Vasai Budkayo/iStock via Getty Images

I started my bullish view on DocuSign, Inc (Nasdaq: Doku) in March 2024, based on my thesis on the company’s expansion into contract lifecycle management and notary services. The company announced first-quarter earnings On June 6y After the bell, indicating slowing growth in revenues and billings. DocuSign has launched its own intelligent agreement management platform, bringing together its standalone products. I see the product launch as a notable step in their platform roadmap. I repeat a “buy” rating, with a fair value of $60 per share.

Launching smart agreement management

Intelligent Agreement Management (IAM) combines DocuSign’s existing standalone products including eSignature, Contract Lifecycle Management, and DocuSign Maestro. I see the launch of the platform as an important milestone for the company to expand its target markets. The main reasons are:

- A unified platform can make selling a product much easier From independent products. Within the same IAM platform, enterprise customers can subscribe to different servers. An IAM platform can improve sales team productivity and boost a company’s profit margins.

- DocuSign provides Navigator, a service that stores and manages agreements in the cloud. Through these services, IAM can help customers create, execute, store and manage all types of agreements, adding value and improving efficiency for customers.

- DocuSign develops custom IAM for specific verticals, such as customer experience, sales, legal, procurement, etc. These IAM platforms can allocate specific functionality to these sectors.

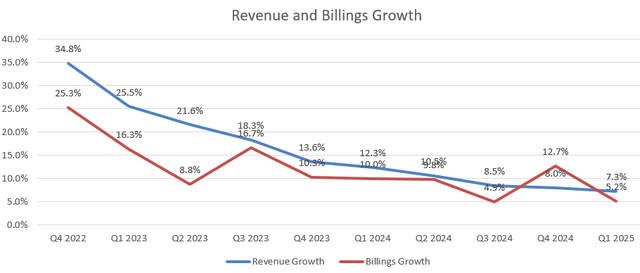

In Q1FY25, DocuSign achieved 7.3% revenue growth and 5.2% billing growth, indicating a deceleration trend compared to past quarters. As described in my startup report, DocuSign needs to grow beyond the traditional e-signature market, expanding into contract lifecycle management and notary services.

DocuSign quarterly earnings

I think the slowdown is caused by several factors:

- DocuSign has already gone through a period of rapid growth, with its e-signature penetration growth peaking. As noted in my start-up report, I expect DocuSign’s revenue growth to begin to return to normal in the post-pandemic period. In other words, the company is unlikely to achieve double-digit revenues in its core business in the future.

- To reduce operating costs, companies are likely to adopt cheaper IT solutions for e-signature. DocuSign is currently in the contract renewal cycle, and the timing of the renewal may impact billing growth each quarter. The current difficult macro environment is not suitable for customer contract renewal, especially for small and medium-sized customers.

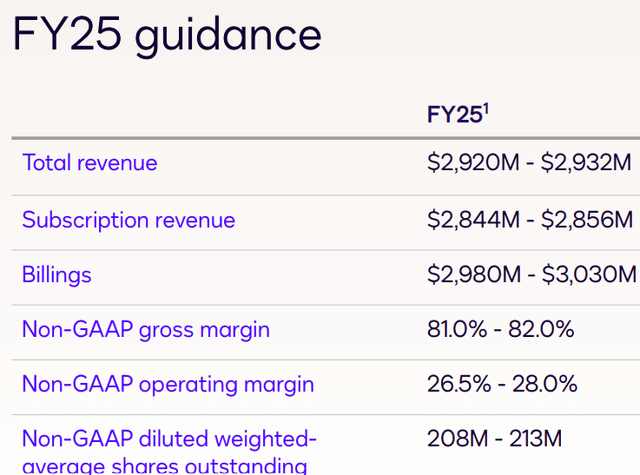

FY25 forecast

While I expect DocuSign’s growth to continue to return to normal, I remain optimistic about its growth in other adjacent regions and its IAM platform.

In fiscal 2025, the company expects revenue growth of 6% and billings growth of 4%, as detailed in the table below.

DocuSign Investor Presentation

I estimate that DocuSign can achieve 6% revenue growth in the near future, based on the following assumptions/reasons:

- During the global pandemic, the market was overly optimistic about the potential growth of the electronic signature market. For example, Prescient Strategy Intelligence forecasts that the e-signature market will grow at a compound annual growth rate of 26.6% from 2021 to 2030. In the post-pandemic era, these forecasts have proven overly optimistic.

- DocuSign has built a leading position in the electronic signature market, and it will be very difficult for it to increase its market share in the future. There are many e-signature providers on the market today, as a simple Google search will show. As such, I do not assume that DocuSign will continue to gain market share in the future.

Google result

I assume that renewing their existing customers will contribute to 4% growth in total revenue, based on their historical billing growth. In addition, I expect the company to achieve another 2% growth from adjacent businesses such as contract lifecycle management and notary services as well as its recently launched IAM platform.

evaluation

As analyzed, I assume DocuSign will deliver 6% organic revenue growth in the near term. In the DCF model, I assume that the company will allocate 3% of revenues to mergers and acquisitions, contributing to an additional 1% growth in total revenues.

In Q1FY25, the company spent $149 million on stock buybacks, a significant increase from $40 million last year. However, since the Company has allocated more than 22% of revenue to stock-based compensation (“SBC”), stock repurchases are insufficient to offset SBC dilutions. At discounted cash flows, I think the total number of shares outstanding will increase by 1.3% per year.

I expect DocuSign’s margin expansion to come from the operating leverage of sales and marketing expenses. The company reduced sales and marketing expenses as a percentage of total revenue from 60.7% in fiscal 2020 to 42.3% in fiscal 2024. I expect this trend to continue in the future, as DocuSign increases its direct online channel to sell its services. I assume operating leverage of 140 basis points from future sales and marketing.

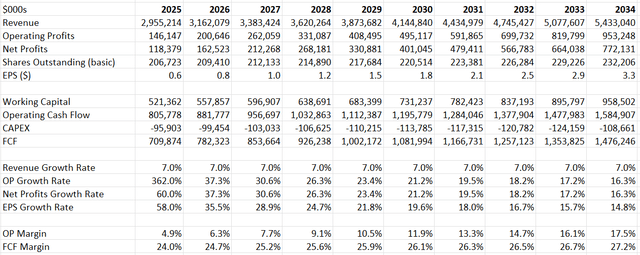

DocuSign DCF – Author Accounts

The weighted average cost of capital is estimated at 15% assuming: a risk-free rate of 4.2% (10-year US Treasury yield); Beta 2.23 (Seeking Alpha); Equity risk premium 5%; Equity balance $1.12 billion; Debt $0; The tax rate is 19%.

Discounting all future free cash flows, the fair value of its stock price is estimated at $60 per share.

Risks

I see the biggest risk for DocuSign as increasing competition in the e-signature market. Notably, Adobe (ADBE) is a strong competitor in the market, and Adobe has several flexible plans that offer PDF and e-signature services to both individual and enterprise customers.

Compared to other IT platforms, eSignature is easier to switch from one vendor to another, as migration costs are not material for enterprise customers. As such, DocuSign needs to continue its innovation in the electronic signature market to maintain its leadership position.

In addition, DocuSign’s SBC spend is very high compared to other IT companies. Unless its revenue growth accelerates in the future, it will be difficult to justify its high spending on SMEs.

Judgment

I see DocuSign’s launch of the IAM platform as a smart strategy to integrate its standalone products, increase sales productivity, and create value for its enterprise clients. I expect that the company’s strategy to expand into neighboring regions will contribute to additional growth for the company in the future. Therefore, I reiterate a “buy” rating at a fair value of $60 per share.