Don’t go

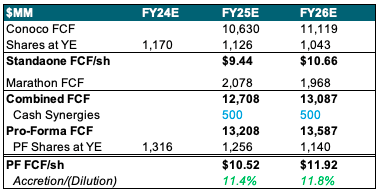

Having previously remained on the sidelines in the ongoing consolidation, on May 29, ConocoPhillips (New York Stock Exchange:COPAnnounced the acquisition of mid-sized shale company E&P Marathon Oil (MRO), increasing production to 2.2 million boe with initial US production The share rose 3 percentage points to 72%. The total consideration would be $22.5 billion with Conoco assuming $5.4 billion of outstanding debt and exchanging 0.2555 shares per share of Marathon Oil, meaning the former Marathon owners own about 11% of the combined entity. Deal multiples look promising as Marathon has historically traded at a discount while Conoco is valued at the high end of its US exploration and production operations. Combined with $500M of synergies expected to be achieved by YE25, I see higher directed share repurchases ($7B for 25E from $5B previously) to provide ~11.4% FCF/sh accretion for 25E, rising to ~11.8% by 26E.

I love the deal and I remain overweight ConocoPhillips shares an unchanged price target of $133 (see my previous article for more color on Conoco here). Key risks remain weaker commodity markets, unexpected maintenance outages, and unfavorable political developments in international assets. Merger-specific risks include integration challenges, failure to achieve expected synergy objectives, and regulatory interference.

(Note: Similar transactions are Exxon (XOM) – Pioneer (PXD), Chevron (CVX) – Hess (HES), Diamondback (FANG) – Endeavor and Occidental (OXY) – Crownrock. All information and expectations regarding the merger from Conoco Investor Financial Presentation for Marathon Oil from the most recent 10-K.)

Key discussion points

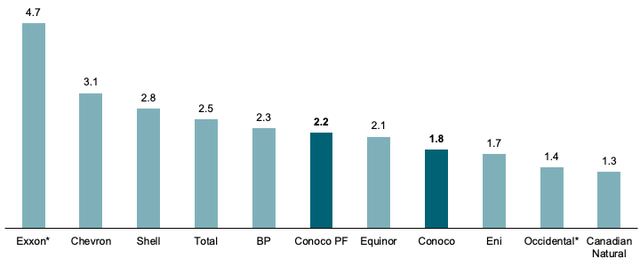

The deal boosts Conoco’s oil and gas production by a quarter and increases the US share of production to 72%.. Adding 0.4 MBoe of daily Marathon production, Conoco’s initial production will increase by almost a quarter to 2.2 MBe based on FY23 figures, putting it ahead of Norway’s Equinor (EQNR). The pro-forma entity also appears poised to overtake BP (BP) for fifth place during 25E as the British major is likely to keep production stable while additional volume increases at Conoco and Marathon should push combined production to ~2.4Mboed. With management not revising its production forecast of 4-5% annual production growth, Conoco should also outperform TotalEnergies (TTE) (about 2-3% annual growth target) by the end of the decade to take fourth place, behind Shell Just. (SHEL) and US Majors (XOM) (CVX). I value this unique position as the only fully upstream-focused independent among a range of integrations to drive scarcity value and increase valuation premiums for remaining exploration and production peers.

Largest oil and gas producers by FY23 production (excluding NOCs/Exxon and OxyPro Forma) (Bloomberg)

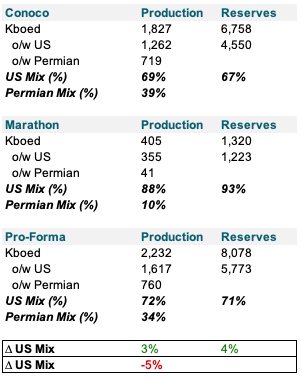

Besides providing additional scale in an industry that relies heavily on volume, the Marathon acquisition also increases Conoco’s relative exposure to U.S.-based production, which investors generally view favorably given the high political stability and positive framing of oil producers. Based on FY23 numbers, I see that the pro forma entity contributed approximately 72% of its production through domestic assets (lower 48+ Alaska), a gain of about 3 percentage points. For reserves, the share rises by 4 percentage points to about 71%.

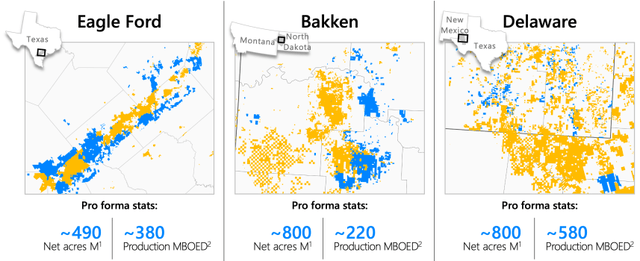

However, it should be noted that Conoco’s share of Permian Basin production actually declines by a significant 5 percentage points from 39% to 34% due to Marathon’s relative lack of exposure to the basin. By increasing daily trading volume by 41,000 boe, initial Permian production would rise by just 5% while production from the Eagle Ford and Bakken would rise by 66% and more than 100%, respectively. It was also noted that the deal does not add any acreage or production in the Midland region, a key area of focus in recent deals (Exxon/Pioneer, Diamondback/Endeavor) and one in which Conoco remains small (about 160,000 boe versus about 500,000). barrels of oil equivalent from last year). Delaware).

Company files

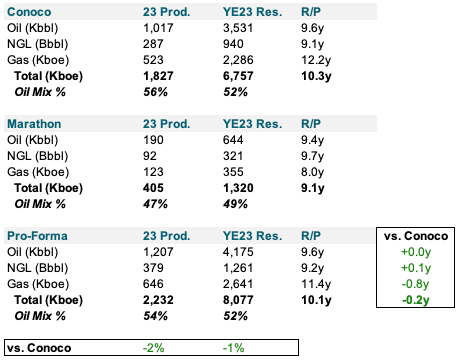

With Marathon’s production mix weighted slightly less toward oil due to gas development in Equatorial Guinea and generally higher shares of associated gas and NGLs for its shale assets versus Conoco’s mixed shale/conventional footprint, the pro forma oil share fell by 2 percent points. However, I note that the vast majority of EG Marathon gas production is distributed to joint ventures associated with LNG production for European end markets. Reserve life remains largely unchanged with a slight reduction in P/E ratio of 10.1 years as higher liquids life is offset marginally by lower gas coverage.

Company files

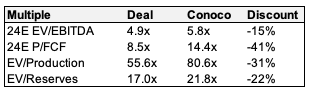

Multiples are showing favorably against Conoco’s trading and recent large E&P transactions. By acquiring Marathon at multiples of 4.9x on 24E EBITDA and 8.5x on 24E FCF, Conoco appears to be continuing its excellent recent history when it comes to financial terms in dealmaking. Compared to Conoco’s own trades, this represents a discount of approximately 15% and approximately 41%, respectively. As a general rule, for all-stock transactions, the deal is usually accretive if the buyer’s multiple is higher than that at which the target purchased it. Financial conditions also look favorable by oil-specific metrics, with Conoco paying about $56 per barrel of flow and about $17 per barrel of proven reserves, 31% and 22% below its trades, respectively. I note that Conoco has long traded at a premium to the broader U.S. E&P space due to its superior size, while Marathon has been valued significantly below its peers, in part due to a lack of exposure to the Permian Basin, so the entire stock deal represents a structural… Attractive.

Company Files, Bloomberg

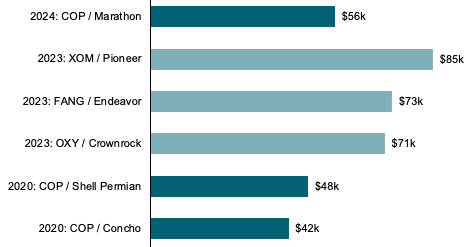

The acquisition price also appears to be very reasonable compared to other recent deals and aligns well with Conoco’s previous deals for Shell’s Permian assets and Concho Resources, both of which it concluded during the low price environment of 2020. At around US$56,000 per unit of Marathon’s 2023 daily production, the deal ranks Higher than Concho and Shell’s transactions but well below recent large E&P deals that averaged around $75K/boe.

EV per barrel flowing for recent large E&P deals (Company Files, Bloomberg)

However, I note that there are significant differences between the acquired operators, both in terms of profitability and space. While Pioneer, Endeavor and Crownrock are unconventional drillers in the Permian, Marathon has relatively low exposure to the Permian with a significant share of production assets located in shale in the Eagle Ford and Bakken. Marathon is also the only recently acquired company with some sort of international exposure through its gas assets and LNG-related joint ventures. While acknowledging these differences, the Marathon probably won’t come off as the kind of deal that the headline numbers suggest, however I still find the deal to be very reasonably priced.

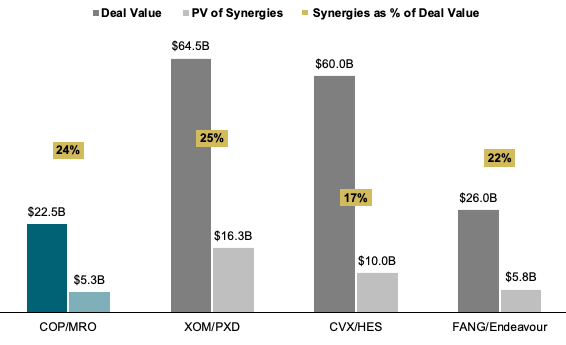

At a run rate of $500 million, synergies will represent approximately 24% of the deal value, in line with the Exxon and Diamondback deals.. Management expects significant synergy potential between the two entities, resulting in targeted savings of $500 million by 2025. Nearly half of the expected cost synergies will be driven by eliminating duplicative efficiencies and redundancies in general and administrative (G&A) functions such as streamlining and integrating resource departments Human, financial and legal at Marathon. $150 million in potential operating cost savings has been identified, with a focus on consolidating aboveground and belowground operations in adjacent parcels across the Permian Basin, Bakken and Eagle Ford, with the largest impact likely to be concentrated in the Eagle Ford. The remaining $100 million is related to capital optimization, with the goal of optimizing Marathon’s legacy D&C cost by leveraging Conoco’s scale.

Conoco IR

Assuming management’s target for synergies at $500 million from 25E onwards with zero future growth and a discount at Conoco’s weighted average cost of capital of ~10%, I estimate the present value of the synergies at ~$5.3 billion, which represents ~24 % of total consideration of $22.5 billion. Compared to recent large US exploration and production deals, this deal ranks among the most synergistic, behind only Exxon’s purchase of Pioneer and ahead of Diamondback/Endeavour and Chevron/Hess.

Company filings, WSR estimates

At current 2025 estimates, Marathon could provide a ~11.4% increase in FCF/sh, rising to ~11.8% by 26E. With closing expected during 4Q24, I expect the deal to be highly accretive to FCF/sh by year 1, driven by the relative undervaluation of Marathon versus Conoco. With total free cash flow of $12.7 billion and assuming the full $500 million of synergies are realized as management expected, this implies pro forma cash flow of $13.2 billion or ~$10.52 per share, compared to ~9.44 USD to Conoco Independent. Management also increased its 25E repurchase guidance by approximately 50% from $5 billion to $7 billion, which, at current pro forma market value, could reduce shares outstanding by approximately 4.6% versus approximately 3.7% under the old repurchase plan and market value. Independent. Estimating the $7B pace to continue through 26E I see Conoco retiring up to 9.2% of initial equity through YE26, resulting in an accretion of 11.8% FCF/sh for the year.

Company filings, WSR estimates