Xavi Smith Photography/Stockbyte via Getty Images

Deckers Outdoor Company (New York Stock Exchange: Deck), together with its subsidiaries, designs, markets and distributes footwear, apparel and accessories for use in casual lifestyle and high-performance activities in the United States and internationally. The most popular brands that DECK owns are UGG and Hoka.

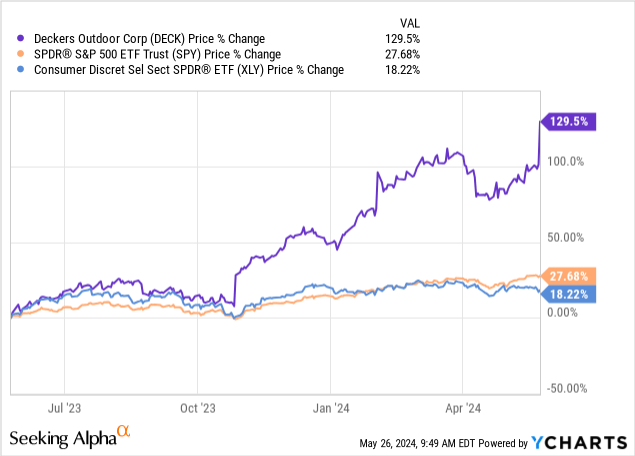

We decided to write about DECK today, as its shares have shown exceptional performance over the past 12 months. The company’s stock price rose nearly 130%, far outperforming the broader market and the consumer discretionary sector. Our goal today is to take a look at the company’s fundamentals, using its most recent annual report, published on May 24, and assess whether or not there is still upside potential left for potential investors after such a strong run. Besides the financial numbers, we will also comment on them briefly The macroeconomic environment, primarily consumer confidence, which we believe often has a material impact on demand for discretionary products.

Let’s jump straight into the latest results.

Financial results

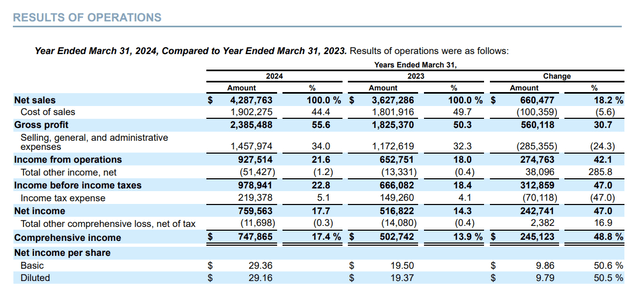

Deckers Outdoor beat revenue and EPS estimates for fiscal fourth quarter 2024 by generating revenue of $959.76 million and EPS of $4.95. Full-year results for 2024 also broke records with revenue of $4.29 billion – representing an 18% increase year over year, and diluted earnings per share of $29.16 – representing a 51% increase compared to the previous year.

Income Statement (DECK)

These numbers actually look impressive at first glance and seem to justify the sharp jump in the stock price after the announcement. But let’s now dig a little deeper into these numbers and examine the factors/brands that were actually driving this performance and discuss whether or not this performance is likely to continue in the future.

he won

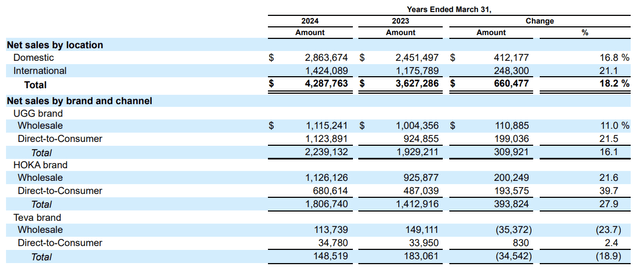

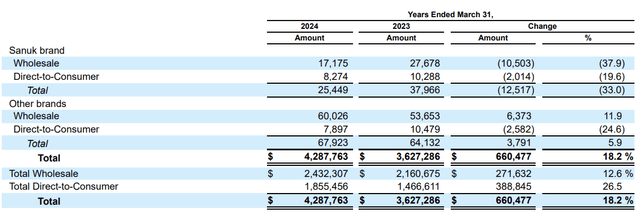

Net sales in fiscal 2024 were up 18% from the previous year. But it is important to break this growth. We will focus on three factors: channel, brand and geography. In order to conclude that growth is high quality, we would like to see growth across all/most channels, brands and geographies.

First, let’s take a look at sales by geography. In the following tables, we can see that DECK’s popularity has grown both domestically and internationally. They have been able to achieve strong double-digit revenue growth in both areas.

Sales (deck) Sales (continued) (surface)

If we continue our segmentation by channel and brand, we can see that the company’s two most popular brands – UGG and HOKA – have performed very well and shown significant growth in both wholesale and DTC. On the other hand, the company’s smaller, less well-known brands performed relatively poorly and partially offset the growth achieved by UGG and HOKA.

There are some key points in the annual report that we find particularly important to highlight here:

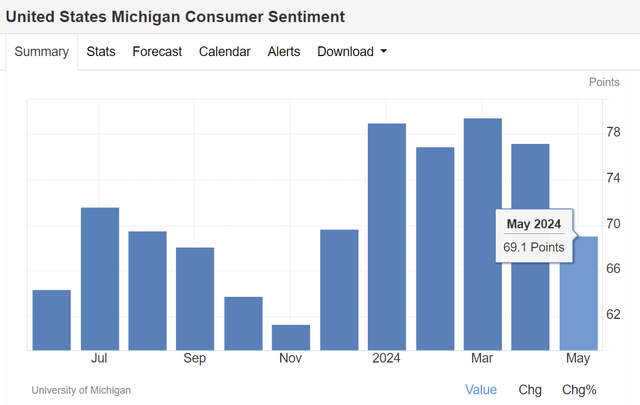

The total volume of units sold increased by 2.8%. This means that the company has been able to sell more items at a higher price, which has led to the material revenue growth we are seeing. We believe this is particularly impressive given the challenging macroeconomic environment, including volatile consumer confidence.

US Consumer Confidence (tradingeconomics.com)

Following this thought, we also have to highlight that DECK has been able to gain and retain customers online. In our opinion, this demonstrates customer loyalty and strong brand recognition.

Looking at the wholesale side, the company reported that HOKA’s net sales have increased domestically and in Asia as well, due to higher demand for certain high-performance products. Lower sales in Europe partly offset the growth. Looking at the UGG brand, it has done well globally. Higher full price sales and selective price increases have contributed to increased revenues.

Overall, we find these results impressive. We believe that the increase in the total volume of units sold, combined with the increase in prices, demonstrates the strength and strength of demand for DECK products. And all this despite headwinds from weak consumer confidence. Looking to the future, the company also seems optimistic, although it expects growth to be somewhat slow. Revenue growth for fiscal year 2025 is expected to reach approximately 10%. Comparing these forecasts with those of DECK’s peers also highlights how strong DECK’s performance is.

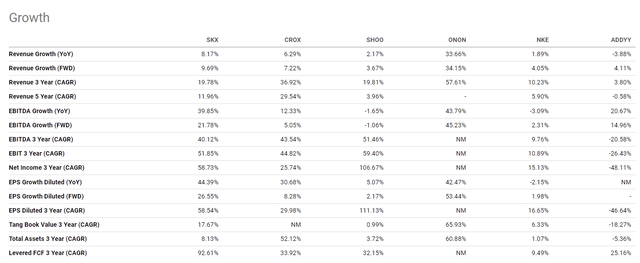

Growth(SA)

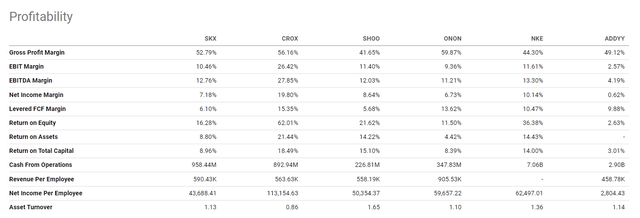

Profitability

Not only were higher revenues generated, but the company’s profitability also improved, which is key to long-term success. Gross profit margin expanded to 55.6% compared to 50.3% in the previous year. Operating margin expanded to 22.8% from 18.4%, and last but not least, net income margin also expanded to 17.7% from 14.3%.

The higher margins were primarily driven by:

(…) favorable full-price sale of the UGG brand, favorable changes in shipping costs, favorable HOKA brand mix and UGG brand product mix shifts, including benefits from selective price increases, and favorable mix of sales in the DTC channel.

The higher full selling price, while reducing inventory and increasing overall sales, we find particularly attractive. Often, when companies need to reduce their inventory to avoid products becoming obsolete, they use deep discounting. This was not the case for DECK.

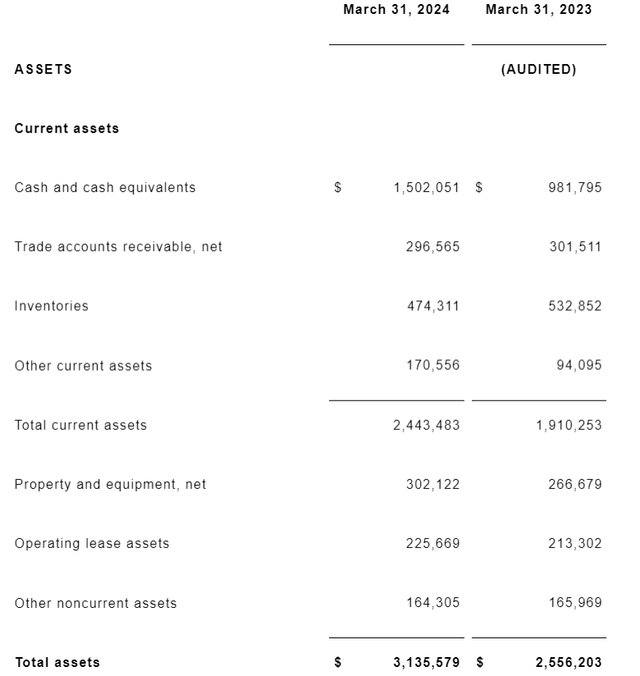

Assets (deck)

These benefits were partially offset by higher SG&A expenses, driven by higher headcount and performance-based compensation, increased advertising and promotion expenses, higher lease and occupancy expenses, and finally by investments in infrastructure.

Now, comparing these numbers again to DECK’s peers and competitors, we can see that DECK is one of the strongest players in this space.

Profitability (SA)

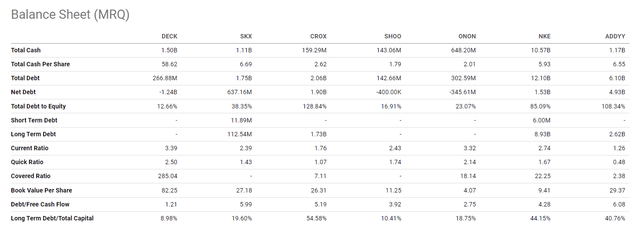

Liquidity

From a liquidity standpoint, we also don’t have much to complain about. The company has barely any debt, and it has liquidity ratios – the current ratio and the quick ratio – well above one. Compared to their peers, DECK’s numbers look attractive again.

Balance Sheet (SA)

Strong liquidity means that the company has financial flexibility and can easily cover its current liabilities with its current assets. This may be particularly important when the macroeconomic environment is uncertain, as is the case now.

For all these reasons, we find DECK attractive from a fundamental standpoint. Strong revenue growth, driven by rising demand and significant pricing power, coupled with expanding profitability, are all positive signs looking to the future. The most important question now remains: Is the current share price attractive or not?

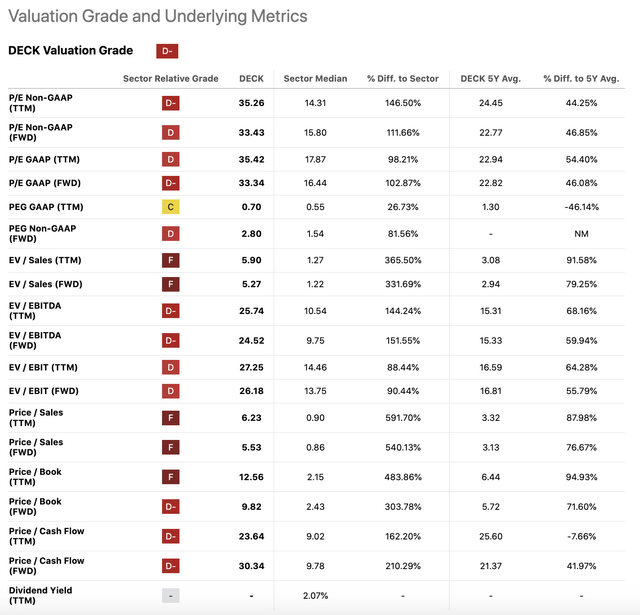

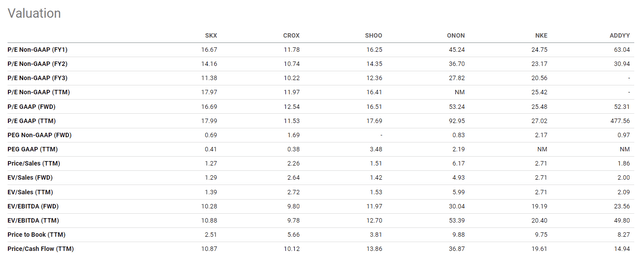

evaluation

To answer this question, we’ll look at a range of traditional price multiples and compare the company’s numbers to the consumer discretionary sector average as well as its own historical averages.

Rating (SA)

All of these metrics indicate overvaluation. If we narrow down the peer group to the companies we used above for comparison, we can still see that DECK stock appears to be at the higher end of the valuation range.

comparison (SA)

On the one hand, we believe the premium is justified due to outstanding growth. On the other hand, we don’t think the current stock price is attractive to a value investor. Even growth investors, who may be less concerned with valuation, should be aware of the range of risks that could derail DECK’s growth story in the near future and could lead to a significant share price decline. We would like to highlight two key risks that we feel are important to consider before investing now:

1. Recently, the container crisis has led to a significant rise in sea freight costs. If this continues, this could have a significant negative impact on DECK’s costs, which could lead to margin contraction and lower earnings per share.

2. Competition is fierce. Companies are constantly coming up with new concepts and new products to make sure they get the biggest piece of the pie. New companies are also entering the arena, trying to challenge the more established players. While DECK appears to be doing well now, maintaining high demand and interest for its products, one might wonder how long it can be sustainable. Potential counterfeits or cheaper substitutes, especially when consumer confidence is weak, could reduce demand for DECK products.

Conclusion

DECK reported outstanding sales and EPS numbers for fiscal 2024. Revenues grew 18%, while EPS increased 51%. The company also expects double-digit sales growth to continue in fiscal year 2025. The total volume of units sold also increased, despite a higher level of full-price sales and selective price increases, proving that demand for DECK products is strong.

The company’s margins also expanded, driven by lower shipping costs, selective price increases and a higher level of full-price selling. At the same time, the company has also managed to reduce its inventory levels.

The company is also attractive from a liquidity perspective, with a relatively small amount of debt and liquidity ratios well above 1.

However, the company’s valuation appears to be relatively high. We believe that based on a range of traditional price multiples, there is no significant upside, and therefore we do not believe that initiating a position at these price levels can outperform the broader market.

For these reasons, we have assigned a “Hold” rating to DECK.