sefa ozel

So far this earnings season, a lot of air has been knocked out of value growth stocks as investors de-risk their portfolios amid all-time market highs. Even strong quarters failed to resonate in markets, including the Datadog Index (NASDAQ:DoG) Q1 Earnings print, which was not only a superior quarter, but also showed accelerating growth and positive comments about normalizing macro conditions.

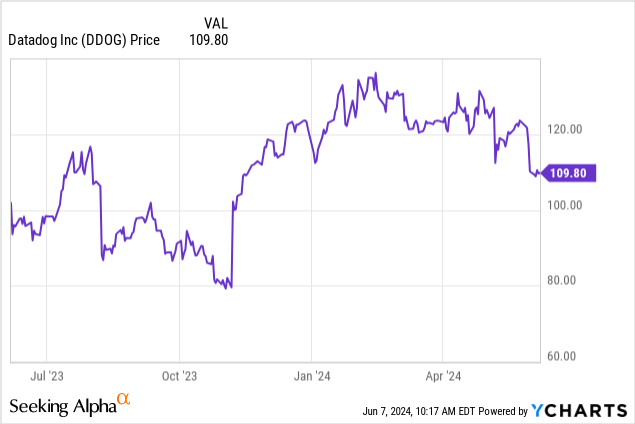

Year to date, Datadog shares are down 5%, underperforming the broader market (which is appropriate after a great year in 2023). However, to me, Datadog’s earnings decline after the first quarter represents the stock getting closer to my buy point.

I last wrote a neutral opinion on Datadog in February, when the stock was still trading near $130 per share. Since then, the stock has fallen about 20%, which piqued my interest. Overall, while I would still rule out Datadog as Too expensive to jump in and buy now, the stock is now on my watchlist if it continues to fall further. I repeat my own neutral Datadog position, with a slight bias toward the upside if volatility continues.

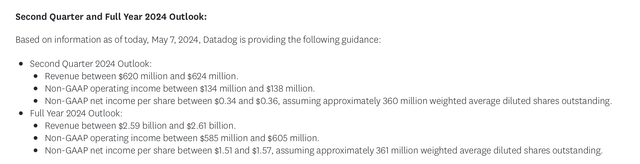

First thing we should check: Datadog’s guidance for the year was raised — which is to be expected for a company that routinely releases earnings and raises its forecasts every quarter. The company now expects revenues of between $2.59 and $2.61 billion for this year, or growth of 22-23% year over year, from a previous vision of annual growth of between 20-21%. For me, a two-point increase in growth expectations is too big.

Datadog forecast (Datadog Q1 earnings announcement)

Also note that for next fiscal year ’25, Wall Street analysts expect Datadog to generate revenue of $3.21 billion, which is 23% YoY growth on top of this year’s expected growth of 22-23% YoY.

Now, check the valuation: At current stock prices near $105, Datadog is trading with a market cap of $36.29 billion. After we divested $2.78 billion of debt and $743 million of convertible debt from Datadog’s most recent balance sheet, the company’s result Enterprise value: $34.25 billion.

This puts Datadog’s valuation multiples at:

- 13.2x EV/Revenue FY24

- 10.7x EV/Revenue FY25

I’m a buyer of Datadog stock if it arrives 9.5x EV/Revenue FY25, Which represents A Target price is $94 And 10% down from current levels. We can justify Datadog’s premium valuation multiple (although not as high as the low teens as it currently stands) due to the fact that the company scores highly from a “rule of 40” standpoint and remains a clear leader in infrastructure monitoring.

Other key upside drivers Datadog should be aware of:

- Huge market opportunity worth $62 billion – Datadog recently rated the observability market as a total opportunity worth $62 billion by 2026 (previously $53 billion by 2025), meaning Datadog still only cracks this overall market opportunity by single digits.

- Pure recurring revenue – Datadog It prices its products based on usage, and all of its customers provide recurring revenue for the company, giving it plenty of room for expansion.

Be patient on the margin until Datadog reaches the right spot price to buy.

Download Q1

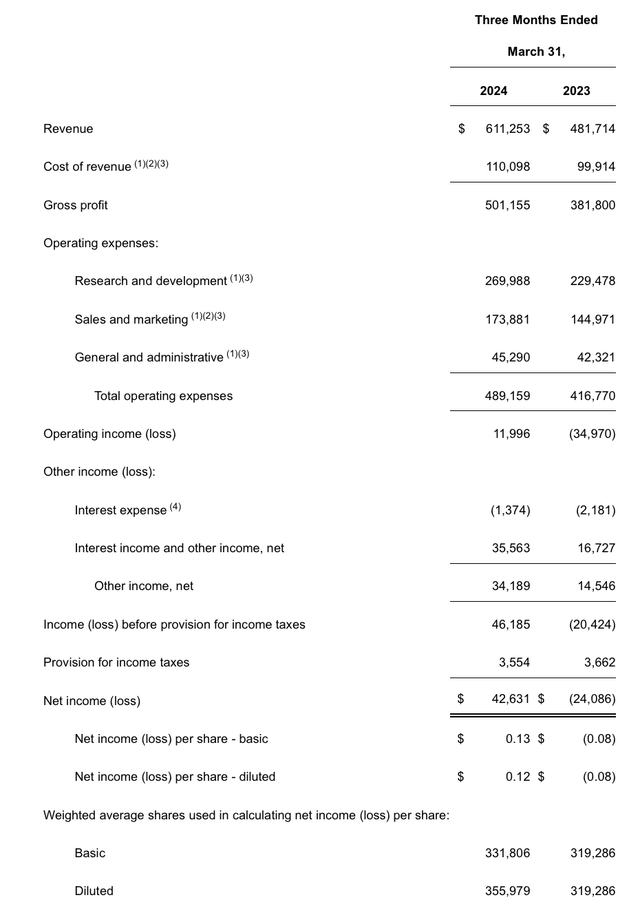

However, we must admit that Datadog’s first quarter results were excellent. Take a look at the earnings summary below:

Datadog Q1 results (Datadog Q1 earnings announcement)

Revenue rose 27% year over year to $611.3 million, exceeding Wall Street expectations of $591.7 million (+23% year over year) and even Acceleration by one point Compared to a growth of 26% year-on-year in the fourth quarter.

Management noted that usage trends are beginning to stabilize. Over the past few quarters, the company has experienced headwinds from IT leaders who optimized utilization in order to incur lower costs; But this trend is beginning to dissipate. CEO Olivier Baumel’s remarks on the first quarter earnings call:

In Q1, we saw usage growth from existing customers that was higher than in Q4, and usage growth in Q1 was similar to what we saw in Q2 and Q3 of 2022. As a reminder, this was the period when we started to see usage normalize after growth The accelerated pace we saw in 2021. Overall, we saw healthy growth across our product lines. As usual, our new products have grown at a faster rate on a smaller base.

While some of our clients continue to be cost-conscious, we are seeing a decline in the intensity of optimization activity. As an example, the model group we identified several quarters ago has grown sequentially again this quarter. We also see customers adopting more products and increasing their use with us. We believe this demonstrates that they are moving forward with their cloud migration and digital transformation plans and that we are implementing opportunities to integrate point solutions into our platform. Finally, the churn rate remains low with total revenue retention stable at the mid-to-high 90%, highlighting the mission-critical nature of our platform for our clients.”

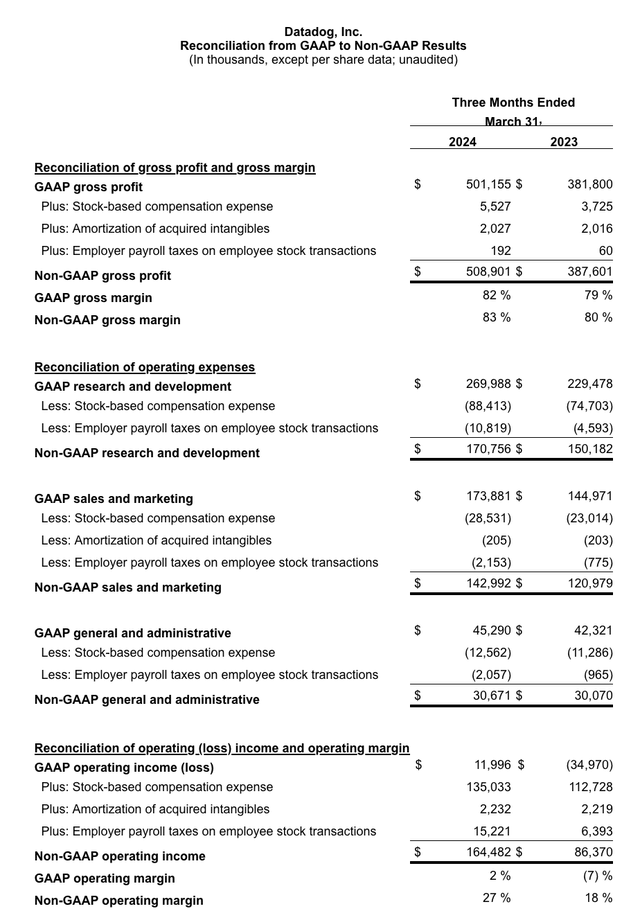

Datadog has also continued to outperform on the profitability front, and that’s the case despite of And the fact that it has earmarked 2024 as the year to invest in hiring, especially in sales and marketing (while many of its peers are cutting headcount and making 2024 the year of efficiency).

Opex grew just 14% year over year in the first quarter, which pales behind 27% year over year revenue growth. As a result, as shown in the chart below, pro forma operating margins rose to 27%, a nine-point improvement from 18% in last year’s first quarter.

Datadog margins (Datadog Q1 earnings announcement)

We note that this puts Datadog’s “Rule of 40” score at 54 (27% revenue growth plus 27% pro forma operating margins), which is the biggest justification for the Outstanding valuation here.

Main sockets

I still recommend patience with Datadog as the price target approaches $94, but be prepared to pounce on this stock in the event of near-term volatility. Datadog’s decline this year is a result of its huge valuation decline, but at its core, Datadog is a great company doing well above the 40 base, with committed customers and a software subsector that has a tremendous TAM.