Daniel Grzelj

summary

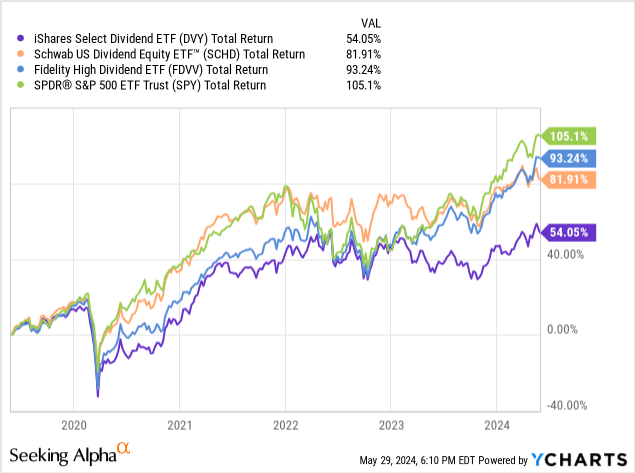

ETFs are a great tool to take advantage of because they give you instant diversification and exposure to some of the best companies in the world. However, not all ETFs are created the same way and this selection process is used The Fund may be left with too many substandard holdings that do not provide a sufficient level of total return. When it comes to dividend ETFs, the goal is usually to earn a higher level of dividend income while maintaining a total return similar to the S&P 500 (spy). Based on past performance, we can see that the iShares Select Dividend ETF (Nasdaq: DVI) is one of the lackluster dividend funds because it underperforms the larger index by a wide margin.

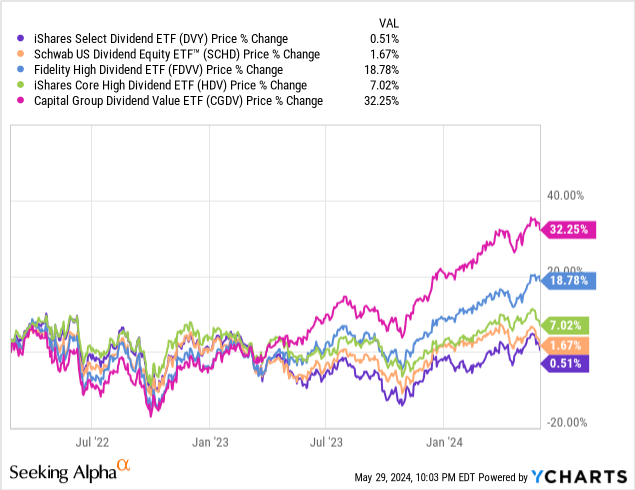

I’ve included a quick comparison of total return versus similarly dividend ETFs like Schwab US Dividend ETF (SCHD) In addition to the Fidelity High Dividend ETF (FDVV). We can see that both of these ETF alternatives outperform DVY by a wide margin of performance over the past five-year period. While the ETF’s stated goal is to track the investment results of a dividend index, I don’t think this is a fair justification for underperformance. Maybe you’re already thinking: “Well, I’m okay with poor performance if it means a higher level of income”! Unfortunately, DVY doesn’t offer the highest dividend yields either.

DVY’s current dividend yield is 3.6%, which is only marginally higher than the peer ETFs I just mentioned. I’ll come back to discuss performance and differences between DVY and some alternatives later. The fund has a very reasonable expense ratio of 0.38%, and DVY has been around for over two decades, with an inception date in 2003. Let’s first start by taking a look at DVVY’s holdings and what diversification looks like.

Possessions and weaknesses

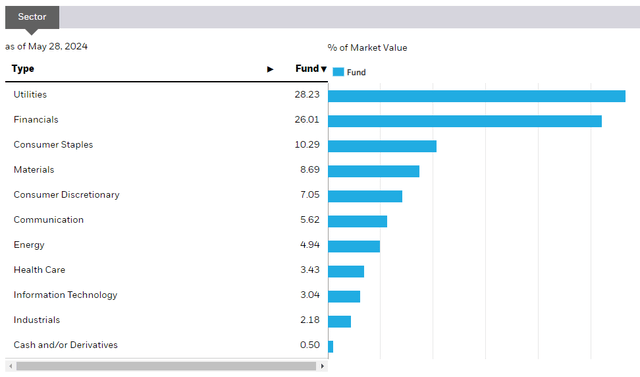

DVY is diversified and provides exposure to many different industries, with a main focus on the utilities sector, which represents 28.3% of the fund. This is closely followed by a 26% overweight in financial stocks. This level of diversification is great because it mitigates any type of concentration risk. However, I am not happy with the low level of exposure to technology. IT represents only 3% of the fund’s weight and I believe this is a big reason why there is little price growth when compared to alternatives.

iShares

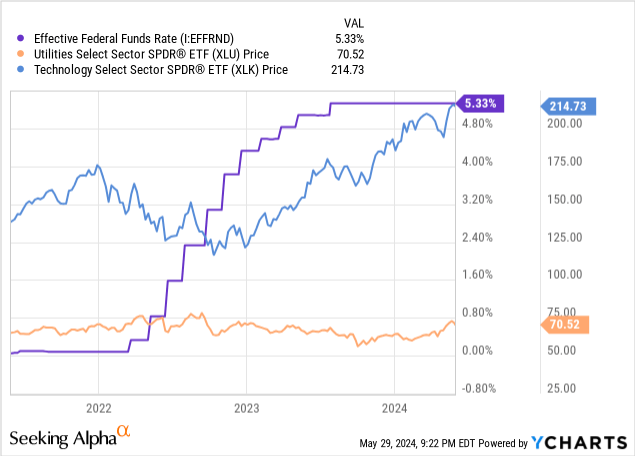

The lack of exposure to technology means that there are plenty of stocks within this ETF that are seeing greater levels of growth. This means that companies like Meta Platforms (META), Alphabet (GOOG), and Nvidia (NVDA) are not contributing to any price growth even though these technology companies are all now paying dividends. Additionally, the focus on utilities means this ETF is more vulnerable to interest rate changes. It is no coincidence that prices have performed poorly since interest rates started rising.

The utilities sector as a whole remains vulnerable to interest rate increases because these companies typically rely on concessional debt to finance operational growth and capital expenditures. As interest rates sit at their highest levels of the decade, this means acquired debt has a higher cost to maintain and may impact profit margins. As a result, there are fewer growth and expansion initiatives at the moment, which contributes to lower returns. We can see that the utilities sector (XLU) is struggling to gain any upward momentum compared to the technology sector.

Since we are currently in a “higher for longer” interest rate environment, I believe the DVY will continue to underperform. While DVY gets the job done, it fails to thrive due to a weak interest rate. Given the continued high levels of inflation and the strong labor market, I believe rates will remain unchanged through the summer. There may be a chance of interest rates being cut by the end of the year, but even if that happens, I think they will be minor cuts given the upcoming elections and ongoing global conflicts.

DVY Fact Sheet

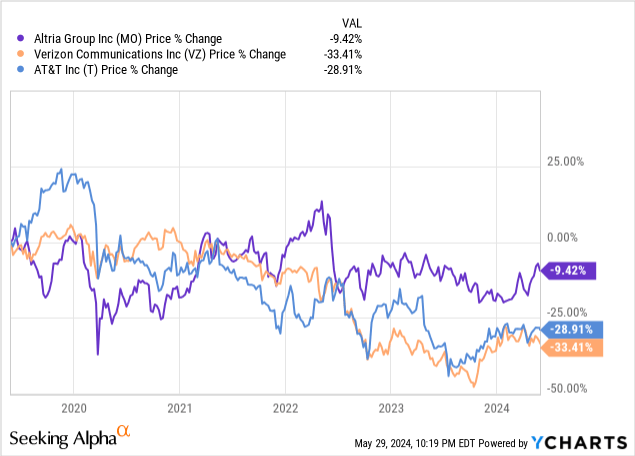

However, DVY gives us exposure to different types of dividend stocks. What I mean by this is that we have a mix of high-yield companies with limited growth, exposure to low initial returns with high growth rates, and middle-of-the-road companies that strike a balance between average return and a decent growth rate. No individual position represents more than 3% of net assets. Altria Group (MO) is the largest single position, closely followed by Verizon (VZ) and AT&T (T). These holdings are likely a large contributor to the fact that DVY’s price performance has been poor. The prices of the three largest holdings have declined significantly over the past five-year period.

Dividends and Valuation

As of the last declared quarterly dividend of $0.9975 per share, the current dividend yield is 3.6%. Since DVY focuses on companies with strong cash flows and that have at least 5 years of dividend history, dividends have naturally increased over the years. For example, dividends have increased at a compound annual growth rate (CAGR) of 7.2% over the past 10-year period. Even if we look at the growth over a smaller time period of five years, we can see that the dividend has increased at a CAGR of 6.3%. Finally, DVY has increased its dividend at a CAGR of 8.1% over the past three-year period.

Dividend growth is an attractive element for investors looking to build a stream of passive dividend income. However, the earnings growth here pales in comparison to its previously mentioned peers. So, if you’re looking for an all-time high for dividend growth, these alternatives may be a better fit for your goals. For reference, here are the dividend growth rates for SCHD and FDVV.

- SCHD: Dividends have grown at a CAGR of 10.8% over the past decade.

- FDVV: hasn’t been around for 10 years but has a strong CAGR of 13.8% over the past three years.

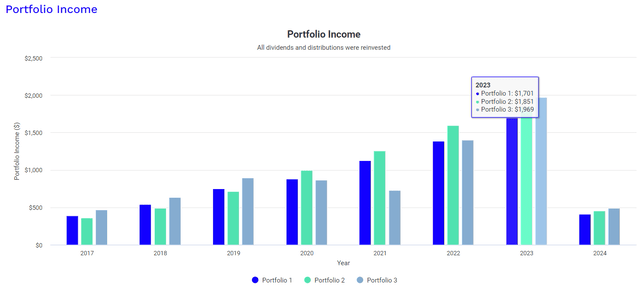

Despite the low level of increases in DVY, dividend growth is still impactful when dividends are reinvested and additional capital is invested at regular intervals, such as a dollar-cost averaging strategy. To visualize this, I created a comparison through the Portfolio Visualizer. This account assumes an initial investment of $10,000, with $250 invested on a monthly basis. This also assumes that dividends are reinvested over the entire holding period. DVY is represented by portfolio 1, the blue line. Portfolio 2 represents SCHD and portfolio 3 represents FDVV.

Portfolio visualizer

Since FDVV is a newer fund, the date here only goes back to 2017. In 2017, the total earnings received from DVY would have been $392. In comparison, dividend income from SCHD was $362 and total FDVV was $471. Fast forward to 2023, we can see that FDVV has outperformed DVY and SCHD in terms of the amount of dividends received. Totals for 2023 would have closed at:

- DVY: $1,701 in dividends received

- SCHD: $1,851 in dividends received

- FDVV: $1,969 in dividends received

In terms of valuation, DVY’s price growth has been disappointing when compared to other dividend-focused ETFs. We can see that over a period of two years, the price of DVY barely moved. However, DVY is currently trading at a price-to-book ratio of 1.69x, which significantly underestimates SPY’s price-to-book ratio. For reference, SPY’s P/B ratio is 3.22x

While it can be difficult to come to a valuation for ETFs, I see limited upside as the best holdings are known for their ability to distribute large amounts of their profits toward dividends. This translates into less capital that can be allocated to growth initiatives and reinvested back into the business. For example, Altria’s dividend yield is 8.6% and its dividend payout ratio is approximately 80%. Likewise, Verizon has a dividend yield of 6.7% with a payout ratio of 60%.

cons

Besides the lackluster performance, an additional downside is that DVY’s dividend yield is not large enough to provide a large enough income stream for a retired investor. A dividend yield of 3.6% means you would have to invest more than $1 million to generate anything close to the livable income required for most places within the United States. For reference, the average per capita income in the United States is about $40,000 as of 2022.

To produce an income in line with the average personal income, you would need to invest more than $1.1 million in DVY. Therefore, if you are looking for high current income as quickly as possible, a combination of business development companies, REITs, or even closed-end funds may be more suitable for you. For example, here are the amounts required to generate the same dividend income of $40,000 when including different asset classes.

- VanEck BDC Income ETF (BIZD): $383,141

- Cohen & Steers Real Estate Investment and Preferred Income Fund (RNP): $487,804

- Janus Henderson AAA CLO ETF (JAAA): $630,914

Unique economic data

While you could argue that less capital would be needed if you were to hold it for a longer period of time and allow compound interest to do its work along with the future dividend growth of the fund, I still think the aforementioned peer dividend ETFs would be a better fit. Both SCHD and FDVV have provided better levels of dividend growth and will eliminate the amount of time you will need to continue investing to eventually produce a large enough income stream.

Away

While DVY gets the job done by providing diversified exposure to many dividend-paying companies, there are much better alternatives that have similar expense ratios while achieving superior price growth through a better portfolio of holdings. I believe that lack of exposure to technology will ultimately remain a large contributing factor as to why price fails to capture upward movement on par with peer ETFs. In addition, the heavy weighting toward the utilities sector means that the DVY is more vulnerable to fluctuations in interest rates. Therefore, I rate DVY a hold because the fund does not excel at anything specific besides having a higher initial return.