com.bjdlzx

Diamondback Energy (Nasdaq: Fang) has a joint venture with Five Point Energy, which recently announced a major acquisition. The joint venture, Deep Blue Midland Basin, has acquired Lagoon Operating. This is the second time Diamondback Energy has tried this To monetize the water operational portion of the non-traditional business. Diamondback holds a 30% stake in this joint venture, which is likely to expand to serve the company’s operations over time.

Round 1 – First time

Some longtime readers will recall that Diamondback Energy took Rattler Midstream public as a way to realize the value of its midstream operations. However, management was never satisfied with the value of Rattler Midstream. This was most likely due to the fact that Rattler had an investment in some long-term projects that brought the product to market as well as the collection system, water treatment and related intermediate works.

The money never arrived from the long-term construction projects before management lost patience with the market and repossessed Rattler shares it did not own. The likely reason for the failure to realize value is the challenges of the Corona virus in fiscal 2020.

Western Midstream (WES) to this day notes in its latest corporate presentation that the logistics segment of the market remains historically cheap despite the fact that the industry overall has a healthier way of doing business and a healthier business strategy that seems to be moving forward.

Round 2 – Deep Blue Midland Basin (dark blue)

This time, Diamondback Energy avoided the public market altogether. Instead, the administration chose to create a joint venture for water management work. This means that Diamondback Energy still retains a significant amount of transmission business. But at least part of the business that management no longer wants has been monetized.

Furthermore, since management has a 30% interest, there is significant upside when the average industry periodically recovers. It is very likely that the joint venture will take the water treatment business into the public sector at some point. If that happens, investors should expect a cyclical peak to be “just around the corner” for this type of business valuation.

The above acquisition plus the addition of more customers means that this business will focus on the oil and gas water treatment business while expanding the business to include other customers. So, this joint venture also seems to be a growth story that may eventually go public.

Sell WTG Midstream Holdings

Diamondback and its partners recently announced the sale of WTG Midstream Holdings to Energy Transfer (ET) for a combination of cash and Energy Transfer common units. This represents another step in monetizing long-term midstream operations for more than management thought the market had valued the property at.

The difference is that over time, not only are construction projects not completed, but pipelines are likely to fill up. This may have resulted in a cash dividend that Rattler Midstream holders never saw. When Rattler Midstream went public, it was more about construction contributions followed by a promise of cash receipts that never came before Rattler was reacquired.

Whether waiting would have made a difference in the outcome for Rattler holders is anyone’s guess, because Diamondback Energy’s management has taken matters into its own hands to capture value for some assets while retaining the local collection system that was part of Rattler.

Evaluation progress from the last article

The last article discussed the valuation, as the stock price saw a nice rise after the announcement of the Endeavor acquisition. If the stock price was reasonable at the time (and it was), all of these monetization and acquisition efforts would only make the stock price a better deal. The price has declined somewhat since the last article, but efforts to monetize some assets should result in increased value per share if management is heading in the right strategic direction.

Shareholders have already approved the issuance of shares to complete the Endeavor deal. Now the only thing left is regulatory approval for the merger. This will take time. But it’s also fairly routine.

Management history creates value

Below is the management log. The caveat is that it is worth different amounts depending on industry and economic conditions.

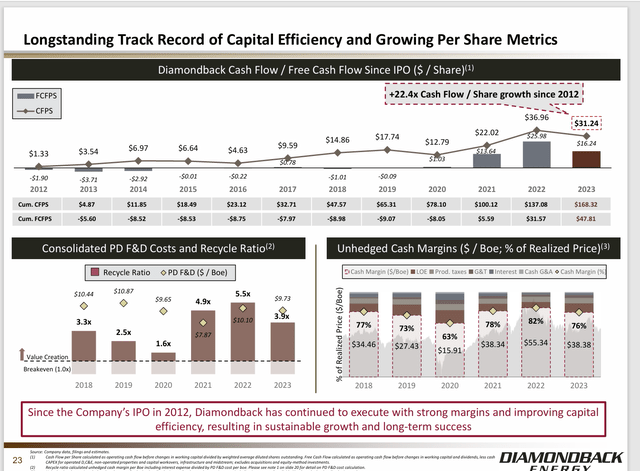

Diamondback Energy summary of per share value creation (Diamondback Energy Q1 2024 Presentation)

This management has a very long history of increasing stock value. The chosen strategy depends to some extent on finding accretive acquisitions. But so far, this is a rare growth story in an industry known as cyclical.

Management used acquisitions to keep costs low. This management also sold non-core space as part of the acquisition strategy.

A key part of the strategy is discovering the rock bottom and development costs outlined above. This is also combined with very low rental operating costs. These lease operating costs are similar to those of dry gas producers compared to other oil competitors. As long as management is able to maintain the competitive advantage of this strategy, it will achieve above-average profitability for the foreseeable future.

summary

Diamondback Energy is that rare company that has managed to continue adding value per share over time in an industry that is known to be cyclical. For this reason, this company remains strong until the growth story changes.

This management found a way to increase headline numbers per share while meeting market demand by paying a decent dividend. This makes the growth story even more remarkable. Most of the companies I follow pay dividends. But growth through acquisitions is a modern industry story that this management has done for too long. This gives this management the advantage of experience when it comes to evaluating acquisition candidates.

The entire oil and gas industry remains historically cheap by many measures. So I don’t worry about “buying lower” now because this is probably a good time to buy. As a result, it takes a lot of effort to overpay. I’ll likely hold on until valuations return to normal, and this company’s growth story changes meaningfully.

Risks

Despite a long history of successful acquisitions, there is always a risk (even if reduced by experience) that the next acquisition will fail to meet management’s expectations or even not be accretive.

This management has led the way in growth through acquisitions. A large portion of the industry adheres to this strategy which leads to a lot of mergers and acquisitions across the industry. As such, acquisition prices can rise to the point where the strategy will no longer work. At that point, management will have to find another way to continue the growth story.

The ability to grow earnings and cash flow per share while driving industry demand requires returns for shareholders, resulting in an unusually large combined return. This yield can at any time go to average yield or worse without warning.

Any company in the oil exploration business is subject to fluctuations in commodity prices and decreased visibility into those prices themselves.

The loss of key employees can hamper a company’s growth and shareholder return plans.