffering, with the mining sector overtaking the steel sector and becoming the largest contributor to EBITDA.

Distribution of the result by sector – general and administrative expenses (DGA) / sales expenses (DGV) (investor relations company)

Before talking about the numbers, it is worth noting that there has been a significant development since my report on the start of coverage. As I mentioned, there was a huge supply problem in the market due to the large amount of steel exported from China to Brazil.

In fact, the government has increased taxes to 25% on Chinese steel, however, the taxes will be applied to only 11 products out of a total of more than 200 products. Moreover, the tariff will be only 25% when a certain export quota is reached.

The limit set was 30% higher than average product imports between 2020 and 2022. In other words, the measures do not meet the expectations of Brazilian producers.

It is interesting to note that the most common commodity China exports to Brazil is flat steel, which is the product to which CSN has the most exposure. This has led the company to sell lower value-added products, such as hot rolled coils (HRC).

Now talking numbers, the sector sold 1,086 kilotons in volume (+2% QoQ; +5.1% YoY). It is interesting to note that the sales volume in the local market amounted to 732 kilotons, down -4.0% QoQ and up +9.0% YoY. However, the year-on-year increase relates to the end of the production bottleneck at the Presidente Vargas (RJ) plant, which affected the first quarter of 2023.

As a result, the division’s EBITDA was $47 million, down -29.3% QoQ and -68.9% YoY. In my opinion, given the macroeconomic situation and the aggressive competitive environment, there is no reason for the operation to contribute again to the result in the short and medium term.

Mining – it was bad too

Companhia Siderúrgica Nacional owns a 79.75% stake in CSN Mineração, a company listed on the Brazilian Stock Exchange, which is consistent with the results of the mining sector.

The deterioration in results was most noticeable in the mining business, which recorded net revenues of $560 million, down -43.9% q-o-q and -31.8% y-o-y. EBITDA suffered a decline of -59.3% q-o-q and -45% y-o-y, to $223 million.

I was actually expecting middling results, as Vale (NYSE:VALE), the giant Brazilian competitor, reported an average result. Both companies are counting on greater economic activity in China to return to reporting strong results.

Logistics and cement – finally, the positive points

Logistics was a positive point, given the good results in the railway logistics sector and the increase in shipment volumes. The cement division also delivered good results, with EBITDA up 6% QoQ and +25% YoY, with lower costs and price adjustments offsetting weaker volumes.

Considerations about results in general

Overall, I don’t think the company chose the right strategy when diversifying its business. It is worth noting that the reason why CSN has much higher leverage than its peers is due to the acquisition of businesses outside the steel and mining sector.

An example is the acquisition of LafargeHolcim’s Brazilian assets, in the cement sector, where the company exceeded net debt/EBITDA by 3x. Although these sectors brought less bad results in the current quarter, the high leverage in the cyclical sector does not appeal to me as a long-term investment.

Rating – Unattractive

At the end of the quarter, the company reached 3.1x net debt/EBITDA, which is much higher than its peers Gerdau (NYSE:GGB) and Usiminas (OTCPK:USNZY) which have the same index between 0x and 1x.

When we look at the P/B index for a company and its peers and take the average, there is no upside to the stock’s value rising. Conversely, there is a premium of 28%, so my recommendation is to sell the stock.

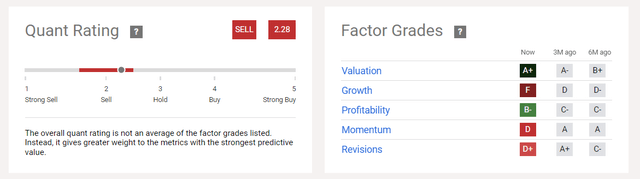

I feel most comfortable with the recommendation when I see that Alpha’s quantitative assessment search tools and factor scores point to the same conclusion.

Quantitative evaluation and factor scores (Searching for Alpha)

In other words, I see no point in buying shares in a company that faces fierce competition from Chinese steel, is highly leveraged, and has a higher valuation premium than its peers.

Potential threats to the bearish thesis

There was little change in the risks to the thesis. The revitalization of the Chinese economy, especially construction, and if this happens, it is possible to redirect a significant portion of Chinese exports to the domestic market, without polluting the market dynamics in countries like Brazil.

The diversification strategy followed by the company may be correct in the long run. It is worth noting that Companhia Siderúrgica Nacional has higher leverage than its peers as it owns cement, logistics and energy companies.

If the medium to long-term scenario in the Brazilian steel sector is truly greater competition with Chinese steel mills, the company will be able to make profits in other businesses to generate shareholder value.

Bottom line

The company trades at a 28% premium in share price to book value compared to peers, and even analyzing the EV/EBITDA multiple, there is no upside potential that would justify a change in recommendation.

The risks to this hypothesis remain the same, as it appears that the surplus supply of Chinese steel in the local market has not ended yet. As a result, the company relies on sectors such as transportation and cement, which are far from representative of overall results.

Based on this analysis, I recommend selling Companhia Siderúrgica Nacional shares. Investors should pay attention to the aggressive competitive environment, high leverage, and little upside potential given the current price.