Bulat Silvia/iStock via Getty Images

When I first reviewed Duolingo (Nasdaq: Ragdoll) A few months ago, the company was given a “Hold” rating. I was a fan of founder-led businesses, but the valuation seemed overpriced to me. Since then, Duolingo stock has fallen roughly 10% The S&P 500 rose more than 13%.

After an excellent showing in the first quarter and a decline in the stock price, I took a position in the company. Let’s dive into Q1 2024 financial results and the latest company news as I explain why I’m bullish on Duolingo.

Company updates

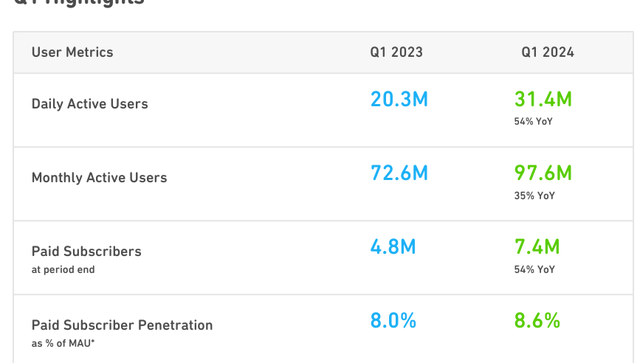

Duolingo had an impressive quarter with the company reporting daily active users (DAUs) of 31.4 million, which represents a 54% increase compared to Q1 2023. The number of monthly active users as well as paid subscribers increased significantly compared to the previous year’s quarter, as This drawing shows who The company in the first quarter of 2024 Shareholders’ letter Clearly explains:

Investor relations

In the first quarter earnings call, management stated that it is focusing on the Duolingo Family plan as well as Duolingo Max. Duolingo Max is the company’s highest subscription tier, which has some generative AI features. Currently, the cap is only available for 5-10% of active DAUs. The company’s CEO, Louis von Ahn, continued this about the current version of the Max, “…We see that there’s a desire among users to get even higher. What you’ll see us doing over the next few quarters is, first and foremost, roll it out, roll out Max in other countries and other countries right now, Duolingo Max is not accessible “Except for people learning French and Spanish on iOS in six countries, we expect it to roll out to Android and in many more countries for learning, which will result in higher usage.”

Regarding Max, von Ahn said the company is experimenting with features to see what works, so Duolingo can eventually figure out how best to pack Max. Once Max rolls out more DAUs, I can definitely see this product being a driver for continued growth.

Regarding the family plan, von Ahn said: “…We’ve found that there’s a lot of desire and desire on the part of people for a family plan. And what we like about the family plan, of course, is that it has a much higher retention rate than our other plans because if you buy a family plan, it has many users in Your family, as long as any of them continue to use it, you’re still on that plan, so it’s been really cool for us.

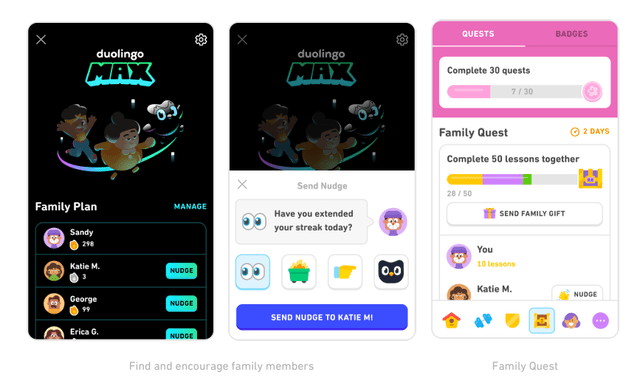

Currently, 18% of Duolingo subscribers are on a family plan. Von Ahn shared that Duolingo is working on new features like “Tasks” so family members can collaborate to reach a common goal. Here are some screenshots of the family plan:

Investor relations

I think Duolingo Max and the Family plan look like great additions to the existing Duolingo offering. As von Ahn noted in his Q1 remarks, as data retention rates rise, I can see Duolingo’s offerings becoming “more consistent” with the family plan.

Finally, Duolingo management saw a huge opportunity for English learners. Von Ahn stated:Although the vast majority of global language learners are learning English, English language learners represent less than half of our daily use units, which is why we see significant opportunity to expand into this segment of the market to increase the number of users and bookings over the next two years. This area of growth, combined with continued momentum in our core product, highlights the tremendous opportunity that lies ahead“.

Von Ahn went on to state that Duolingo’s belief is that there is a $115 billion language learning market, and with English learners accounting for less than 50% of DAUs, it certainly seems like there is an opportunity there.

Finance

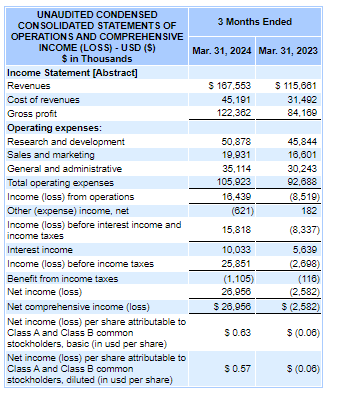

Duolingo delivered another strong quarter with Q1 2024 revenue of approximately $167 million, representing a 45% increase compared to Q1 2023. Total bookings were approximately $197, an increase of 41% compared to Q1 From the previous year. Subscription bookings were approximately $161 million, representing a 47% increase compared to Q1 2023.

This significant revenue growth resulted in Duolingo generating net income of $27 million which is much better than the loss recorded in the first quarter of 2023 as you can see below:

SEC.gov

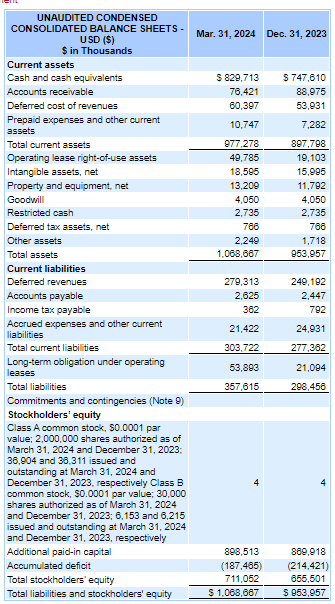

The company has maintained an impressive balance sheet as you can see below:

SEC.gov

Duolingo has a large cash balance that covers all of the company’s liabilities. Duolingo has no long-term debt and most of the company’s liabilities consist of deferred revenue.

Finally, from a cash flow perspective in the first quarter of 2024, cash flow from operating activities was approximately $84 million and free cash flow of approximately $80. These are significant increases compared to the first quarter of 2023, when the company had nearly $30 million of cash flow from operating activities and nearly $29 million of free cash flow in the prior-year quarter.

evaluation

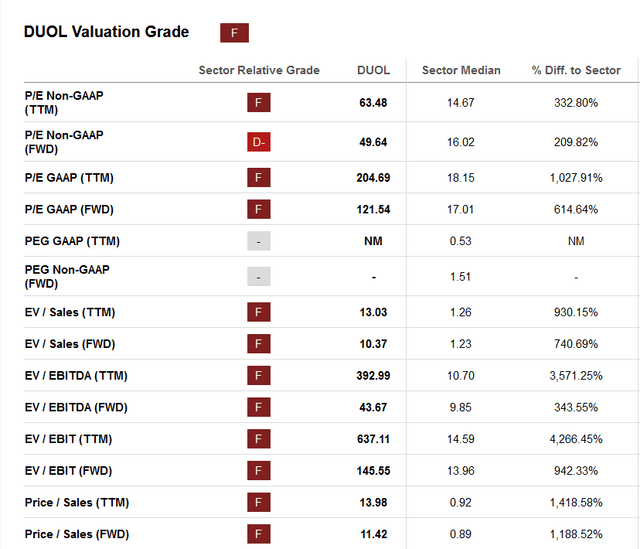

Duolingo is still an expensive stock, and as you can see from the valuation metrics below, Duolingo’s overall Alpha value score is an “F.”

Seeking alpha

In my previous analysis, I mentioned that a company’s price-to-earnings ratio is the ideal valuation metric for Duolingo, but as some comments in my old article mentioned, price-to-sales is probably a better metric for Duolingo.

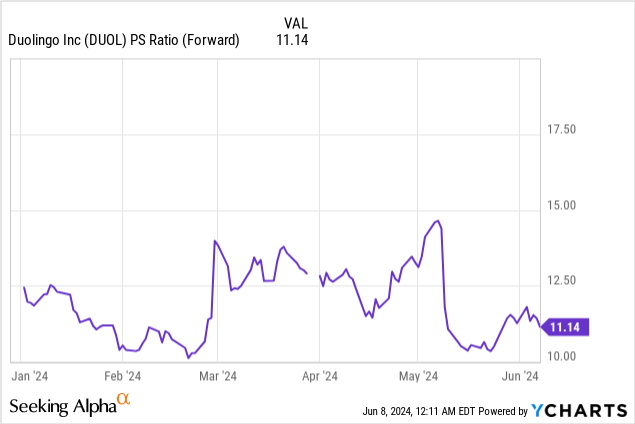

The company’s forward PE is at 11.42 which is definitely still high, although as I mentioned in my introduction, it is lower compared to where it was earlier this spring as you can see below:

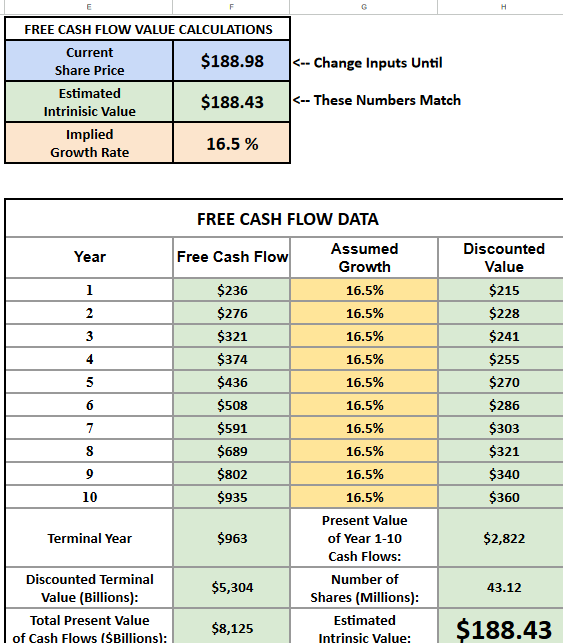

However, using a reverse discounted cash flow model with a discount rate of 10%, a terminal rate of 3%, and an assumed growth of 16.5%, I arrived at an estimated intrinsic value of roughly equivalent to the current stock price:

Arthur model

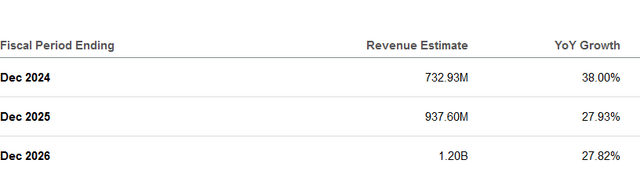

I think Duolingo will grow by more than 16.5% and looking at Seeking Alpha’s estimates this seems to be the correct assumption:

Seeking alpha

The growth rate may not still be high for Duolingo, but even if you use a slightly lower growth rate, like 20%, you get a stock price of $243 using the model above. I think 20% is more reasonable (if not too conservative) and that’s why I think Duolingo is a buy at these current levels.

Risks

Some analysts and investors alike believe that AI systems like ChatGPT will accelerate at a pace that makes its technology less good than Duolingo’s offerings. I would like to point out the difference between a translator and actually learning a new language. There was a recent demo of OpenAI’s GPT-4 that showed off some great translation capabilities. Regarding translation, I believe that AI will make translation much easier and more impactful for users.

However, learning a new language is a completely different situation. Users want learning a new language to be fun and engaging. This is Duolingo’s current competitive advantage. Duolingo has excelled at making learning a new language exciting through play. Furthermore, as I mentioned in my first article, Duolingo has a culture that emphasizes constant testing and experimentation. Through experimentation, Duolingo can learn what works and what doesn’t as it improves its offerings. This philosophy coupled with the fact that Duolingo has more data than its peers puts them in a prime position to use AI to further improve the user experience.

This doesn’t mean that an AI system can’t get similar data as Duolingo and eventually create a competitive offering, but since Duolingo has a first-mover advantage in terms of users and data, I don’t see a competitor coming in quickly and disrupting this business.

Aside from the technology aspect, I think the most likely risk in the short term is a decline in consumer spending. As noted in earnings calls for various companies, such as McDonald’s (MCD) and Target (TGT), consumers are feeling overwhelmed. If consumers cut back on discretionary spending, I could see a decline in Duolingo’s paid subscriber growth. Despite Duolingo’s popularity, I don’t think Duolingo has an offering like Netflix or Spotify, where consumers are willing to pay for their monthly subscription no matter what.

Conclusion

Duolingo had another great quarter as revenue, bookings, active users, and subscribers continued to grow.

Duolingo has some exciting offers rolling out with Duolingo Max and more features on the Duolingo Family plan. I think these offers, especially the family plan, will make Duolingo’s offerings more compelling and less likely that consumers will stop paying for it. There is a huge income opportunity with English learners as well.

Despite the introduction of AI applications like ChatGPT, I don’t think Duolingo has lost its moat or competitive advantage. The company has a massive data set from all of its experiments and has created a great “freemium” model. I think most importantly, Duolingo has created a fun and engaging product and with the help of Duo they have created a very strong and socially relevant brand.

I plan to take advantage of the recent decline in the company’s stock price and add shares. Duolingo is the industry leader in language learning, and with its amazing co-founder at the helm as CEO, I expect Duolingo to continue to grow in the coming years.