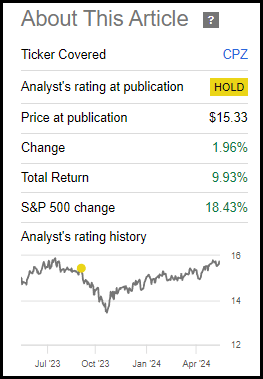

George Greuel

Written by Nick Ackerman, and co-produced by Stanford Chemist.

Calamos Long/Short Equity and Dynamic Income Fund (CPZ) provides investors with exposure to a dynamic portfolio consisting of shorting the market and investing in some of the largest markets names. This creates a situation where each part of the box works against the other. Although it can be used a bit as a hedge or tactically, this is one of the main problems the fund faces, in my opinion.

One of the most attractive features currently is the box discount, which has increased slightly since the last update. The discount expansion had a minimal impact on the fund’s total returns compared to the Standard & Poor’s 500 Index (SP500).

CPZ performance since pre-update (Seeking Alpha)

CPZ Basics

- One-year Z-score: 1.18

- Discount: -13.50%

- Distribution yield: 10.75%

- Expense ratio: 2.11%

- Leverage: 25.42%

- Assets under management: $472 million

- Structure: Duration (expected liquidation date, November 25, 2031).

The investment objective of CPZ is “to seek to provide current income and increase risk-managed capital.” They also add that the fund “seeks to provide hedged market exposure built on Calamos’ time-tested global long-short equity strategy.” The portfolio fits in. They stated, “The fund may be suitable for risk-conscious investors who wish to invest capital in the business in pursuit of income and capital appreciation.”

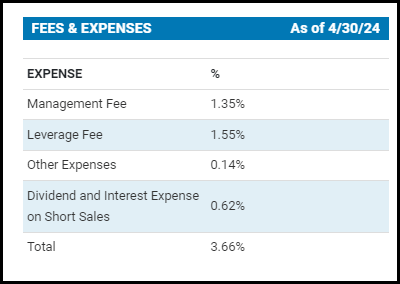

The fund’s expense ratio is high, and this comes with the nature of short investments. Being short means they pay dividends and interest expense on those short sales. Furthermore, the Fund uses leverage to enhance overall performance. Leverage adds more volatility and risk, as trying to increase performance also means increasing potential downside. Additionally, this leverage comes with its own costs, and when fully aggregated, the fund’s expense ratio comes to 3.66%.

CPZ (Kalamos) District Expenditures

Limited reasons to own

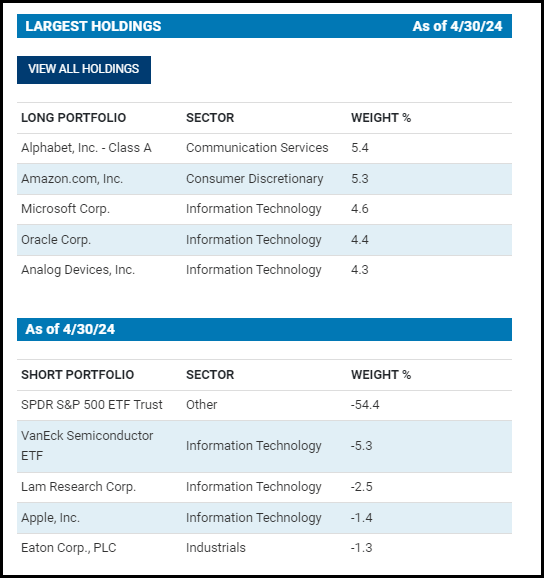

Over time, the stock market tends to have an overall upward trend, which can make short selling very difficult. You have to get your timing right and what you are cutting short in order to be successful. In the case of CPZ, it is interesting that they are shorting the SPDR S&P 500 ETF (SPY) while at the same time being the largest contributor to the index. These companies include Alphabet (GOOGL), Amazon (AMZN), and the largest espionage powerhouse at the time, Microsoft (MSFT).

The largest holding companies in the CPZ (Kalamos) region

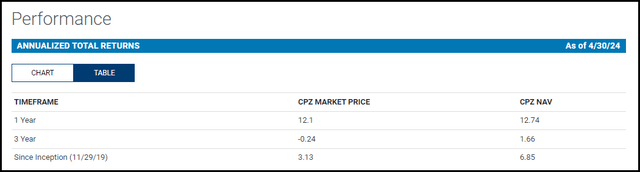

This can create a situation where one side of the portfolio is actively working against the other. Positioning here ensures that you will never outperform in terms of beating something like SPY. However, the fund has produced some positive results in its life – at least on a total NAV return basis – in each of the standard annual measurement periods.

Annual performance of CPZ (Calamos)

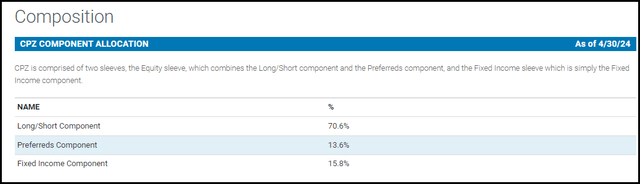

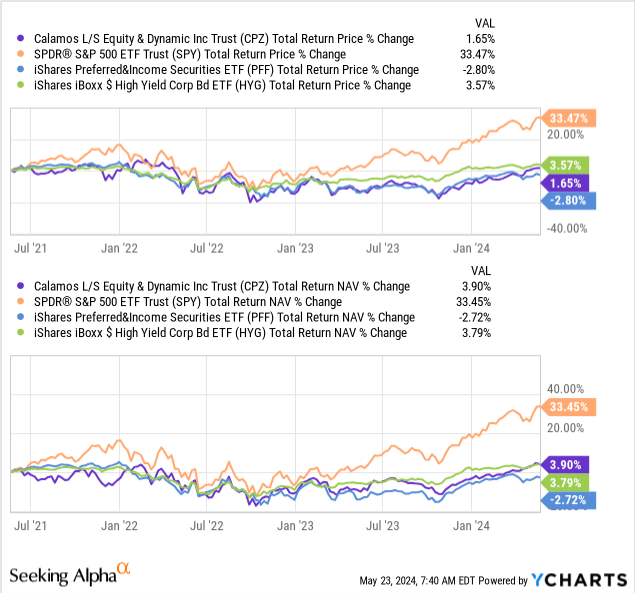

For some context, we can look at the fund’s performance over the past three years compared to SPY. But to be fair, the fund also holds a significant amount of fixed income and preferred instruments.

CPZ Asset Allocation (Calamos)

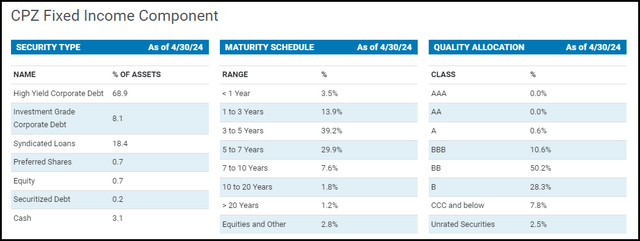

The fixed income wrapper focuses primarily on high-yield corporate debt.

Fixed income exposure in the CPZ (Kalamos) zone

Therefore, we will also include the iShares iBoxx $High Yield Corporate Bond ETF (HYG) and the iShares Preferred and Income Securities ETF (PFF) for comparison purposes.

YCharts

When these items are included, we can see the relatively lackluster results, and this is at least a partial contributing factor to CPZ’s weaker performance as well. Of course, with SPY returning 33%+ over the past three years and the fund actively selling the position, that won’t help the fund either.

Shorting SPY is nothing new for this fund either, as it is a staple of the fund and its “differentiation” factor. The last time we looked at the fund, it was short with a similar weighting of about 55%. So, the actual stock selection where they choose to sell doesn’t really seem to be what they’re looking for. Instead, they take an unexpected approach and sell out the entire market.

Having a differentiator is not always a good thing, but there are some limited instances where a fund can be attractive to an investor.

Reason No. 1: Discount appeal

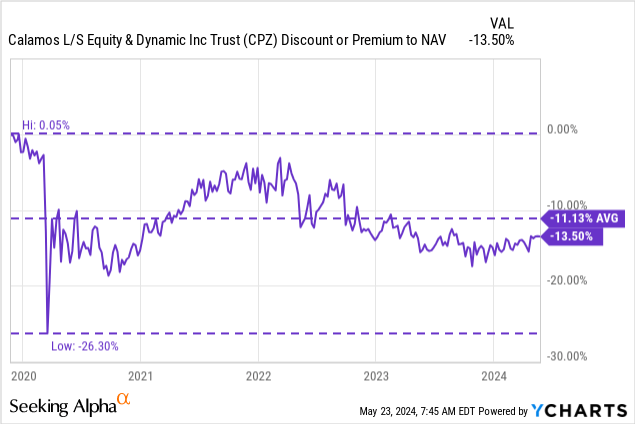

First, if they believe the fund’s discount may shrink in the future, that may be one of its currently attractive features. On this front, the appeal is limited because the actual relative discount to its historical level is not actually trading at a significant discount. Even the fund’s one-year z-score currently suggests the fund is on the richer side on this basis.

YCharts

Unless an activist pushes the Fund to do something about this discount, it does not appear that it will be a major incentive. Which, in fact, Saba Capital Management appears to own about 5% of the fund. Saba prompted Pimco to change the Pimco Dynamic Income Strategy Fund (PDX) back to a PIMCO-like strategy of being a multi-sector bond fund, where it had previously been a fund with a heavy energy focus.

Calamos converting CPZ into a long-only fund focused on stocks and convertible bonds could be a viable strategy for the fund. Another interesting possibility is to integrate CPZ into the Calamos Strategy Total Return (CSQ) fund. So that will be something to keep an eye on if anything happens there. Saba seems to be fully focused on BlackRock lately, so it may take some time.

As a structured term fund, one can expect to gain NAV in the future. However, with the date not set until 2031, there is some time before that becomes a real factor.

Reason No. 2: Hedging

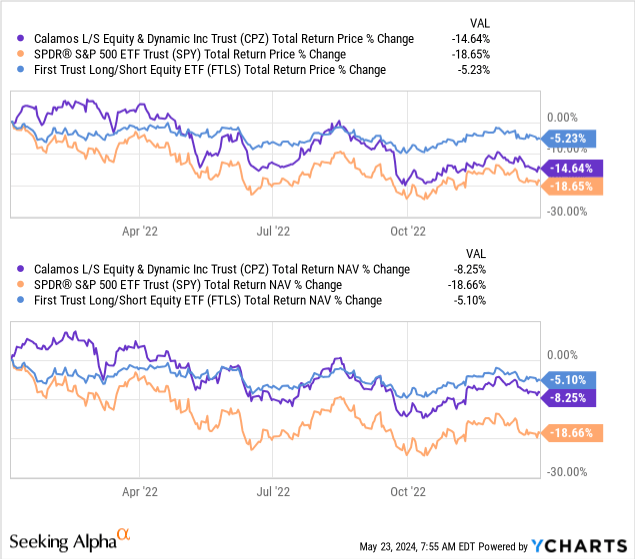

The second case to be made for this fund would be for hedging purposes. Having this short component in addition to the fixed income component can mean more limited losses during a bear market. 2022 is the latest example of a longer and longer bear market. During that time, CPZ’s NAV has declined less compared to SPY.

Given the discount/premium mechanism in mutual funds, this meant that the total fund share price return was poor anyway. Therefore, even this hedging factor can have limited success given the pool’s type of being a CEF and seeing wider cuts during volatile markets. Alternatively, a better bet would have been the First Trust Long/Short Equity ETF (FTLS), being an ETF that doesn’t trade with the same kind of runaway discount/premium.

YCharts

It’s also about timing; If you could predict when the next bear market would be, I think you wouldn’t be investing in these funds in the first place. Either allocate larger amounts of cash or simply sell the market yourself.

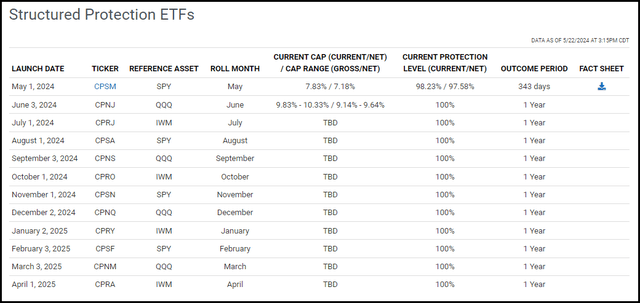

Also on this point, if you really want to stick with Calamos, they now offer “buffer ETFs” or “structured protection ETFs”. These are ETFs designed to give limited downside, but that comes with limited upside as well. Funds can participate in the rally to a certain extent. However, like any investment, the upside is not guaranteed. You may end up holding the fund for an entire outcome period and never make a return. In fact, if the market moves sideways, you will lose with an expense ratio of 0.69%.

Calamos Buffer ETFs (Calamos)

However, if you’re looking for funds that can primarily provide a hedge, the up to 100% downside protection that these buffer ETFs can offer should hold some appeal. These new offerings were brought to my attention thanks to a reader recently; I never realized these ETFs existed, and they could be something worth exploring further in the future.

The Calamos S&P 500 Structured Alt Protection ETF (CPSM) is the only ETF currently trading, but it is scheduled to launch a new fund every month for the coming year.

Reason #3: Distribution

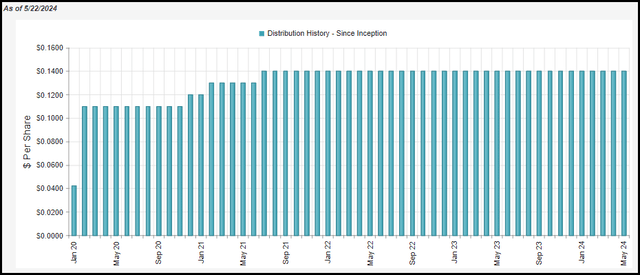

A third potential reason an investor might choose CPZ could be the monthly distribution. This certainly attracts income-focused investors.

CPZ Distribution Register (CEFConnect)

On the other hand, a CEF fund can pay whatever it wants as long as the NAV stays above $0. So, a 10.75% distribution yield may be attractive, but that doesn’t mean it’s earned. At an NAV rate of 9.30%, this is what the fund would have to earn going forward to support this payout. At least historically, we have already seen that the Fund has not been able to achieve this.

Conclusion

Given the unattractive position of Calamos L/S Equity & Dynamic Inc Trust’s portfolio – at least in my opinion – I will continue to lean toward being more negative on this fund. Even the reasons I might come up with for owning the box come with their own glaring issues.

I wouldn’t give it a “sell” rating because the fund’s discount has some appeal at this current level. Furthermore, the fund is not necessarily likely to produce poor performance, but should only continue to produce average results. I’m a big fan of Calamos, but for me, Calamos L/S Equity & Dynamic Inc Trust remains a pass at the end.