Matteo Colombo

introduction

What is the wealth composite?

According to Morgan Stanley, it is a very specific type of stock with huge return potential.

Our research shows that these “compounds” exhibit properties such as Strong franchise durability, high, and low cash flow generation Capital intensity and minimum leverageI was born Superior risk-adjusted returns across the economic cycle. – Morgan Stanley (Emphasis added)

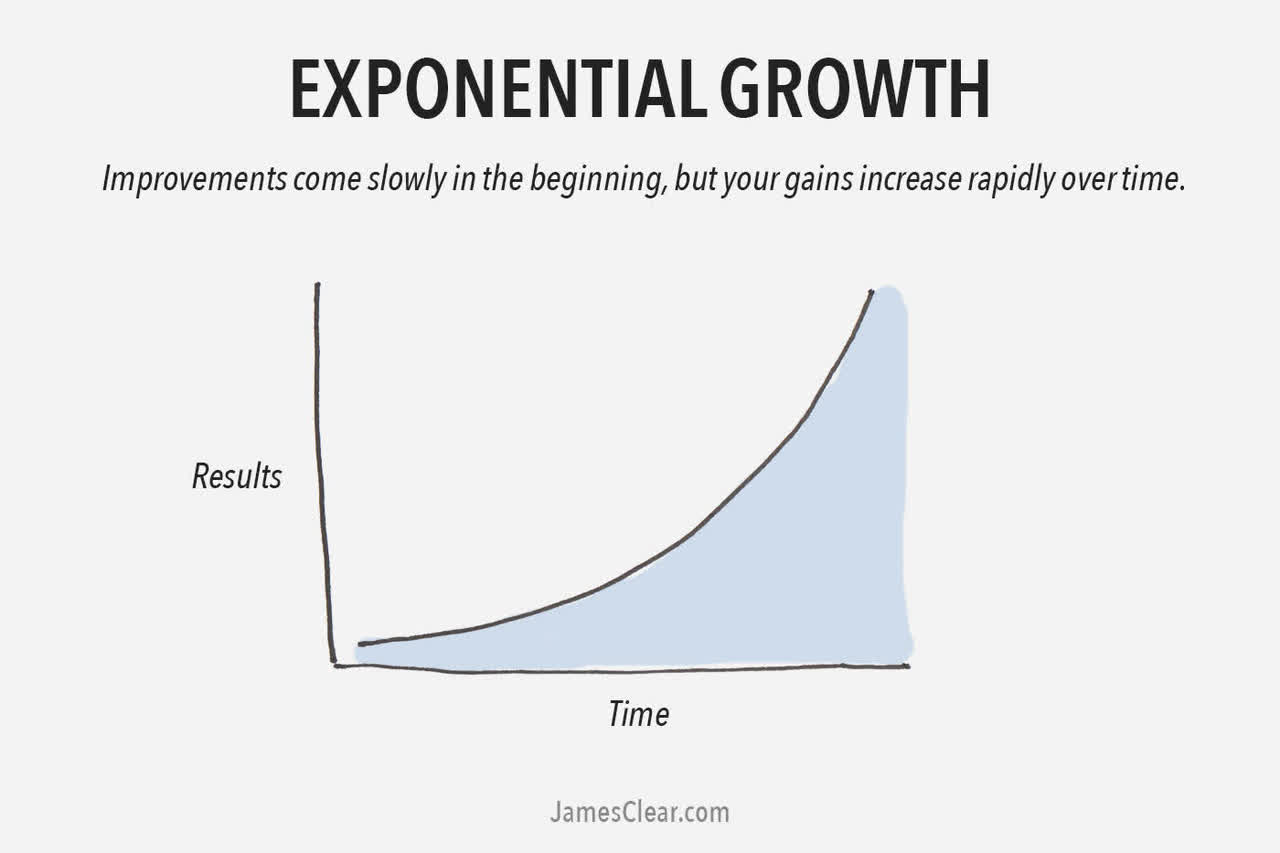

In general, we’re all looking for wealth multipliers – stocks that give us the ability to compound interest, like the exponential curve below.

James Clear

While strategies and financial requirements vary (some investors need higher income, while others can’t afford cyclical risks), it’s all about finding investments that grow our wealth above the rate of inflation and potentially come with higher dividends.

This is the place MSCI (New York Stock Exchange: MSCI) Comes, financial strength begins coverage in 2022.

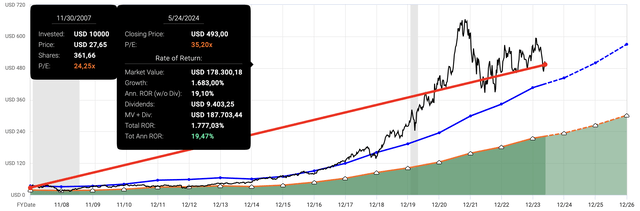

this The wide-moat S&P 500 member has been one of the best composite companies in recent history, returning 19.5% annually since November 2007, when it was spun off from former parent Morgan Stanley (Ms).

Keep in mind that MSCI stands for “Morgan Stanley Capital International.“

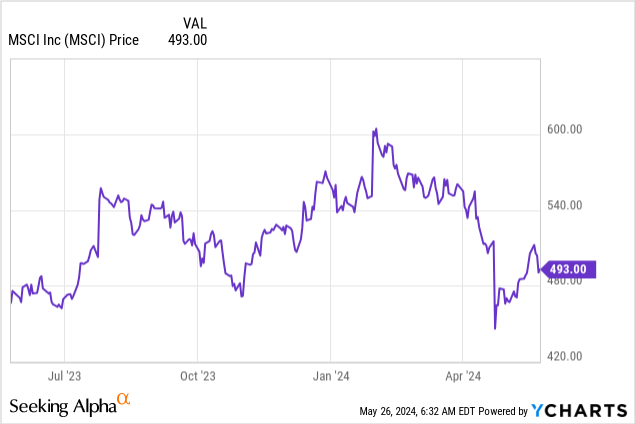

Quick charts

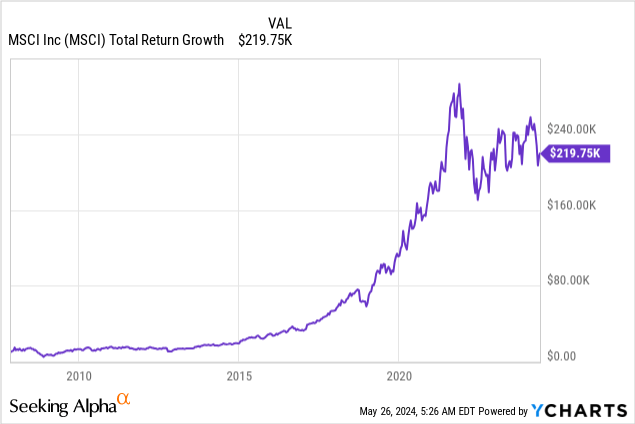

To give you an idea of the size of the deal with a 19.5% annual return, the initial investment of $10,000 after the spin-off would have turned into $219,750.

This is higher than the current median home price in Oklahoma.

Obviously, past returns are meaningless relative to future returns.

If you buy now, it doesn’t matter how much money investors before you made.

However, after publishing my last article on September 13, 2023, it’s time to reconsider the bullish case as the stock has moved sideways since 2021, under the pressure of last month’s earnings release.

So lets get to it!

The wide moat behind MSCI

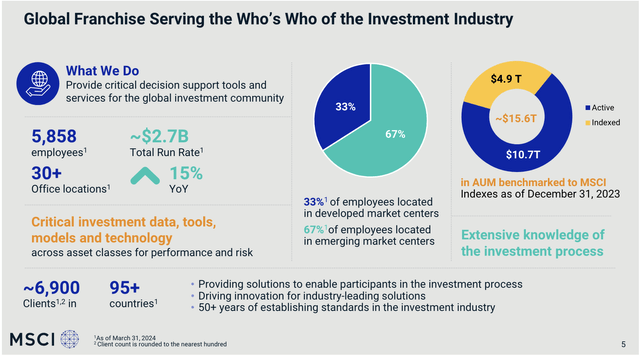

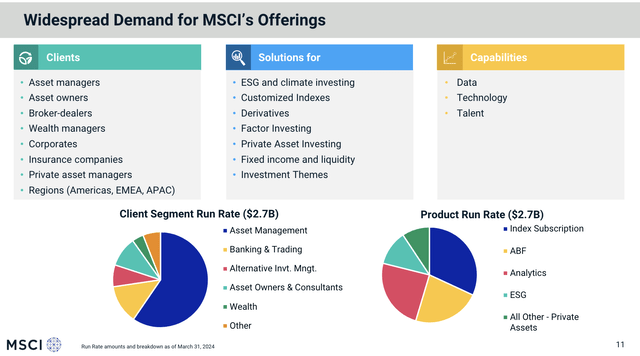

MSCI is a financial giant. However, in an industry dominated by banks, they offer very specific services.

The company’s primary goal is to help investors navigate the many complexities that come with global markets, including leveraging its knowledge of global investment processes, research, data, technology, and portfolio construction.

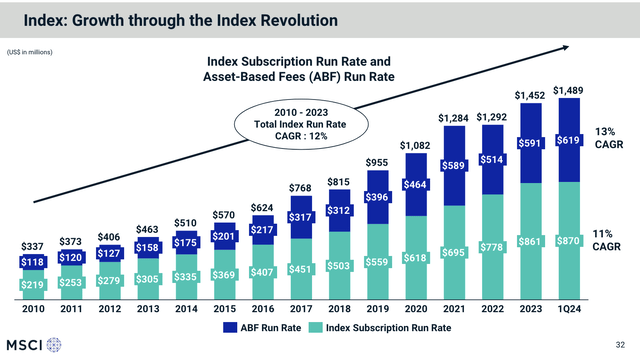

Its product portfolio consists of a number of services that are all benefiting from strong (secular) demand growth.

- Indexes: The company covers global equities, fixed income, ESG, and select thematic investments through its indices. Using the data below, we see that the MSCI indices cover $15.6 trillion in assets!

- Portfolio construction and risk management tools: The company offers advanced risk and performance analytics.

- ESG and climate solutions: MSCI provides insights and tools to integrate sustainability into investment processes.

- Own asset data and analysis: The company helps provide transparency and insights into private market investments.

MSCI Corporation

As of the start of this year, the company had nearly 7,000 clients in more than 95 countries, with BlackRock (BLK) being its largest client, accounting for nearly 10% of its operating revenue.

BlackRock’s revenue is primarily generated through asset-based fees on ETFs and non-ETF products that use MSCI indices.

For example, below:

Black stone

Essentially, MSCI is one of the biggest winners of the global boom in passive investing through ETFs and similar products.

Overall, the company believes it has at least four key factors supporting long-term growth:

- Customer operating models and rapidly evolving business strategies.

- Adopting multi-asset and private-asset investments.

- Continuous integration of ESG and climate-based guidelines.

- Growth of indexed investing and demand for high-quality data.

Although relying on BlackRock may be a risk, the company has a broad business model that benefits from a massive footprint in the index business, as it has benchmarks that have become cornerstones of the financial industry, including the MSCI ACWI Index and the MSCI Index. Emerging markets index.

MSCI Corporation

In addition to the growing interest in passive investing in ETFs, investors need benchmarks to compare their performance – often using unique benchmarks for specific purposes.

MSCI Corporation

Moreover, regardless of someone’s opinion on ESG investing (I’m very critical of it), the company uses so many indicators and has such a good reputation and strong relationships that it is difficult for competitors to gain market share.

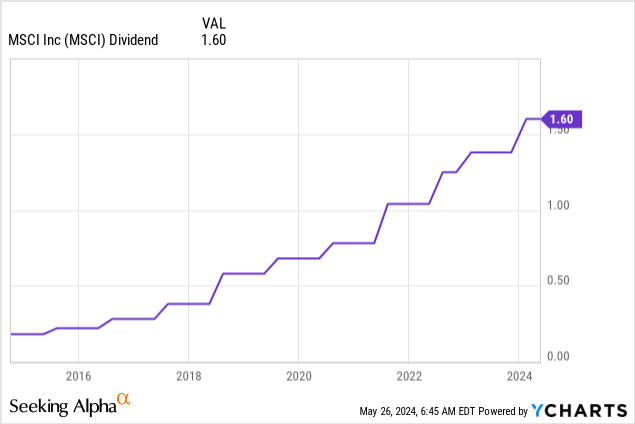

MSCI Dividends

In terms of total return, the company’s business has been supported by strong dividend growth.

After raising its dividend 16% in January, it currently pays $1.60 per share per quarter. This translates to a return of 1.3%.

Although a 1.3% yield is nothing to write home about, we need to keep a few things in mind.

- Dividends come with a payout ratio in the low 40% range.

- Earnings are at a five-year CAGR of 20.8%!

- The dividend has been increased every year since the dividend began.

In other words, the only reason MSCI is not a high-yield stock is because the market always makes sure that earnings growth is offset by capital gains.

This is not a bad thing, unless you require a high income. In this case, MSCI is probably the wrong stock for you.

Fuel behind 20% annual returns.

The strong business model has translated into impressive growth rates.

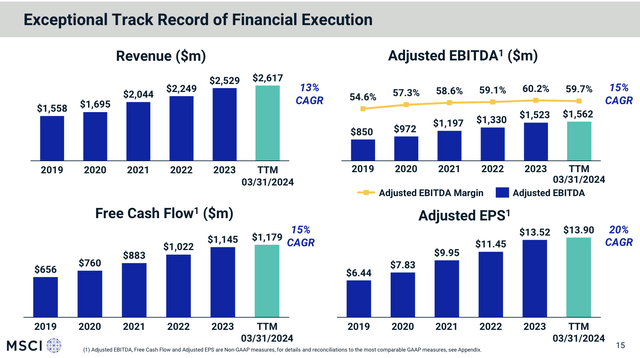

Using the data below, we see that the company has doubled its revenue by 13% annually since 2019.

Thanks to higher margins (it adjusted EBITDA margins in the high 50% range), it has been able to double adjusted EPS by 20% annually since 2019.

MSCI Corporation

To maintain high growth, the company uses its market leadership to improve innovation and meet evolving customer needs.

For example, during the Barclays Americas Select Franchise conference this month, the company noted that it is accelerating the development of new products across its segments, including AI-driven analytics.

And this is paying off.

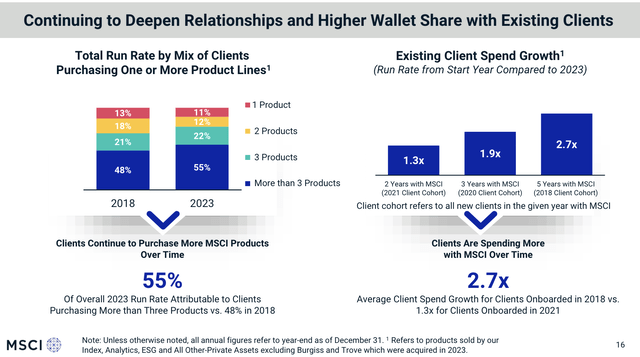

Since 2018, the number of customers using multiple MSCI products has increased significantly, with 77% using three or more products (up from 69%).

Moreover, average customer spending has increased significantly.

MSCI Corporation

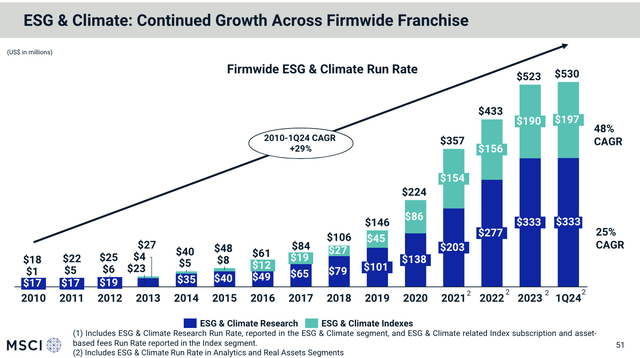

Growth metrics also focus on environmental, social, governance and climate solutions.

While global political shifts can act as headwinds to environmental, social, and governance (ESG) adoption, the company is seeing strong demand for its solutions, with climate-related products representing nearly 20% of the company’s total ESG run rate, with growth By 40%.

Demand for its solutions is particularly strong in Europe.

MSCI Corporation

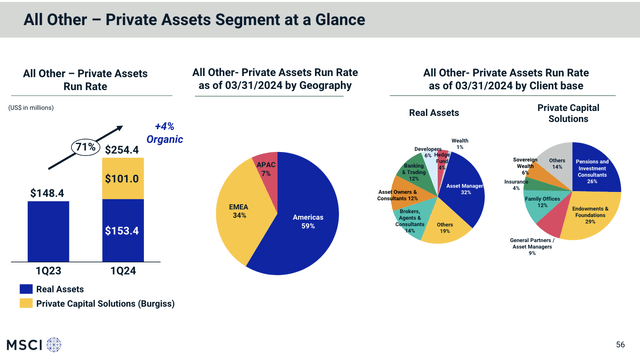

In addition, MSCI is diversifying into the private assets market.

This includes the acquisition of Burgess, which has strengthened MSCI’s capabilities in providing private market portfolio coverage – dealing mainly with institutional investors and asset owners.

With over 35 years of experience in alternative investments, Burgiss delivers private asset data, analytics and software applications, including leading research-quality performance data dating back to 1978. The Burgiss data set covers more than 13,000 private equity funds around the world, It represents 15 US dollars. $1 trillion of cumulative investments in private equity, private real estate, private debt, infrastructure, and natural resources in 195 countries. -MSCI

MSCI Corporation

So, what does this mean for shareholders?

How much shareholder value is left?

Despite returning 20% annually since its spin-off, the company has taken a sideways trend since 2021. It is currently 27% below its all-time high and is down 13% year to date.

This is partly due to the first quarter 2024 earnings report, although MSCI shares have recovered significantly since then.

Essentially, in the first quarter of 2024, the company reported 10% organic revenue growth, 12% adjusted EPS, and 14% higher free cash flow.

While these numbers aren’t bad, they were lower than expected, under the pressure of weak recurring sales (new recurring sales were flat year over year).

Overall, the industry is under pressure due to market volatility, interest rate uncertainty, and pressure on investment firms – especially active managers.

This included a major cancellation of $7 million from a major client, which was related to the merger of two major banks in Europe (we can assume that this is Credit Suisse and UBS).

Readers who frequently read my articles know that I worry about inflation and interest rates, too.

Although I am optimistic about MSCI’s future, this is not a great environment for the “average” investor, especially those who invest in ETFs.

Although I don’t expect MSCI to have problems, it will likely see “lower” growth rates, which could suppress its stock price.

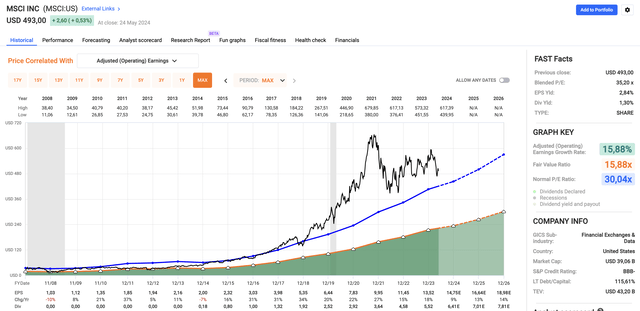

Using the FactSet data in the chart below, MSCI is currently trading at a blended P/E ratio of 35.2 times.

- The company has a normal P/E ratio of 30.0x, which means it is trading at a premium.

- Analysts expect the company to average annual EPS growth of 12% in 2024-2026.

Quick charts

I think these growth rates are too low to justify a 37x earnings multiple.

Rather, I would point out that a 30x multiple requires higher growth rates.

He said I’m sticking to me He buys evaluation.

Even if we use a 30x multiple, the company has a fair share price of $567 using 2026E EPS of $18.89. This means an increase of 15%.

With all this in mind, investors who believe MSCI is a good fit for their portfolios may be better off buying gradually. If the economy remains in a difficult situation, we may see more downside, allowing investors to average lower.

However, given MSCI’s growth potential, all the good news is likely to send the stock price higher.

Depending on one’s strategy and time horizon, I think the MSCI is a great long-term investment. It is a bit difficult to deal with short-term evaluation.

Away

MSCI is an excellent example of a wealth compound, returning 20% annually since its spin-off.

As a financial powerhouse focused on global market services, MSCI benefits from diverse revenue streams, from index services to ESG solutions and private asset data analysis.

While recent market volatility and macroeconomic challenges may have turned into headwinds, MSCI’s strong fundamentals and growth initiatives point to a promising growth outlook – slightly lower compared to previous years.

With advanced investment strategies and an eye on long-term value, MSCI remains a compelling choice for investors seeking sustainable wealth accumulation.

However, investors need to keep an eye on its valuation, as short-term returns could be disappointing if headwinds remain strong.

Pros and Cons

Positives:

- Continuous growth: MSCI has a track record of 19.5% annual returns since its spin-off. While this does not guarantee future returns, the company has found a great way to grow.

- Diverse revenue sources: From index services to ESG solutions, MSCI’s diverse portfolio comes with a wide range of unique capabilities.

- Market leadership: With benchmark indices covering $15.6 trillion in assets, MSCI’s dominance comes with broad characteristics.

- Earnings growth: Earnings come at a five-year compound annual growth rate of 20.8%, with long-term growth potential in the double digits.

cons:

- Market volatility: Recent volatility and macroeconomic headwinds are putting pressure on revenue growth.

- Client dependency: While the relationship with BlackRock is profitable, this dependence may come with headwinds in the future.

- Evaluation concerns: MSCI trades at a premium with a P/E ratio of 35.2 times, and MSCI faces challenges justifying its valuation, which means there is little room for error.