urbazon

Macro context

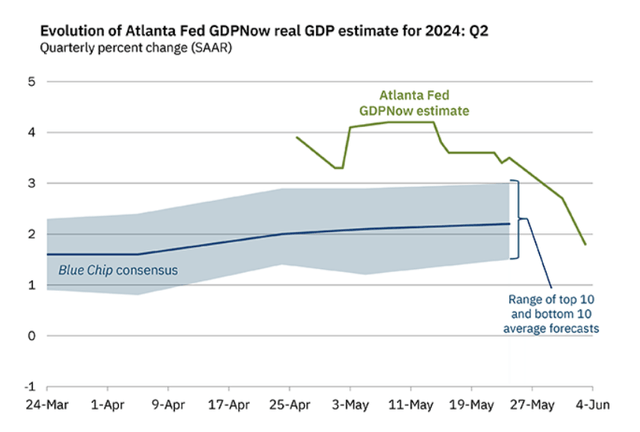

Recent data shows that the US economy is slowing sharply. Atlanta’s Q2 GDP rating was downgraded from more than 4% to 1.8% in just a few weeks.

GDP now (Federal Reserve Bank of Atlanta)

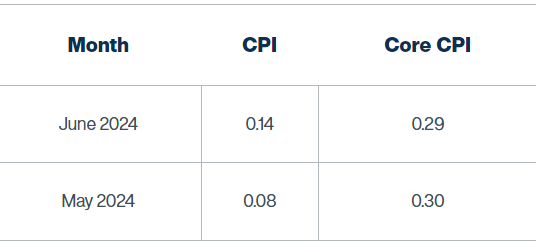

Meanwhile, inflation remains steady well above the Fed’s 2% target. The May CPI inflation report is expected to confirm this, by showing a 0.3% month-on-month increase in core CPI, which equates to about 3.6% of annual core CPI inflation.

Thus, the Fed should seriously consider lowering interest rates, as the economy is clearly heading toward a recession, perhaps even in the third quarter. However, due to stable and high inflation, the Fed is unable to start lowering interest rates. As a result, the economy is likely to continue to slow until growth turns negative and the unemployment rate begins to rise – that is the hard landing Scenario. In other words, the Fed will be forced to keep policy tight until a recession comes due to stable and high inflation.

Thus, the S&P 500 (SP500) is facing a stagnant bear market. Given the high valuation, with a P/E ratio of 22, and irrationally high earnings expectations, the S&P 500 could face a deep 20%+ decline, which could be much deeper if the real estate bubble bursts with a systemic credit event.

May CPI Report: Inflation High and Stable

The key piece of the macro context puzzle is stable and high inflation, which prevents the Fed from preemptively cutting interest rates and engineering a soft landing (falling inflation short of a recession).

As mentioned previously, the Fed’s inflation target is 2% as measured by core personal consumption expenditures inflation, which is used to calculate GDP.

However, the market uses the inflation measure in the CPI for inflation-adjusted transactions and even for pricing TIPS. Core CPI inflation is typically about 0.5% higher than core PCE inflation. Therefore, the Fed will consider a core CPI of 2.5% to be an acceptable level of price stability. An annual core CPI inflation rate of 2.5% requires the monthly core CPI inflation rate to average 0.2% per month.

The Fed’s Inflation Nowcast expects the monthly core CPI for May and June to reach 0.3% from the previous month – this corresponds to approximately 3.6% of the annual core CPI, well above the Fed’s target.

Real-time inflation expectations (Federal Reserve Bank of Cleveland)

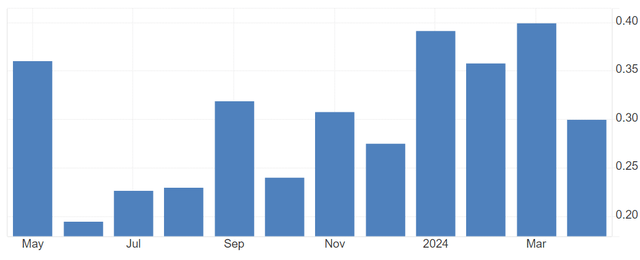

The monthly core CPI for April was also 0.3%, and even higher at 0.4% for January, February and March, as the chart below shows. Therefore, it is clear that the core CPI is between 3.5% and 4%.

Core consumer price index monthly (Economics of Trade)

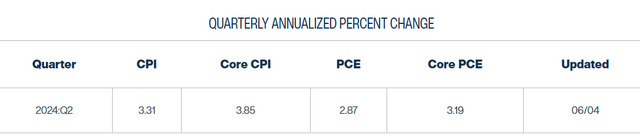

In fact, the quarterly core CPI inflation rate is 3.85%, while the quarterly core PCE inflation rate is 3.19%. These inflation readings are clearly well above the Fed’s target. Importantly, monthly inflation readings appear to have been fairly steady since September 2023 – meaning “inflation is high and stable.” This is the problem the Fed faces, especially now that the economy has begun to slow sharply.

Federal Reserve Bank of Cleveland

The Fed needs to see core CPI at 0.2% per month for several months before it starts cutting interest rates — and we’re not even close to that point yet.

What makes the core CPI high and stable?

The main reason for flat and high core inflation is inflation in services excluding energy; Which is weighted heavily in the overall CPI, has risen 0.4-0.5% m/m over the past three months, and is up 5.3% y/y.

Within services inflation excluding energy, the key is shelter inflation, which rose 0.4% month-on-month over the past three months, and is up 5.5% year-on-year.

Also, within this category, transportation costs rose sharply by 11% year over year, and this includes car insurance, as well as car repair costs.

So, let’s focus on shelter inflation. Many analysts, including the Fed, point out that the shelter inflation measure does not reflect current market rents, which are either falling or rising at a much lower rate. Thus, the Fed is confident that shelter inflation will eventually moderate.

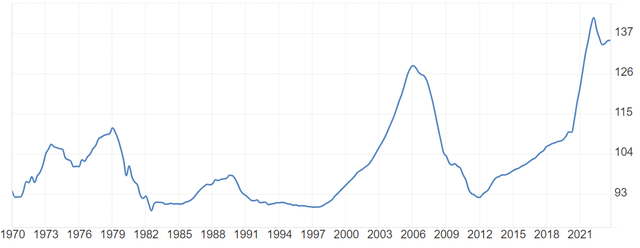

However, empirical evidence actually links OER shelter rent to housing prices, and housing prices continue to rise. In fact, the housing-to-rent ratio is near record levels, and unless housing prices fall, rents will continue to rise.

Price to rent (Economics of Trade)

Thus, the key point is that as long as housing prices remain high, housing inflation will remain constant. At the same time, falling housing prices could lead to a deep recession, with the possibility of a systemic credit event. This is the choice the Fed faces: either allow housing to remain high, or induce a housing market correction and recession – a situation more like the crisis that preceded the 2008 financial crisis.

Other sources and measures of inflation

Inflation can also be measured in real time with commodity prices, and recently metal prices (copper, aluminium, silver, gold and platinum) have risen. The price of crude oil is currently falling due to Biden’s efforts to calm the geopolitical situation in the Middle East before the elections. But, how long can this last? What happens after the elections?

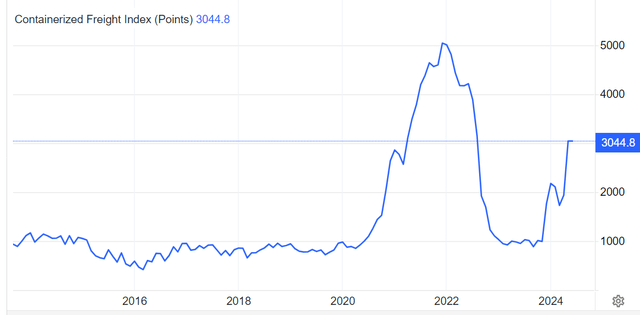

But more importantly, the container freight index has been rising over the past few weeks, approaching the peak of the pandemic when ports were closed due to coronavirus lockdowns. Why are shipping costs rising now? This is due to the geopolitical situation.

Trading economics

We are experiencing an accelerating process of deglobalization, as opposing blocs compete to erect trade barriers. There are two real proxy wars, with conflict brewing in a few places, most notably in Taiwan.

Deglobalization leads to stagflation, and that is precisely what the data showed: flat and high inflation, and slow growth.

Ramifications

Core CPI for May is expected to come in at 0.3% monthly, which is consistent with an annual inflation rate of approximately 3.6%, and consistent with the recent trend of flat and rising inflation. The Fed is therefore unable to begin cutting interest rates and preemptively respond to a severe economic slowdown to avoid a recession.

Thus, the economy is likely to enter a recession over the coming quarters, meaning the S&P 500 is facing a sluggish bear market. A potential housing market correction could deepen the decline in a bear market.