Abstract aerial art

dispegar.com (New York Stock Exchange: Desp) is the leading OTA company in Latin America.

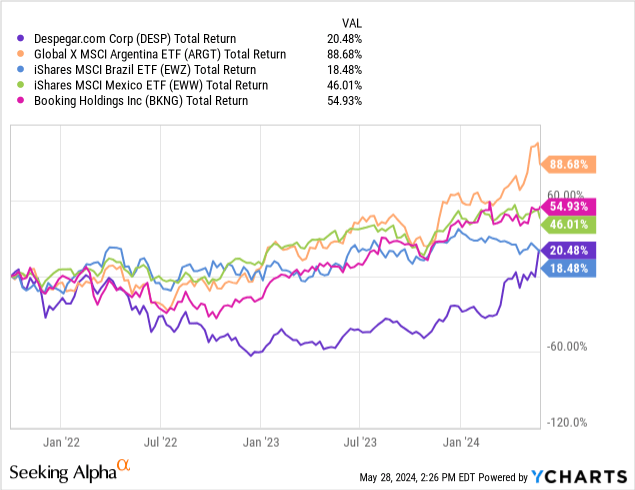

I’ve been covering Despegar since October 2021, with a consistent comment rating. Since then, the stock has returned about 20% versus 16% for the S&P 500 (SPY).). However, the stock has clearly lagged behind broad Latin American indices in Argentina, Brazil and Mexico (its largest markets) and competitors such as Booking (Baking).

My assessment was based on the company’s high valuation compared to its earnings today and its potential in the future. Like most technology companies, Despegar trades at high multiples (today at a P/E of 35x, shown below).

In this article, I review the company’s results and earnings for the first quarter of 2024. In my opinion. Despegar recorded impressive results, achieving 13% year-on-year growth. Moreover, the bottom line results were better, thanks to the rationalization of expenses (especially in… Corporate expenses). We have to make adjustments to the company’s reported numbers to find a true measure of net income. This number is significantly lower than adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) but is still improving.

Overall, I think Despegar’s 35x P/E ratio (from adjusted net income) is very high, even for a growing company. To achieve a positive long-term return for shareholders, companies with high P/E ratios have to achieve a lot of growth. If they don’t, and even more so if multiples shrink, they will disappoint investors. For this reason, I believe Despegar is still pending.

Profitable growth continues

After the pandemic, Despijar began to recover strongly, surpassing the pre-pandemic period. This was true for 1Q24 as well. The top line grew 9%.

Significant growth in Brazil and Mexico: When analyzed by region, we find that Brazil and Mexico recorded overall bookings growth of more than 25%, while the rest of Latin America declined by 8%. Currency depreciation and recession in Argentina are behind the problems in the rest of Latin America. Due to the devaluation of the Argentine peso, the foreign exchange neutral numbers presented by the company (42% growth) are not meaningful.

Low quality of financing incomeIn terms of products, airline tickets decreased by 2%, but this was offset by good growth in offers (14%) and financial services (almost 80%). This last segment provided nearly a third of the growth ($5.6 million out of $15 million). The financial services sector is not a traditional business for travel agencies. Rather, it is the revenue generated from lending in the form of buy now, pay later, and installment options. In my opinion, this type of revenue is much lower quality than that of traditional travel agencies because it has to take into account losses from loan losses. These losses are generally high because people who use BNPL services typically cannot access more traditional credit options (such as a credit card or bank loan), generally because they do not qualify for these products.

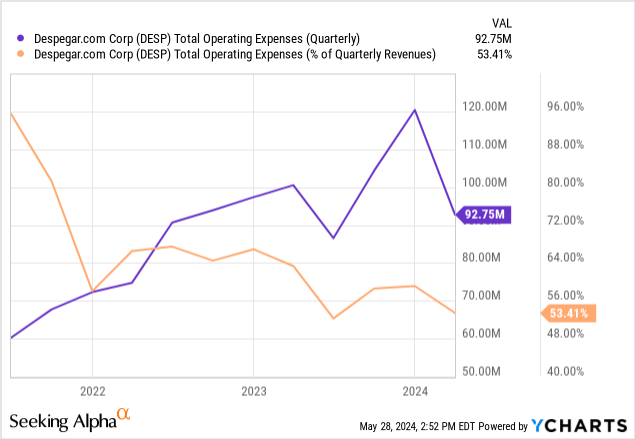

OpEx management is great, but with limitations: Despegar’s operating income expanded nearly 300% to $28 million during the quarter. Revenue growth was part of it, but the bulk came from lower OpEx, particularly in G&A (down 30%), and R&D (down 10%). However, 1Q24 is the last quarter in which the company has the advantage of OpEx declining to revenue levels. Since 2Q23, the revenue OpEx level has been around 55%, which is also similar to the pre-pandemic level. I don’t think the company will be able to continue to benefit from these costs in the future.

The rating is high in the revised guidelines

Despegar’s management reaffirmed its guidance for the year, with revenue up 16% ($820 million) and adjusted EBITDA up 34% ($150 million).

Management has stated that most of this growth will come in 2H24. In my opinion, this last point is a sign of caution, given three factors impacting the company’s markets. First, the value of both the Mexican peso and the Brazilian real has fallen, making foreign travel more expensive for citizens of those countries. Second, Argentina (the company’s third largest market) is experiencing a deep recession, which will likely impact 1H2024 revenues more than the -8% reported in 1Q24.

We can use management guidance to evaluate the company. Starting at $150 million of adjusted EBITDA, we need to remove about $45 million of annual depreciation and amortization, which is similar to the company’s cash capital expenditures. We also need to remove approximately $36 million in factoring costs (annualized from the Q1 2024 fiscal expense of $8 million). Finally, we also need to remove $3 million from stock-based compensation. This results in pre-tax income of $66 million.

From this perspective, we need to apply a tax rate of 30%. This is a combination of the tax rates applied in Mexico (30%), Brazil (35%), and Argentina (35%). The net result is $46.2 million. Finally, we need to remove the $15 million in dividends on the Class A preferred stock (the company’s Class B preferred stock has already converted). The end result is net income to common shareholders of $31 million for the year.

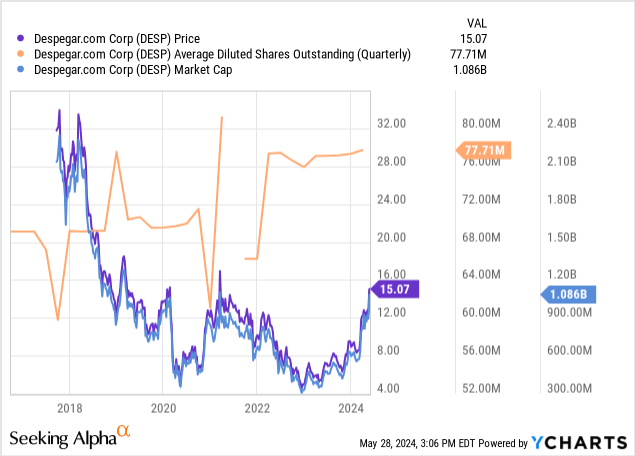

The company’s current market cap is about $1.1 billion, as shown below. This represents a price-to-earnings ratio of 35 times compared to net income to shareholders, as expected above (based on the company’s own guidance).

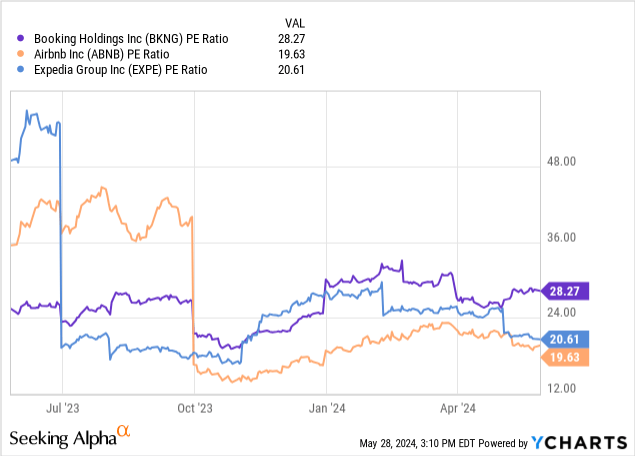

An AP/E ratio of 35x is excessive for almost any company except companies with outstanding quality, high growth, and highly defensible earnings. This is not the case for Despejar, which is growing at a rate of 9% (lower if we remove revenue from lower-quality financial services) in a competitive and discretionary market such as travel agencies. It’s also high compared to peers like Booking, Airbnb, or Expedia, as shown below.

When we buy a stock with a high P/E ratio, we are making a very lopsided bet, which is against our interest. For a stock to deliver a good return, the company needs to continue growing at high rates, and the market needs to continue paying a high multiple for the stock. If neither of these things happen, we may lose money. Moreover, if neither of these conditions occurs (low or no growth, and a shrinking multiple), we could lose a lot of money. In my opinion, this does not represent an opportunity.

For this reason, I still think Despegar is overpriced at these levels.