Jetta Productions Inc/DigitalVision via Getty Images

When things are not going your way in the market, it can be difficult to stay the course. The longer the market doesn’t agree with your assessment, the more difficult this type of situation becomes. After all, time is limited in life and the more you spend the more If you are holding a below average position, you seem to be missing more. However, in some cases, I think extreme patience may be worth it. A good example I think this applies to is Dana Incorporated (New York Stock Exchange: Dan).

For those who don’t know the company, it focuses on servicing different types of vehicles such as commercial vehicles and off-road equipment. It does this by selling axles, transmissions, driveline components, and other related products, all so that said vehicles can run. In May 2023, I wrote my last article about a company. In that article, I acknowledged that the company’s share price was underperforming the broader market. However, it was praised for its sales growth even as margins struggled. Given the cheapness of the stock, I could only keep it with a ‘buy’ rating.

Since then, things have not gone as I had hoped. It is true that stocks rose, but only by 9.3%. This pales in comparison to the 28.6% increase the S&P 500 saw over the same time period. Given this disparity in returns, you might think the company has underperformed. In some ways, that would be an accurate description. But in other cases, such as revenues and cash flows, the picture was mixed but generally positive. For the current fiscal year, management also remains optimistic. When you add on top of that how cheap the stock remains, I think patience will reward shareholders well in the end. For this reason, I keep the company with a “buy” rating for now.

Stocks look dirt cheap

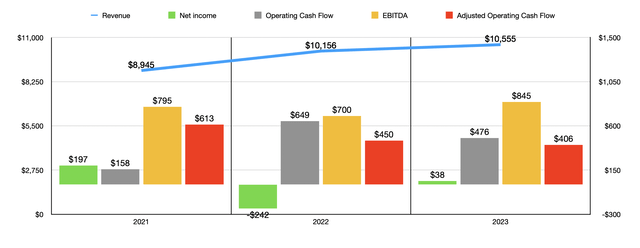

A lot has happened since I last wrote about Dana. So it might be wise to touch on the financial journey the company has taken since then. For starters, for fiscal year 2023, the company generated revenue of $10.56 billion. This was 3.9% higher than the $10.16 billion the company generated in 2022. Although the company has a history of making acquisitions, acquisitions and divestitures did not take into account any change in revenue during this time period. With the exception of the $9 million loss caused by foreign currency fluctuations, all of the company’s rise was attributed to organic growth. In particular, the company benefited from a $491 million, or 16.1%, increase in revenue associated with its European operations. $460 million of this increase was attributable to organic growth, with off-road, mining and construction demand driving strong growth. Management also said production of light trucks and medium/heavy trucks jumped nicely, expanding 16% and 17%, respectively.

Author – SEC EDGAR data

It wasn’t all great work. While the company benefited from a $136 million, or 9.8%, increase in revenue associated with the Asia-Pacific region, its North American and South American units took a hit. Labor strikes in the fourth quarter of 2023 and lower light truck production levels were instrumental in pushing total North American sales down $171 million. In South America, sales fell by about 7.2%. If we exclude foreign currency gains, the decline would have been even worse, reaching 8.6%. The administration attributed this to a decrease in the volume of production of medium and heavy trucks by 32%.

As overall revenues rose, the company’s profits improved, as the company went from a net loss of $242 million to a net profit of $38 million. There are multiple reasons why such a drastic change occurred. For starters, in 2022, the company had a goodwill impairment charge of $191 million. This compares to nothing in fiscal year 2023. Income tax expenses also rose significantly in 2022, reaching $284 million. This compares to the $121 million reported last year. Other profitability metrics were mixed. For example, operating cash flow fell from $649 million to $476 million. However, if we adjust for changes in working capital, we get a slightly smaller decline from $450 million to $406 million. On the other hand, the EBITDA of the business actually expanded from $700 million to $845 million.

Author – SEC EDGAR data

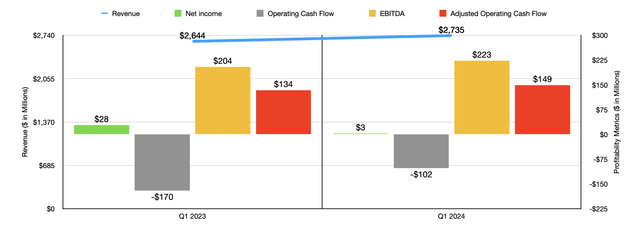

Moving into fiscal 2024, for which we only have the first quarter, the picture looks mostly better. Revenue of $2.74 billion came in 3.4% above the $2.64 billion reported at the same time in 2023. Almost all of that growth came from light vehicle production, up 14.1% year over year from $962 million to $1.10 billion. dollar. Much of that strength occurred in North America, where revenue of $1.33 billion was 12.2% above the $1.18 billion reported a year ago. Almost all of this growth was organic, with management attributing the upside in part to a full quarter of production in its full-frame light truck customer program compared to the fact that production was only increasing at the same time last year. Higher production levels of light vehicle engines and what management describes as a “sales backlog conversion” also contributed to this upward trend. Both Europe and the Asia-Pacific region saw sales declines, with weakness in the construction, mining and agricultural equipment markets negatively impacting sales in Europe, and lower sales of electric vehicle-related products in the Asia-Pacific region also impacting the business. In South America, revenues increased from $168 million to $184 million. High production volumes, including medium and heavy vehicles, helped in this regard.

The company’s only weakness from a profitability perspective relates to net income. The company went from a profit of $28 million in the first quarter of 2023 to a profit of $3 million at the same time this year. This was largely the result of a $29 million loss from the disposal of some assets that were for sale at the time. But other factors, such as interest costs rising from $34 million to $39 million, also contributed. Meanwhile, other profitability metrics were stronger during this time period. Operating cash flow fell from negative $170 million to negative $102 million. If we adjust for changes in working capital, we get an increase from $134 million to $149 million. Meanwhile, the company’s EBITDA expanded from $204 million to $223 million.

Although results have been largely mixed for a while, management seems optimistic about 2024. It expects, for example, revenue to be between $10.65 billion and $11.15 billion. At the midpoint, this would be 3.3% greater than what the company saw last year. Earnings per share should be between $0.35 and $0.85. At the halfway point, that would mean net profits of $86.9 million. But in all honesty, the extreme range given by management makes this estimate almost worthless in my opinion. On the low end, we’d be looking at net income of just $50.7 million. At the high end, we’ll be looking at a number of $123.1 million. However, other profitability measures do not have this problem. Operating cash flow is expected to range between $500 million and $550 million. Meanwhile, management expects EBITDA to be between $875 million and $975 million. No estimates of adjusted operating cash flows are provided. But if we take the midpoint of our operating cash flow and assume that adjusted operating cash flow will expand at the same rate on an annual basis, that would give us a reading of $448 million.

Dana Incorporated

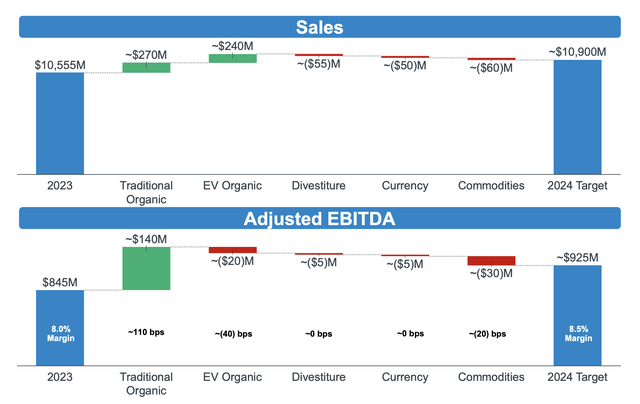

Besides providing only basic estimates, the company also provided more detailed estimates. In the image above, you can see the projected revenue bridge for 2023 to 2024. The company should benefit from organic growth of about $270 million on an annual basis. This focuses only on its traditional products. Meanwhile, its organic growth in electric vehicles should add another $240 million to its top line. This must be offset by divestments of up to $55 million, foreign currency fluctuations of up to $50 million, and changes in commodity prices of up to $60 million. This same image also shows a similar bridge that takes us to the middle of our EBITDA guidance. Despite the increase in organic revenue associated with electric vehicle sales, profits are expected to take a hit. This is not surprising to me. As I detailed in another article, the average price of an electric vehicle is declining rapidly compared to conventional vehicles. This is bound to put margin pressure on any company in this space. Fortunately, conventional organic products should increase profits by about $140 million.

Author – SEC EDGAR data

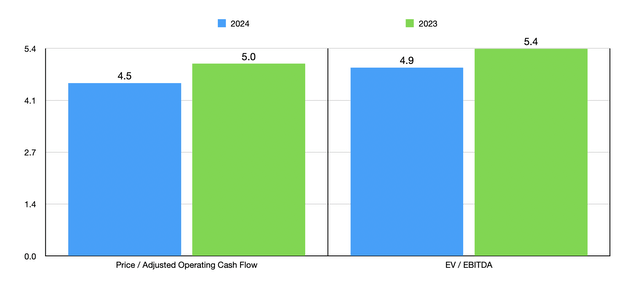

Using these numbers, I was able to value the company as shown in the chart above. I also estimate the company using last year’s results. It’s great to see a company trading in the low to mid single digit range. Even compared to similar companies, the share price looks attractive. In the table below, I compared them to five similar companies. On a price-to-operating cash flow basis, only one of the five companies was cheaper than Dana Incorporated. But using the EV to EBITDA approach, our candidate was the cheapest of the bunch.

| a company | Price/operating cash flow | Value added/EBITDA |

| Dana Incorporated | 5.0 | 5.4 |

| LCI Industries (LCII) | 6.1 | 12.2 |

| Patrick Industries (BATC) | 5.6 | 9.5 |

| Dorman Products (DORM) | 12.3 | 11.0 |

| Standard Motor Products (SMP) | 5.7 | 7.3 |

| Garrett Motion (GTX) | 4.1 | 6.0 |

Away

Fundamentally speaking, Dana Incorporated isn’t exactly the best company out there. The company’s financial results, especially the bottom line, are incredibly volatile. This creates some uncertainty, as well as additional risks. It is likely because of these mixed results that stocks have underperformed compared to the broader market. However, the stock is incredibly cheap, even using 2023 results. This is true on an absolute basis and relative to similar companies. Given this, I think keeping the company at a ‘buy’ rating is sensible and will pay off in the end.