Diverse photography

Dell Technologies (New York Stock Exchange: Dell) posted relatively mixed performance in 1Q25 with strong strength in AI server revenue, servers shipped, and strength in backlog. Despite this high level of demand, other sectors continued to face challenges with warehousing recording a flat quarter with 3% growth in business activity. PC sales were coupled with a -15% decline in consumer PCs and a tighter outlook for operating margins. Although these factors seem discouraging upfront, I believe Dell is well positioned for a strong finish to FY25 and continued strength into FY2026 as enterprise customers move from training AI/MBA models to getting them into production, which I think it will create a ripple effect across storage, networking and ultimately endpoint sales. Incorporating this thesis into my financial outlook, I reiterate my Strong Buy recommendation for DELL stock and believe shares should be priced at $194.41 per share at 8.48x FY2026 EV/EBITDA.

Be sure to check out my initial thesis here:

Dell has untapped upside risk

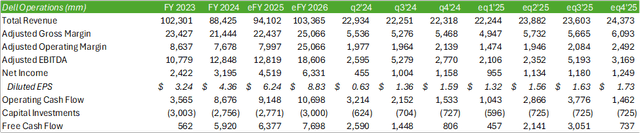

Dell Technologies operations

Dell Technologies reported mixed earnings results for 1Q25, as its growth engine, AI infrastructure, showed significant strength in the quarter coupled with weak growth in PCs. Management remained optimistic about a PC recovery rollout in the second half of 2025; However, I expect this to remain relatively constant despite the approaching modernization cycle as organizations seek to manage lower costs while simultaneously bringing in AI applications. As management noted during the call, several companies are working through test prototypes and are expected to begin inferring local applications later this year. As this happens, I expect heuristics to be the driver of modernization, not the 4-year modernization cycle. My prediction is for the PC to become a bottleneck for speed, rather than upgrading for the sake of upgrading. I believe that storage growth will be the leading indicator of PC growth in future periods, as investments in storage are likely to be a result of the move from cloud-based applications to on-premises hardware-based applications and reasoning.

Corporate reports

As a result, I expect relatively flat growth in the CSG sector for Q2 2025 and Q3 2025 before seeing strength in Q4 2025 and continued strength in FY26. Although I expect domestic AI applications to ramp up next year However, I believe that a lot of testing will take place in the cloud before moving to private data centers. This thesis is based on the H100s’ bottlenecks in Q4 2024 and inventory improvements in FY25. I also expect growth in AI-powered PCs to be driven by the adoption of enterprise-level AI applications, which likely won’t happen until The second half of 2025 or FY26 as companies continue to undergo data training. Given how quickly these applications are evolving, and the security risks inherent in implementing corporate data, I expect companies to take more conservative steps toward adopting the applications. My thesis on cybersecurity can be found in my recent report covering CrowdStrike (CRWD) which partners with Dell to secure AI infrastructure.

On the ISG side of the business, I expect the flow of strength to continue as demand for AI infrastructure continues to grow. Management said supply chain bottlenecks for Nvidia’s (NVDA) H100 GPUs have eased, which in theory should allow more companies to build their own AI factories in-house. As for the H200 GPUs, I expect most of the demand will initially be driven by hyperscalers because I don’t think companies will require that much capacity up front. If this is the case, I believe this will allow every customer to gain the capacity required to build and operate their own data centers. As a result, as organizations expand their AI infrastructure, storage should follow suit followed by networks and business computers.

Corporate reports

Taking into account the company’s overall operations, management stated that the company may face some margin headwinds as a result of inflationary pressures combined with competitive pricing pressures as holiday PC sales deals continued during 1Q25. Although I do not expect it to constitute This challenges demand for AI and endpoint infrastructure over time, but I expect Dell will still be able to remain price competitive to attract consumers and business customers to upgrade to newer PC models. This may become more prevalent as AI personal computers become more accessible, especially with the pace of improvement in technology. Despite this factor, I expect Dell to have the ability to grow its cash flow as demand for next-generation infrastructure remains high, even if legacy servers remain flat throughout the year.

Corporate reports

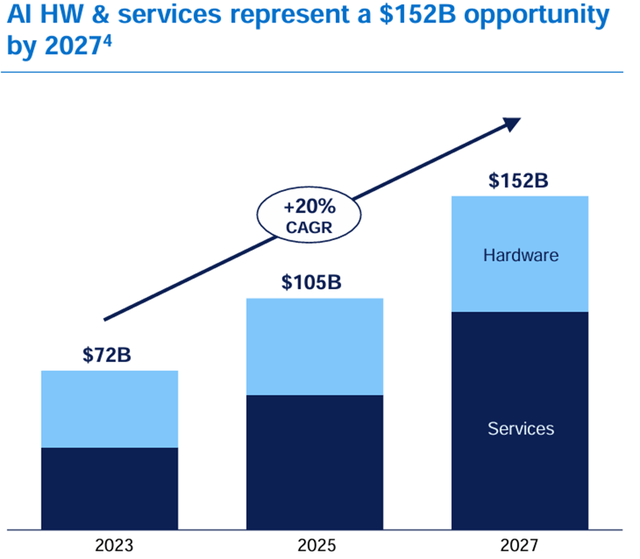

To reiterate my initial thesis for Dell, I expect most of the company’s growth to come from server builds with storage and networking lagging for a few quarters, and eventually for endpoints to follow in FY26. As Palantir’s (PLTR) growth outlook improves for FY2024, I expect some degree of acceleration In the second half of 2025 so that institutions can obtain the necessary infrastructure to run these LLM models. I think the big inflection point for Dell will be driven by the shift from training data to inference data. This can be seen in Dell’s $2.6 billion in order revenue from AI infrastructure and a growing backlog that now stands at $3.8 billion. Given the massive 20% annual growth rate for AI-related infrastructure and services according to IDC forecasts, Dell should realize significant tailwinds in the space that should flow through other verticals like storage, networking, and endpoints.

Corporate reports

Valuation and shareholder value

Corporate reports

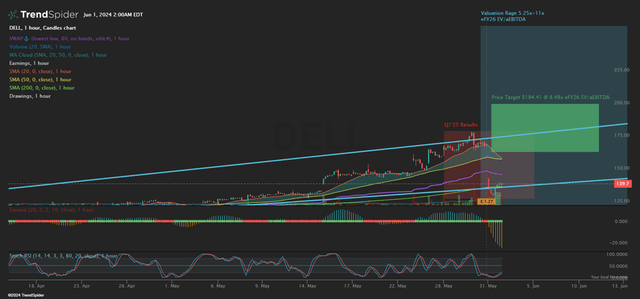

DELL shares took a hit from their all-time highs, closing down 18% the day after earnings. I think a lot of the price performance was driven by the potential challenge of margin pressure in the coming quarters, coupled with profit taking as shares saw a significant uptick in post-FY24 results.

TrendSpider

Looking at the technical chart, DELL stock appears to be in a sell-off position. I believe this event has provided space for investors to build their positions within the stock as I expect continued growth over the duration of FY25 to FY26.

TrendSpider

Given Dell’s growth trajectory driven by growth in AI infrastructure followed by ripple effects across other sectors, I maintain my Strong Buy recommendation with a price target of $194.41 per share at 8.48x FY2026 EV/EBITDA.

Corporate reports