Hiroshi Watanabe

thesis

Calamos Investments is a well-known manager for its closed-end funds of convertible securities, but now it is making a push into the ETF space, specifically into the “buffer ETFs” space:

Buffer ETFs are funds that seek To provide investors with upside in asset returns (generally up to a specified percentage) while also providing downside protection The first is a predetermined percentage of losses.

Source: Charles Schwab

According to Charles Schwab, buffer ETFs have become one of the fastest growing corners of the ETF market, with more than $27 billion in assets under management for this strategy.

Calamos S&P 500 Structured Alternative Protection ETF – May (NYSEARCA:CPSM) is one of the funds that falls under the umbrella of the “Buffer ETF” strategy. Unlike other names, Calamos Fund provides 100% downside protection:

Calamos Structural Protection ETFs are designed to Matches the positive price return of the S&P 500® Index up to a specified maximum while protecting against 100% of losses over a one-year period (before fees and expenses).

In this article, we’ll take an in-depth look at CPSM, its structure and return profile, and highlight why it’s a very solid fund to buy for equity exposure in today’s extended markets.

What does CPSM actually do?

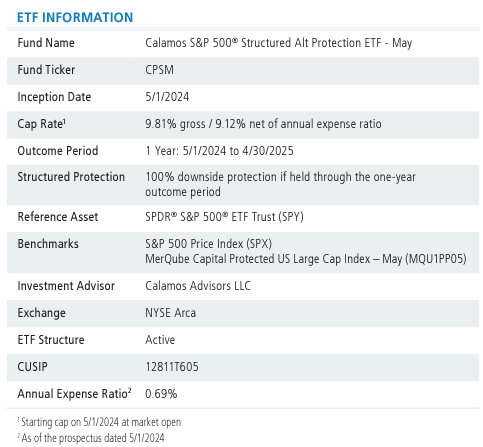

The CPSM aims to track the S&P 500 over a one-year outcome period, with an upside limit of 9.81%. So, as an investor, you will never make more than 9.81% during the outcome period, but at the same time the fund protects 100% of your downside – that is, you will not lose money. The worst case scenario here is a return of 0% minus the fund’s expense ratio of 0.69%:

Information (fund website)

The Outcome Period ends on April 30, 2025, and the Fund’s initial public offering price is $25 per share.

In the best-case scenario, an investor can make 9.81% minus the expense ratio, while no increases are recorded in the S&P 500 above this level.

How does CPSM actually do this?

Many retail investors may be puzzled by the ongoing financial engineering and want to understand how it can be achieved. Let us walk you through how the fund achieved its goal.

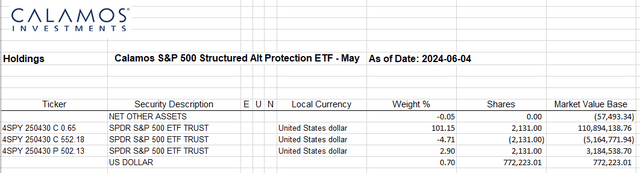

If a retail investor goes to the ETF’s website, they can find current holdings:

Holding (Fund website)

One will notice that the fund held a very high delta strike call of 0.65 (long), sold the 552 strike call, and bought the 502 strike call. It is worth noting that the S&P 500 was at 502 on the first day of the results period, i.e. May 1, 2024.

The Fund can therefore fully protect the downside by purchasing, which was partially funded from the call sold at 552. The investor should understand though that these options are not standard US options traded on the NYSE, but are designated “flexible options”:

The Fund is designed to provide point-to-point exposure to the price return of a benchmark asset via a basket of Flex options. As a result, the ETF is not expected to move directly in line with the Reference Asset during the interim period. Investors who purchase shares after the start of the Outcome Period may experience results that are significantly different from the Fund’s investment objective. The initial results periods are approximately one year starting from the date of the fund’s establishment. Following the initial Outcomes Period, each subsequent Outcomes Period will begin on the first day of the month in which the Fund was established. After the results period ends, another period will begin.

Flexible options are a designated European option (i.e. they can only be exercised on their maturity date) and their mark-to-market will be different from a standard exchange-traded option. So the pricing is more advantageous. Hence, a manager can consider taking advantage of market skew to fully protect the downside.

Now let’s see how different the prices of Flexible Options are versus American Options. If we currently look at the market, we can measure the current pricing at at-the-money puts, and 9% of at-the-money calls:

- June 20, 2025 The $530 strike cost is $23.5 per contract.

- June 20, 2025 580 strike calls (9.1% upside) cost $18.5 per contract

- So the net cost is 23.5-18.5, which equates to $5 per contract

A retail investor with a position in SPY now needs to spend $500 for every $53,000 notional in order to fully protect the downside while limiting the upside to 9.1%. This is the cost across US options currently traded on the NYSE. Furthermore, you cannot buy deep into the money call options, with a higher delta bid of 150.

Flexible options are custom contracts that allow for better pricing given their discrete exercise history and unique features. The current skewed environment where investors appear to be buying more calls than they do also favors the CPSM structure.

Make no mistake, with the market down, CPSM was not able to offer the same downside protection while offering upside. On the Outcome Period Date, the Fund will need to price the next batch of flexible options based on the equity terms at that time.

Why is this fund attractive compared to outright buying SPY for some investors?

CPSM is a fund for conservative investors who are concerned about a market crash. No one wants to see their portfolio burn and incur large drawdowns in a bear market, hence the appeal of “buffer ETFs” like CPSM. A 9% upside on a one-year time frame is a number that most investors would find attractive on a net basis.

If you are an investor concerned about withdrawals, CPSM is the solution for you. In a worst-case scenario, a one-year investment in this fund from current levels could result in a loss equal to the fund’s expense ratio. Given the put, a -30% market decline will not impact the fund’s price when the options expire in April 2025.

Conclusion

CPSM is a new “ETF” from Calamos. The vehicle offers a 9% cap on the fully protected downside. The fund uses one-year FLEX options, and the potential investor needs to hold the fund for the outcome period in order to get the full benefits of the fund’s structure. With extended stock markets, we prefer CPSM to buying SPY outright here.