Pidgeot

Duke Energy (New York Stock Exchange: Duke) recently signed deals with some of the world’s biggest tech giants. After Goldman Sachs predicted huge electricity demand due to artificial intelligence, Duke could see its forecasts being highly charged.

Duke Energy signs are clean Energy deals with technology giants

Duke Energy has signed agreements with Amazon (AMZN), Google (GOOG) and Microsoft (MSFT) to develop new energy contract terms for zero-carbon power generation investments in North Carolina and South Carolina, Seeking Alpha reported Wednesday.

Duke and the technology companies signed proposals to formulate new pricing structures, designed to reduce the long-term costs of investing in clean energy. The utility company said the new tariffs will create useful generation at customers’ facilities.

US tech giants have been at the forefront of the growth in energy-intensive data centers for generative AI projects. The Electric Power Research Institute can It will absorb up to 9% of US electricity generation by the end of the decade, according to a recent study by the Electric Power Research Institute.

I think the company is well aware of the potential of data centers and has already entered into contracts with some of the biggest players driving the AI engine. This could put Duke at the forefront of the move to meet electricity demand using artificial intelligence.

Goldman Sachs has identified the huge growth potential of electricity

Investment bank Goldman Sachs also recently identified a massive increase in energy demand due to the growth of artificial intelligence.

The bank’s analysts said the United States and Europe will need nearly $1 trillion in investments in renewable energy over the next decade. Goldman said data centers are expected to be a big driver of global demand by up to 160% by 2030.

Other data showed that investment in data centers is up 200% since 2016 with another 89% expected by 2028. Companies like Amazon outlined big plans for AI investment spending in the recent first-quarter earnings season.

Q1 earnings expect strong growth

Duke Energy recently released its first-quarter 2024 earnings, with the company setting its strong growth trajectory through 2028.

Energy growth in Duke (Duke Energy)

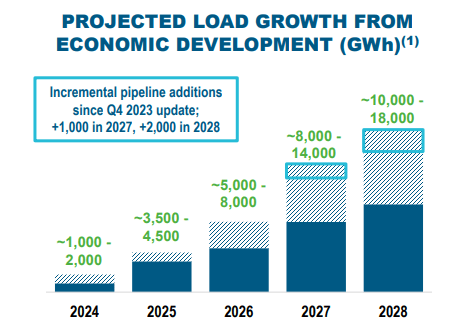

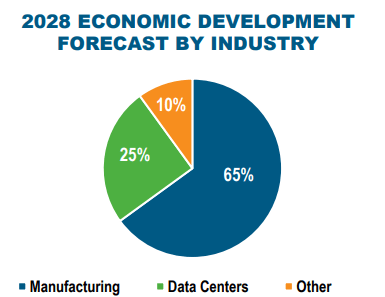

The company’s outlook is driven by manufacturing but data centers are becoming a growing topic.

Duke Energy Sector Outlook (Duke Energy)

Green energy development is driving the manufacturing of huge plants in Duke’s jurisdictions, such as Toyota’s $13.9 billion battery plant in North Carolina and Stellantis and Samsung’s $6.3 billion plant in Indiana. The government’s commitment to green energy could support further subsidies in the future, increasing the positive potential.

Duke’s estimate could also rise by 25% for data centers depending on the success of its AI projects. We’re still at the dawn of AI technology, and if a new product becomes a commercial success, it could create increased demand and more upside for Duke.

First-quarter results saw the company post adjusted earnings of $1.44 per share, beating estimates of $1.38 per share, due to improved weather and the effects of a favorable price condition. Revenue was slightly below expectations, but $1.02 billion in the dominant electricity segment was up from $791 million in the first quarter of 2023.

Load growth in the first quarter increased 2.4% in the Carolinas and Florida. The company reiterated its guidance of $5.85-$6.10, which is in line with expectations.

During the earnings call, CEO Len Judd said the company was on track to “deliver sustainable value and earnings growth of 5% to 7% over the next five years.”

The company also confirmed that it has entered into new contracts for data center billing, which will include take-up or advance payments and infrastructure build-out payments.

Duke Energy Valuation Forecast

According to Seeking Alpha data, I believe Duke Energy is still fairly valued on a five-year basis. Its non-GAAP P/E ratio is -6.27% lower than average, and its enterprise value/sales are largely flat.

This gives investors a margin of safety compared to before and I believe management has a good strategy to achieve the expected annual growth in earnings of 5% over the next five years. GAAP earnings per share grew 6.29% year over year and operating cash flow saw 97% growth over the same period.

The company has had higher earnings per share over the past four years and I think the outlook through 2028 gives investors a chance to jump on the next four years of growth.

The company currently has a dividend yield of 4.1% but is committed to raising that over the long term.

Risks facing the investment thesis

The biggest risk to the investment thesis will be a failure to uptake AI. Front-end chipmakers have dominated the sector and built capacity from the tech giants, but they will need to see companies and consumers embrace AI en masse or else they will need less electricity.

However, there is a rise in the number of companies looking to invest in data centers and the company’s outlook is likely to be safe for at least a year or two in my opinion. The company is currently trading at fair value and economic development from green energy manufacturing dominates the growth outlook.

Update on activist investing

An investor in Duke Energy as of 2020 was activist hedge fund Elliot Investment Management.

The company is in the top 10 and is urging utilities to pursue a tax-free spinoff into three region-focused, publicly traded companies. In a letter to Duke’s board this month, Elliott laid out a plan to create $12 billion to $15 billion in near-term value for the company’s shareholders.

Elliott viewed Duke’s business as underperforming its potential and not maximizing its high-quality assets. Elliott wants to see the company split into three regions: the Carolinas, Florida and the Midwest. The goal is to improve implementation, reduce costs and increase investment.

“Our extensive efforts and conversations with stakeholders have made clear that the Company’s sprawling, non-contiguous facilities portfolio has saddled shareholders with a ‘conglomerate discount’ relative to the value of Duke’s utility franchises,” the hedge fund’s letter said.

Duke responded with a lengthy letter of its own responding to the investment firm’s proposals and outlining its recent outperformance of the S&P 500 and plans to deploy $125 billion of capital over the next 10 years. Management also said the separation came with the risk of “additional costs.”

Conclusion

Duke Energy is a strong utility company that has outperformed its sector over the past year. The company generated strong year-over-year revenue in the first quarter and expects EPS to grow at an annual rate of 5-7% through 2028. This forecast is driven by huge investments in clean energy manufacturing as well as a recent uptick in data center investment. Recent deals with US tech giants taking over data centers are a good sign that lines of communication are open between Duke and those companies. The activists’ letter this month shows Elliott remains an enthusiastic investor in Duke and they could make a more aggressive effort on the electric growth outlook. Duke’s value is just below many of its five-year averages, and that doesn’t account for its 4% dividend yield and expected earnings growth.