Dell Q1 Preview: Expect routing upgrade due to AI-enhanced server; Buy Rating (NYSE:DELL)

thinglass

Dell Technologies (New York Stock Exchange: Dell) provides storage, server, networking, computers and workstations to commercial and consumer customers. Recently, Dell has partnered with major GPU manufacturers including Nvidia (NVDA) and Advanced Micro Devices (AMD).) to launch AI-optimized servers. While the AI-related business represents less than 5% of total revenue today, I expect the AI-enhanced server and storage portfolio to have the potential to transform Dell’s growth profile. I expect Dell to upgrade its full-year guidance; Therefore, I am buying its shares ahead of its next quarterly earnings announcement scheduled for May 30thy After the market closes. I start with a “buy” with a one-year target price of $205 per share.

Growth from AI-optimized server and storage

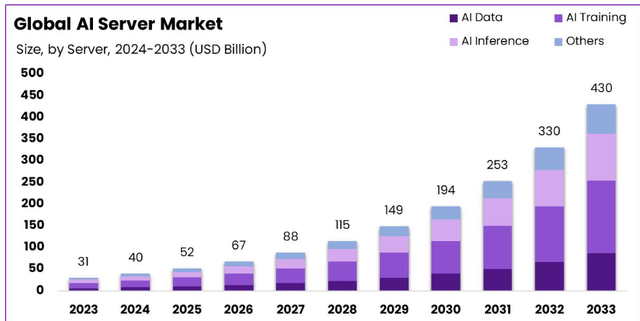

Market.US expects the AI server market to grow at a CAGR of 30.3% from 2023 to 2033, primarily driven by AI training, inference and data. AI servers are equipped with GPUs From third parties including Nvidia’s H100 and H200 and AMD’s MI300X. Since corporate investment in AI is still in its early stages, I expect the AI server market to continue its rapid growth in the near future.

Market.United States

Dell has a wide range of AI-powered server and storage families, including the PowerEdge XE9680, XE9640, XE8640 and R760xa. Dell servers are compatible with major GPU providers including Intel (INTC), Nvidia, and AMD. Dell exits fiscal 2024 with a total backlog of $2.9 billion, with orders growing 40% quarter-over-quarter, as revealed in its latest earnings call. I believe AI-related companies account for less than 5% of total revenue today; However, I am optimistic that AI-optimized server and storage will grow by 15%+ in the near future because:

- Most large-scale companies and enterprises still leverage AI primarily for training purposes. Once AI training is complete, the AI market will gradually shift toward inference, improving workload efficiency and enabling machine-to-machine interactions. In the AI inference phase, more AI-optimized servers are needed to interact with end-clients.

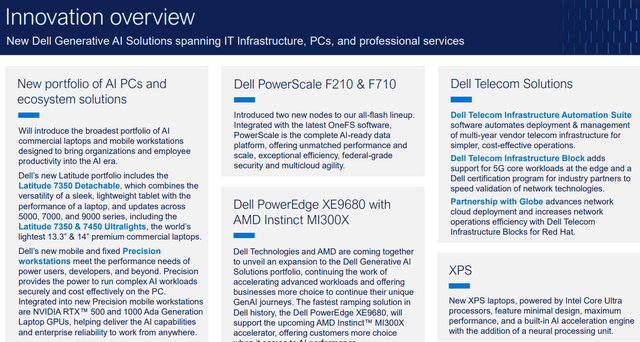

- As revealed by the company, Dell has approximately 30% market share in the mainstream server market. The leading position provides a strong foundation to capture the rapidly growing AI server market. Dell has done a great job partnering with major GPU providers with their innovative PowerEdge products. As shown in the slide below, Dell has launched a wide range of AI solutions across IT infrastructure, computing, and professional services.

Dell investor presentation

Customer Solutions Group is a mature market

Dells Customer Solutions Group (CSG) sells PCs, laptops, desktops and workstations, serving consumer and business customers. The business is tied to the hardware refresh cycle, and most of its operations are located in mature markets.

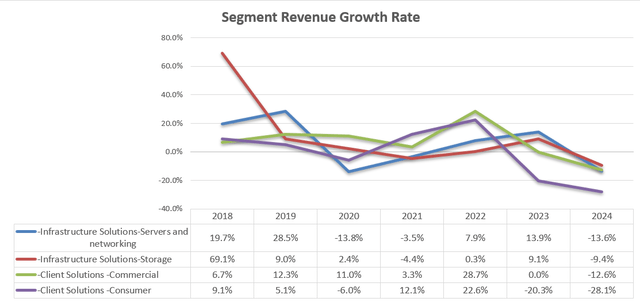

Dell has focused on its commercial side of the CSG business, which makes strategic sense. 80% of Dell units are in the commercial end market. As the company revealed, Dell captured 23% of the business PC market share in FY23, a marked improvement from 16% in FY13. As shown in the chart below, Dell’s business PC business saw decent growth over the course of The past few years.

Dell 10 kilos

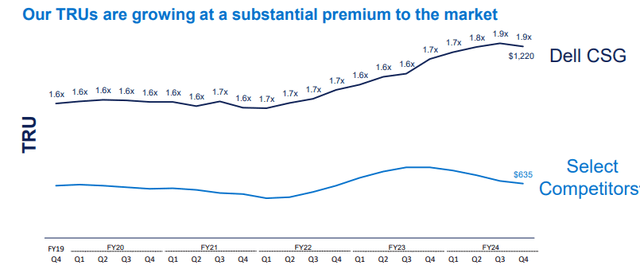

The business’s strong growth is primarily due to its premium pricing and total revenue per unit (TRU). As shown in the chart below, Dell makes about $1,220 TRU, 1.9 times the TRU of its competitors. This is due to Dell’s focus on large enterprises and premium PC and workstation solutions.

Dell investor presentation

Having said that, since PC is a mature business, I expect CSG to deliver LSD-type growth in the long term. In other words, I don’t expect CSG to become a structural growth driver for Dell’s growth over the long term.

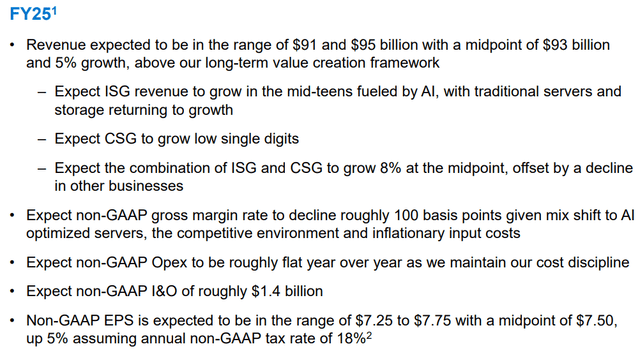

Q1 FY25 preview and FY25 outlook

In Q4FY24, Dell expects its revenue to grow 3% in Q1FY25 and 5% for the full year at the midpoint. Overall, I think their guidance for FY25 is quite conservative, and most likely, they will upgrade their full-year guidance next quarter, in my view. Nvidia reported its Q1FY25 results on May 22 with its data center business growing 427% year over year. Strong growth in data centers was driven by strong AI compute and strong orders for the H100 and H200. Additionally, during the earnings call, Nvidia revealed that Dell will bring Nvidia’s new Ethernet switch, Spectrum-X, to market. Strong growth in the data center business and new product distribution through Dell will likely lead to a strong quarter and fiscal ’25 for Dell.

Dell investor presentation

To achieve growth in FY25, the following factors must be taken into account:

- Customer Solutions – Consumer Business: After a two-year slowdown in PC demand, I expect the PC market to begin to recover in FY25. Microsoft (MSFT) announced that Windows 10 will reach end of support on October 14, 2025, marking It may stimulate hardware upgrade in the near future. As such, I expect the Customer Solutions – Consumer business to grow at least 5% in FY25.

- Customer Solutions – Business: In addition to potential tailwinds from Windows 10, businesses could be driven by AI-powered edge computing requirements. As we discussed earlier, the AI is ready to enter the inference phase in the future, after the AI training is completed. AI-powered edge computing can generate additional requirements for computers and workstations.

- Servers, Networking and Storage: I expect the market to grow rapidly over the next few years, as analyzed previously. I expect Dell to grow 15%+ in the near term.

Putting it all together, I expect Dell to be able to grow its revenue by 8.5% in FY25. As such, I think its original guidance is quite conservative for its revenue growth rate.

Ratings

As for normalized revenue growth, I expect Dell Customer Solutions to grow 3% annually, since PCs and workstations are inherently mature businesses. Through this cycle, the LSD PC market is likely to grow in the future. As such, normal revenue growth has been calculated at around 7%, assuming growth of 15% from servers/storage and 3% from PCs.

I expect Dell’s margin expansion to come primarily from gross earnings and SG&A expenses. Dell has been implementing its cost optimization initiatives over the past few years. In addition, Dell has steadily improved its revenue per unit for its PC business, as discussed previously.

I believe Dell can generate operating leverage from its gross earnings of 10 basis points annually, and another 10 basis points from SG&A leverage. Total operating expenses are expected to grow by 6.7% in the model.

Dell DCF – Author Calculations

Free cash flow from equity is calculated in the table below:

Dell FCFE- Author’s calculations

The cost of equity was calculated to be 10.6% assuming: a risk-free rate of 4.5% (10-year US Treasury yield); Beta 0.87 (SA); Equity risk premium 7%.

Deducting all free cash flow from equity, the one-year price target is calculated to be $205 per share. The current share price implies less than 18 times forward free cash flow, which is a very cheap multiple compared to other growth companies.

Main risks

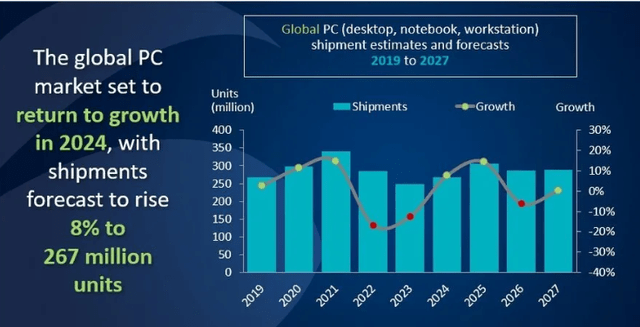

Consumer computers business: The consumer PC business represents about 10% of total revenues, and revenues were down 28% in FY24 and 20% in FY23, following the global pandemic. Toms Hardware expects the global PC market to return to growth in 2024 and 2025. As shown in the chart below, the global PC market shows high volatility due to its association with consumer renewal cycles. As such, Dell investors need to feel comfortable with the inherent volatility of the company’s PC business.

Canalys reports

Marketing AI server and storage: Although I believe that AI servers and storage will see rapid growth over the next few years, it is important to acknowledge that the market will eventually be commoditized, similar to other types of IT hardware. However, this is a long-term risk for Dell, and I expect Dell to be able to enjoy rapid AI growth for several years, as the enterprise AI market is still at an early stage.

Debt level: Dell had ~$26B of total debt in FY24, implying 3.1x total leverage. The level of leverage is very high compared to other technology companies. The company needs to reduce its debt levels to improve its balance sheet.

Class Actions Related to Class V Treatment: In 2022, Dell reached a $1 billion settlement of a lawsuit accusing it of defrauding some shareholders in 2018 when it returned as a public company. Although the lawsuits were settled, it was an indication that Dell did not have strong corporate governance at the time.

To my readers:

Rapid growth in server AI and storage will likely accelerate Dell’s long-term growth profile, which could send multiple shares higher. I buy ahead of earnings and initiate a “buy” with a one-year target price of $205 per share.