Thomas Barwick

Investment Thesis: I have a bullish view on Despegar.com.

In a previous article in March, I made the argument that Despegar.com (New York Stock Exchange: Desp) has the potential for further upside in the future, due to strong growth in Total bookings and revenue – with the Brazilian market showing a particularly strong performance.

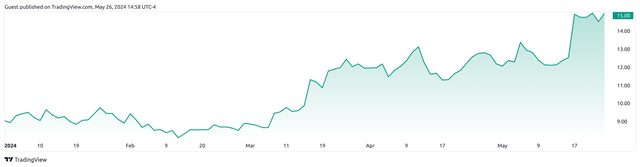

Since then, we’ve seen the stock skyrocket – with over 37% growth since my last article.

TradingView.com

The purpose of this article is to evaluate whether Despegar.com has the potential to see further upside in the future – taking recent performance into account.

performance

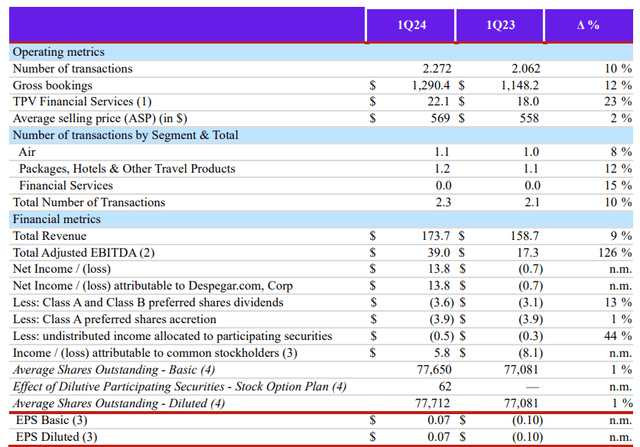

When looking at Despegar.com’s Q1 2024 financial results, we can see that total bookings increased by 12% compared to the previous year’s quarter.

Despegar.com Q1 2024 Financial Results

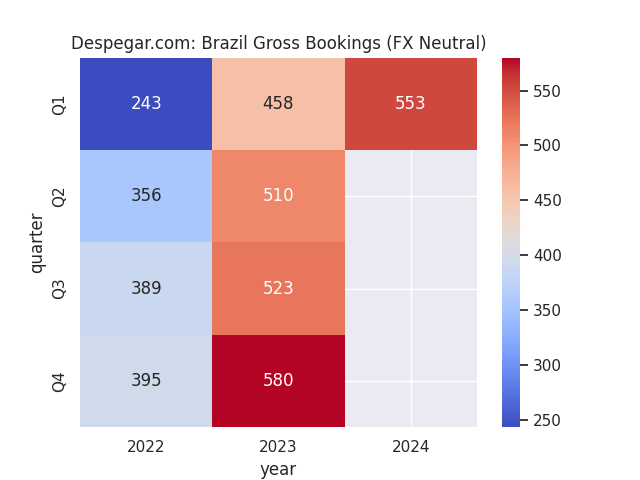

The Company determines that on a foreign currency neutral basis, the total… Bookings rose 42% year-on-year, with the strong demand environment in key markets such as Brazil and Mexico the main driver of this growth.

Looking at the Brazilian market, which is more than twice the size of the Mexican market, we see that total bookings on a foreign exchange neutral basis were up 21% sequentially to US$553 million.

Figures are derived from Despegar.com’s historical financial results. Heat map created by the author using the marine visualization library in Python.

This growth rate was much higher than the rate we saw in Mexico, where we saw 15% growth from US$218 million to US$250 million over the same period.

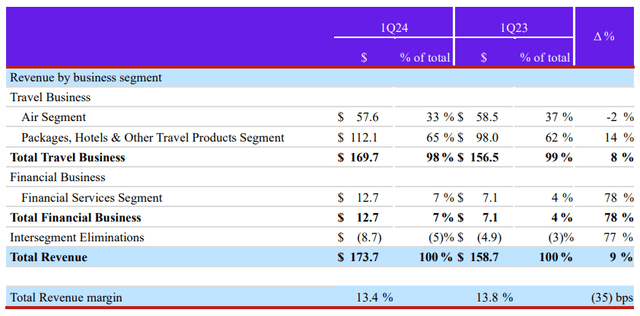

When looking at revenue by business segment, we can see that the packages, hotels and other travel products segment witnessed a growth of 14% compared to the same quarter of the previous year. Furthermore, this segment now represents 65% of total revenues, compared to 62% in the previous quarter.

Despegar.com: Financial results for the first quarter of 2024

In this regard, I find that the growth in revenues and total bookings during the last quarter was impressive.

From a balance sheet standpoint, Despegar.com has continued to reduce its long-term debt – falling to $1,944 million last quarter with a long-term debt to total assets ratio of 0.22%.

| December 22 | December 23 | March 24 | |

| Long term debt | 5119 | 2262 | 1944 |

| Total assets | 804172 | 898334 | 886062 |

| The ratio of long-term debt to total assets | 0.64% | 0.25% | 0.22% |

Source: Figures (in thousands of US dollars) are derived from Despegar.com’s Q4 2022, Q4 2023 and Q1 2024 quarterly reports. Long-term debt to total assets (%) calculated by author.

When looking at short-term liquidity, we see that the quick ratio remains at the same level as it was in the previous quarter – but cash and cash equivalents are down more than 15% since last quarter.

| December 22 | December 23 | March 24 | |

| Cash and cash equivalents | 219167 | 214576 | 181495 |

| Accounts receivable | 147806 | 183393 | 204494 |

| Total current orders | 564466 | 671080 | 657754 |

| Fast rate | 0.65 | 0.59 | 0.59 |

Source: Figures derived from Despegar.com’s Q4 2022 and Q4 2023 financial results (in US$ thousands, excluding quick ratio). A quick ratio calculated by the author.

Looking to the future and risks

We see that the Brazilian market continued to show strong growth in gross bookings, while revenues across the Packages, Hotels and Other Travel Products segment showed double-digit growth. In terms of my view on the above results and future prospects of the stock, it is clear that future growth will depend heavily on the performance in the Brazilian market.

While the company’s balance sheet shows a quick ratio of less than 1 (suggesting that the company does not have enough liquid assets to service its current liabilities), I argue that the company’s low levels of long-term debt compared to total assets means investors will. We are willing to overlook a decline in short-term cash reserves as long as we continue to see strong growth in total bookings and revenue – which is the case.

Given that we’ve recently seen EPS rebound into positive territory, the growth we’ve seen in the stock is likely driven by revenue, not earnings growth per se.

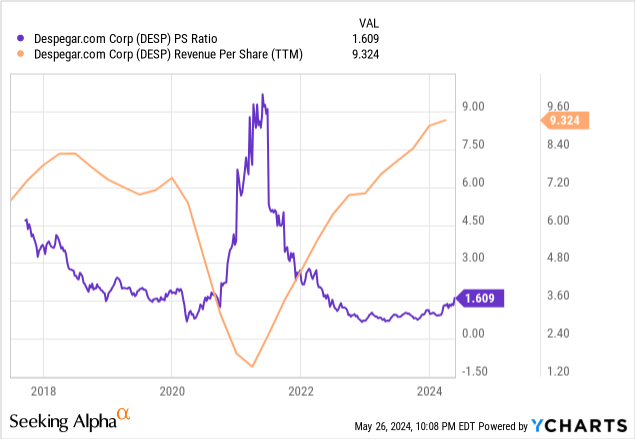

We can see that the company’s price-to-sales ratio remains at relatively low levels compared to the overall five-year trend, while earnings per share are at a five-year high:

ycharts.com

From this standpoint, I see the stock as having the potential for further upside, assuming revenue growth remains on a strong path.

In terms of the company’s strategy going forward, Despegar.com is pursuing an “online-offline” strategy in Brazil and Argentina, with the company opening physical stores to tap the offline market in these countries. The purpose of opening offline stores is to primarily acquire offline customers, while at the same time encouraging future online activity by building trust with these customers. Half the market remains offline in Latin America as a whole, and offline stores and contact centers represent 13% of the company’s bookings.

With ten stores opened across the Brazilian market, I believe this could represent a great opportunity to enhance brand awareness and capture a significant portion of the offline market in the country.

One potential risk for Despegar.com at this time is the possibility of a slowdown in revenue as we approach the months of June to August, which represent the winter season for Brazil. With an expected seasonal slowdown in domestic travel during this time, this may impact overall bookings. However, as detailed under the “Performance” section of this article – we have already seen that total bookings in Q2 and Q3 of last year actually saw an increase versus Q1. In this regard, there is still potential for the company to see growth in this market.

Conclusion

In conclusion, Despegar.com has seen encouraging growth across the Brazilian market and the company’s balance sheet continues to look good. For these reasons, I continue to take a bullish view on Despegar.com.