Miyako Nakamura/E+ via Getty Images

Casgevy’s proposition: Genetic leap or stumble?

I visited last time CRISPR therapeutics (Nasdaq: CRSB) in January. Remember that CRISPR Kasjivi It is a gene therapy product targeting transfusion-dependent beta-thalassemia (TDT) and sickle cell disease (SCD). It was Kasjevi It was approved in the United States in December 2023. It provides SCD patients with a “potentially curative” treatment. However, the company faces competition from another gene therapy producer, Livigeniawas approved on the same day as Casgevy and is marketed by Bluebird Bio (blue). Despite these important scientific advances, my January analysis expressed concern about “operational hurdles, competitive pressures, overvaluation, and uncertain long-term prospects” weighing on CRISPR Therapeutics. And then that was my recommendation.”He sells,” And CRSP It has fallen by 13% since then.

The initial commercial launch of gene therapies like Casgevy and Lyfgenia is different from small-molecule drugs. Companies “Approved treatment centers” must first be established. in Q1 report, CRISPR provided some insights into commercializing Casgevy. “More than 25 accredited treatment centers” have been established “worldwide,” paving the way for the use of gene therapy. “Cells have already been collected from several patients,” indicating their intention to undergo the $2.2 million CRISPR treatment.

When assessing the perceptions surrounding potentially curative gene therapies for conditions such as sickle cell disease, they are certainly mixed and nuanced. For example, the long-term benefits and risks of gene therapy remain largely unknown in early stages (Cleveland Clinic). However, despite some recent advances in sickle cell disease, the lifespan of patients with sickle cell disease (ASH) remains limited. In general, treatment recommendations favor gene therapy for adult patients with significant complications of ASH, despite standard treatments such as hydroxyurea. At present, it does not appear that gene therapy will be widely used in children.

First quarter earnings

Taking a closer look at Q1 earnings, CRISPR revenue of $504,000 missed by $26 million. I don’t see this error as important, as rolling out gene therapy requires time and strategy. Revenue estimates for the second quarter are $14.24 million. This is a more reasonable estimate, as some patients should start treatment. CRISPR is making progress in its efforts to reduce expenses. For example, R&D expenses decreased from $99.9 million in the first quarter of 2023 to $76.17 million in the first quarter of 2024. It is worth noting that CRISPR shares Casgevy-related costs with its partner, Vertex Pharmaceutical Industries (vertex). In the first quarter, CRISPR reported collaboration expenses of $47 million. This was slightly higher than the same period last year. General and administrative expenses were slightly lower, at $17.95 million. When excluding a significant one-time payment of $100 million recorded in 1Q23, CRISPR’s net loss improved reasonably in 1Q24, at $116.59 million. Common shares outstanding increased from approximately 78 million to approximately 81 million, representing only a slight decrease.

Physical ability

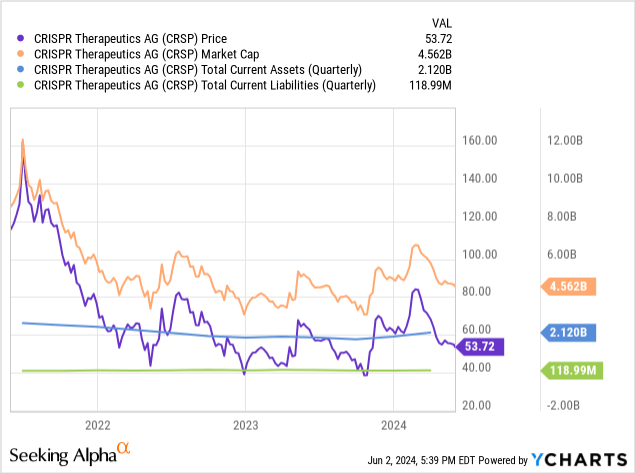

As of March 31, CRISPR’s cash and cash equivalents totaled $707.4 million. Marketable securities amounted to $1.4 billion. Total current assets amounted to $2.119 billion, while total current liabilities amounted to only $118.99 million. As such, CRISPR appears to be well-funded to handle the significant short-term costs associated with the complex rollout of Casgevy. CRISPR does not appear to have any significant debt on its balance sheet.

Since CRISPR is not yet profitable, I will estimate the cash runway based on historical data. I’ll use their net loss from Q1 ($116.59 million) for representation Burn cashI think this is the most representative number. When we divide their most liquid assets (cash and marketable securities) by their quarterly cash burn, we get approximately 4.5 years of… Cash runway. There are some limitations to my estimates, especially since they are historical. For example, CRISPR numbers indicate an increase in revenue as Casgevy infusions begin.

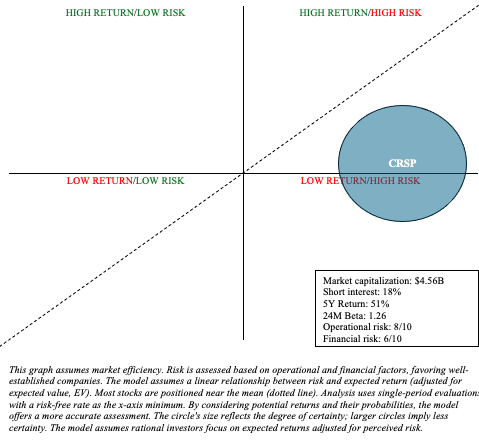

Risk/reward analysis and investment recommendations

CRSP is fraught with operational and financial (long-term) uncertainty when it comes to evaluating risk and reward. I represented the high level of uncertainty by adjusting the size of the CRSP circle within my risk/reward quadrant, as shown below.

Visual representation of the author

The treatment landscape for SCD and TDT is complex and evolving. The success of potential curative treatments like Casgevy depends largely on long-term outcomes and patient perception. Moreover, other gene therapies, such as Levigenia, are direct competitors to CRISPR. I still think Casgevy’s market, at least in the early years, will be remarkably limited and likely to be caught off guard by downside. However, CRISPR’s market capitalization, approaching $4.5 billion, appears to present many of the risks discussed above. The initial excitement that pushed CRISPR shares above $80 in February over the reality of marketing a complex, new, uncertain and expensive treatment has faded amid weaker sentiment in the biotech sector. Overall, I’m willing to upgrade my recommendation from “Sell” to “Sell.” “Catch” Based on the recent valuation revision and the company’s prudent management of operating expenses, which has expanded its cash runway so that there is more certainty about the market outlook. However, potential and current investors should be aware of the speculative nature of investments like CRISPR. This may be a suitable choice for your iron wallet. This means that it allocates the vast majority of cash to low-risk assets such as Treasuries and broad market ETFs, with the remainder allocated to investments that are more likely to generate alpha.

Editor’s Note: This article discusses one or more small-cap stocks. Please be aware of the risks associated with these stocks.