Dollar Tree Q1: Strategic Alternative Shows Hope, Family Dollar Weakness Continues (DLTR)

J. Michael Jones

dollar tree (Nasdaq: DTR) operates discount stores, selling discounted items such as single-use utensils, toys, vases, and batteries, with most products sold at a fixed price of $1.25 within the Dollar Tree segment. In addition, the company operates general retail discount stores under Family Dollar A sector with a more intense focus on consumer sales. Over the long term, Dollar Tree’s returns have been good with a ten-year compound annual growth rate of about 8.4%.

Ten year stock chart (Searching for Alpha)

The company announced first-quarter results on May 5y In June, before market hours, it was reported that the process of reviewing strategic alternatives for the Family Dollar segment had begun. The stock opened with a neutral reaction to the news as financial conditions continued to stabilize, but the reaction has since turned slightly negative as the market digests the news. News.

Stable financial report for the first quarter

Dollar Tree reported the company’s first-quarter results on the fifth dayy From June. Reported revenues grew 4.2% year over year to $7.63 billion, missing Wall Street analysts’ estimates by a narrow margin of $40 million. Adjusted EPS came in at $1.43, in line with expectations – overall, the quarter saw results roughly in line with expectations with continued stable demand for the company.

Fiscal 2024 forecasts, including revenue of $31 billion to $32 billion and adjusted earnings per share of $6.5 to $7.0, were reaffirmed and are in line with consensus estimates; Dollar Tree continues to see quite stable demand and continued modest growth in the Dollar Tree segment.

The company also gave an outlook for the second quarter, forecasting sales of $7.3-7.6 billion in the second quarter along with adjusted EPS of $1.0-1.1, with consensus estimates at the high end of the revenue range. Adjusted EPS was estimated at $1.2 as reported by Seeking Alpha, above guidance provided. Q2 guidance assumes a $0.1 charge due to hurricane damage at the distribution center, and full-year FY2024 guidance assumes a total charge of $0.2 to $0.3 EPS.

Long-term financial vision

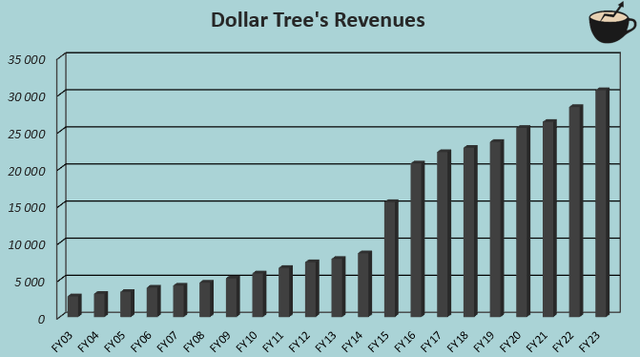

Dollar Tree has been able to increasingly expand its store network, increasing sales in a consistent manner. In 2015, the company purchased Family Dollar shares, causing a rally in fiscal years 2015 and 2016. Excluding the two-year growth fueled by the acquisition, Dollar Tree achieved a revenue compound annual growth rate of 8.8% from fiscal year 2003 to fiscal year 2023.

Author’s calculation using TIKR data

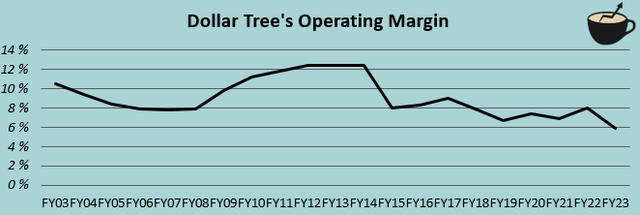

The Family Dollar acquisition had a very negative impact on Dollar Tree’s margins, as operating margin went from 12.4% in FY 2014 to just 5.9% in FY 2023, with a significant decline initially due to Family Dollar’s weak margins, but since then also with Small margin continues to decline. Despite being a discount retailer, Dollar Tree is not as resistant to macroeconomic disruptions as many other retailers, especially grocery chains – most of Dollar Tree’s revenue comes from discretionary products, where demand depends on customers’ purchasing power, resulting in a lower margin operating by 2.1 percentage points in fiscal year 2023.

Author’s calculation using TIKR data

Historical growth was driven by capital expenditures, with Dollar Tree having about $2.1 billion in FY2023 which significantly deteriorated cash flows. In the first quarter alone, the company opened 116 new Dollar Tree stores and 41 Family Dollar stores, and continued high capital expenditures of $472.2 million in the quarter — with a five-year average return on capital of 7.1%, not growing Dollar Tree Growth. Come cheap.

Dollar Tree reviews strategic alternatives for Family Dollar

In a separate press release, Dollar Tree announced that the company is reviewing strategic alternatives for the Family Dollar business, leading to a possible sale or spin-off of that segment. JPMorgan will act as financial advisor in the review process.

The announcement comes after Family Dollar reported weaker growth than the Dollar Tree chain — for example in the first quarter, Dollar Tree same-store sales grew 1.7% compared to Family Dollar’s growth of just 0.1%, following a long trend of weak financial performance for Family Dollar. . In fiscal 2023, Family Dollar generated $13.8 billion, or about 45.2% of the company’s $30.6 billion in revenue, but well below the company’s adjusted operating income. For example, in the first quarter, the Dollar Tree segment reported a GAAP operating margin of 12.5% compared to a regular Family Dollar margin of just 1.5%. Since this segment represents a large portion of the company’s revenue, the potential deal still seems like a significant event.

Dollar Tree has already begun a review of its Family Dollar store portfolio, and plans to close approximately 970 Family Dollar stores for a total of 7,877 after the first quarter. After the first quarter, 550 planned closures have already occurred, and an additional 150 closures are scheduled to be completed before the end of fiscal year 2024 – approximately 5.3% of existing stores are still scheduled to close as many Family Dollar stores do not generate sufficient revenue on top of the money.

Dollar Tree acquired Family Dollar in fiscal 2015 after announcing the intended acquisition the previous year. The acquisition was made at an enterprise value of approximately $9.2 billion. At the time, Family Dollar had about 8,200 stores nationwide, fewer than its current store count of 7,877 due to ongoing store closings that conflicted with investments being made in new stores. Given the current financial performance, and Family Dollar’s slightly smaller operations, I think there will likely be less than $9.2 billion consideration for this segment in a sell or offer scenario.

I think that despite the potential lower valuation for this segment than it had in the acquisition completed in FY15, a strategic review could be a good move from Dollar Tree. As noted in the press release, the segments could focus more on growth as separate companies. The long-term operating margin trend following the Family Dollar acquisition also speaks volumes that favor strategic alternatives, and the trajectory of gross earnings as separate companies could be improved.

Evaluation: Strategic alternatives could provide some upside

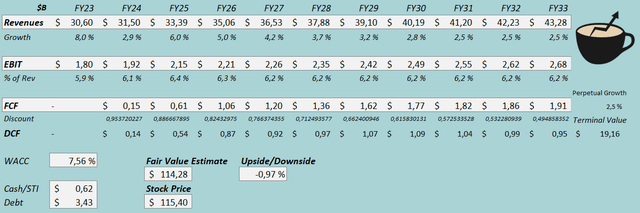

While strategic alternatives remain uncertain, I value the company with a discounted cash flow model for total operations (DCF model). In the model, I estimate the midpoint of FY2024 revenue guidance, and 6.0% growth in FY2026 due to store expansion and store closures having less impact. With continued investments, I expect a gradual slowdown to a sustained growth of 2.5%, representing a total revenue CAGR of 3.5% from FY2023 to FY33.

For EBIT margin, I estimate some leverage of 6.5% in FY2025 after a stable FY2024 as Family Dollar store closures improved profitability. After that, I expect a decline to a sustainable level of 6.2% given the weak margin trajectory over the long term. It appears that store openings will worsen cash flows significantly in the coming years, but I estimate cash flows will improve as growth slows.

The discounted cash flow model estimates Dollar Tree’s fair value at $114.28, close to the stock price at the time of writing. The stock appears to be roughly valued right, with strategic alternatives adding some upside in a bullish scenario. However, I do not necessarily consider the stock to be a high-risk-reward investment at the current price level, as considerations for the Family Dollar sector appear to be very weak.

Discounted cash flow model (author’s account)

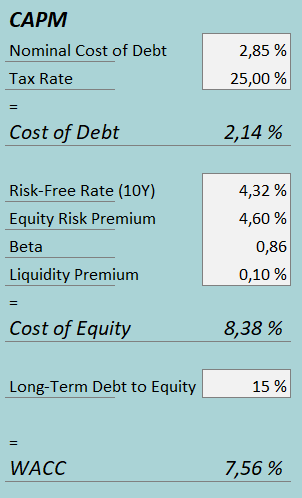

A weighted average cost of capital of 7.56% was used in the DCF model. The weighted average cost of capital (WACC) used is derived from the capital asset pricing model:

CAPM (author’s account)

In the first quarter, Dollar Tree had $24.4 million in interest expense, putting the company’s interest rate at 2.85% with the current amount of interest-bearing debt. I estimate that the debt-to-equity ratio is a fairly modest 15% over the long term.

To estimate the cost of stocks, I use the 10-year US bond yield of 4.32% as the risk-free rate. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the US, updated on 5y January. Seeking Alpha estimates Dollar Tree’s beta at 0.86. Finally, I add a liquidity premium of 0.1%, creating a cost of equity of 8.38% and an average cost of capital of 7.56%.

Away

Dollar Tree reports first-quarter results and begins a strategic review of its underperforming Family Dollar segment. First-quarter results were roughly in line with expectations, and fiscal 2024 looks to continue the mostly flat performance that was slightly dampened by hurricane damage at the distribution center. In light of the company’s long-term performance after the Family Dollar acquisition, and the sector’s poor performance, I view the strategic process as positive even though the valuation of a potential sale looks worse than Dollar Tree’s consideration of an acquisition a decade later. since. The valuation now seems to value the business fairly, and although strategic options can show investors a good upside, I think a hold rating has been formed for now.