Guido meth

What a difference a few months can make! Back in late September last year, I ran an analysis Dime Community Bank Stock (Nasdaq: Dicom), a modest-sized bank with a market capitalization today Only $775.1 million. At the time, it felt as though the stock was cheap enough to offer some good upside to investors. Ultimately, the stock actually rose, resulting in the upside from the time I rated the company a “buy” through late December of about 42%. But since then, its weak financial position has helped push the stock lower. Fast forward to today, the stock is up just 4.2% while the S&P 500 is up 22.3%.

Given this performance, you would think I would be here reiterating my optimism about the company. But this is not the case. after Given the latest available data, I think it is time to downgrade the rating. Although I would like to see the stock value as it did previously, financial performance has gotten worse and the stock does not look attractive compared to what is out there. The only exception to this is if the stock is cheap. But I would argue that the quality of the institution makes this cheapness justifiable. For this reason, I am officially downgrading the company from “buy” to “hold” to reflect my view that the stock is unlikely to outperform the broader market in the foreseeable future.

Look at the recent weakness

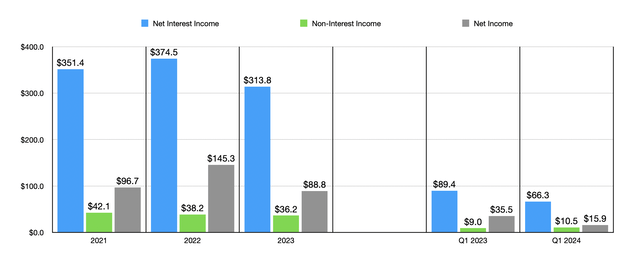

When I wrote about Dime Community Bancshares previously, we only had data covering the second quarter of fiscal year 2023. This data now extends to the first quarter of 2024. Before we get to the latest results, it will be helpful to look at how the year ended 2023. The Foundation’s net interest income for that year was $313.8 million. This is down from the $374.5 million reported one year ago. This was despite the fact that the company’s balance sheet increased significantly. Much of the institution’s pain can be attributed to the fact that its net interest margin fell from 3.25% to 2.46%. But this was not the only weakness the institution witnessed. Non-interest income decreased from $38.2 million to $36.2 million. Combined, this reduced net profits from $145.3 million to $88.8 million.

Author – SEC EDGAR data

When it comes to fiscal year 2024, the weakness has largely continued. Impairments in the value of cash, securities and loans, as well as a contraction in the company’s net interest margin, reduced net interest income to $66.3 million in the first quarter of this year compared to the $89.4 million reported a year ago. It is true that non-interest income increased from $9 million to $10.5 million. But that wasn’t enough to keep net income from falling from $35.5 million to $15.9 million. It’s worth noting that some of that pain was also due to higher expenses, namely a rise in payroll and employee benefits costs from $26.6 million to $32 million, as well as an increase in federal deposit insurance premiums from $1.9 million to $2.2 million.

Author – SEC EDGAR data Author – SEC EDGAR data

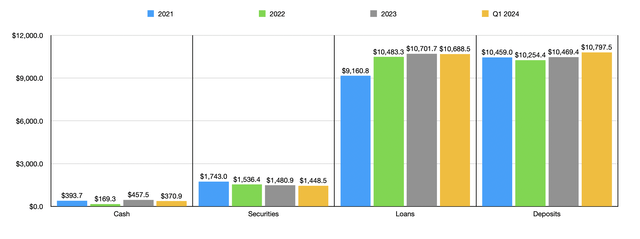

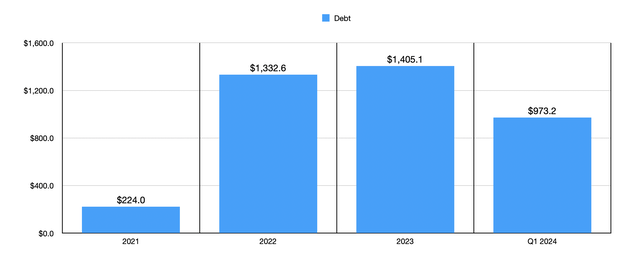

Moving on to the balance sheet, there were both positive and negative changes witnessed by the company. For example, the value of deposits continued to grow. They totaled just under $10.80 billion in the first quarter of 2024. That was up from the $10.47 billion recorded at the end of 2023. On the other hand, the value of securities fell from $1.48 billion to $1.45 billion, while the value of loans declined The company’s books fell from $10.70 billion to $10.69 billion. Even the value of cash and cash equivalents decreased from $457.5 million to $370.9 million. This does not mean that all these declines were in vain. At the same time as this happened, the value of debt on the company’s books declined. At the end of last year, the debt reached $1.41 billion. This number decreased by the end of the first quarter of this year to $973.2 million. Given how high interest rates are, this is a net positive and probably would have been worth the decline in cash, securities and loans.

Author – SEC EDGAR data

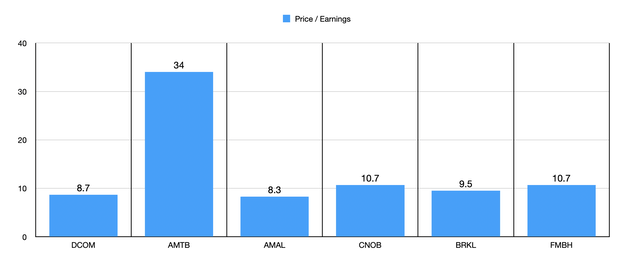

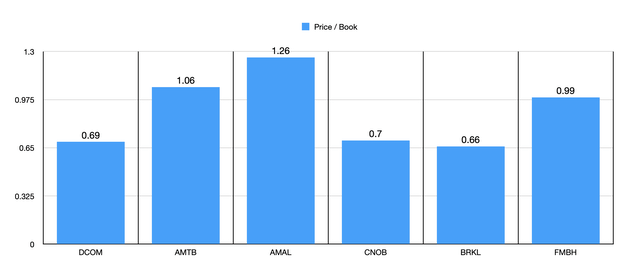

While I am generally negative about declining revenues and profits, I believe the decline in debt and increase in deposits outweighs the decline seen in cash, securities and loans. But there’s more to evaluating this work than just looking at those data points. We also need to consider how cheap the stock prices are. In the chart above, for example, you can see how stocks are priced compared to earnings. You can also see the same for five similar companies that I decided to compare with Dime Community Bancshares. On this basis, only one of the five companies ended up being cheaper. I then did the same thing using the price-to-book approach, as shown in the chart below. With a price-to-book multiple of just 0.69, Dime Community Bancshares is not only objectively cheap, it’s also cheaper than all but one of the five companies I’m comparing it to.

Author – SEC EDGAR data

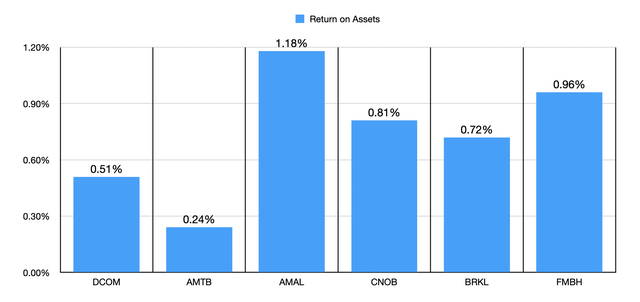

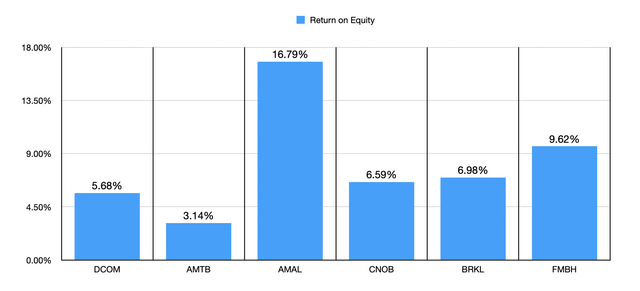

You would think that the combination of increased deposits, lower debt, and lower trading multiples would make me bullish on the business. However, we also need to pay attention to the quality of the assets in question. We can do this in many different ways. In the first chart below, you can see the ROA, not only for Dime Community Bancshares, but also for the same five companies I’ve already compared it to. In this case, four of the five companies are of higher quality. In the following chart, I did the same thing using ROE. And again, I find that four of the five companies are higher than this. Although stocks are cheap, they deserve to be cheap because of the low asset quality we are talking about.

Author – SEC EDGAR data Author – SEC EDGAR data

Away

For people who prioritize valuation over everything else, I can understand why a bullish outlook for Dime Community Bancshares might be the result. But I think the picture is more complex than that. Recent revenue and earnings issues, combined with declining asset quality, are a problem in my book. This justifies, to some extent, the stock trading at a cheap price. Given these factors, I would argue that while there may be upside available for investors going forward, there are likely better market opportunities to be had. As a result, it decided to downgrade the company’s rating to ‘hold’. But if we start to see revenue and earnings improve, it would be easy for me to justify an upgrade to Buy again.