Andranik Hakobyan

Persistent earnings stagnation

The US Bureau of Economic Analysis released the second estimate of GDP for the first quarter of 2024. Most notable is that GDP growth was reduced from 1.6% to 1.3%, as expected by analyst consensus.

However, the biggest surprise is that the preliminary estimate for Q1 corporate earnings is -1.7%, well below the consensus forecast of 3.9%, as the table below shows.

Trading economics

In fact, this could be the beginning of another earnings slump, which would require two consecutive quarters of negative growth. There was an earnings recession in late 2021 and early 2022, and then another earnings recession in late 2022 and early 2023.

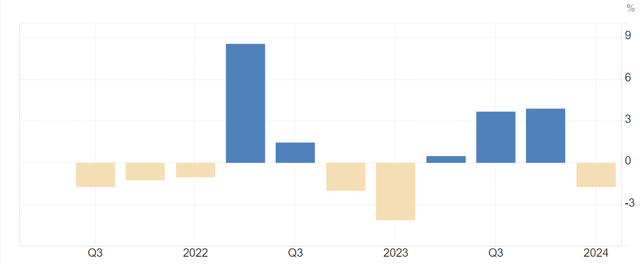

As the chart below shows, after three consecutive quarters of positive corporate earnings growth, the latest quarter saw another negative corporate earnings growth. And so if the next The second quarter (Q2 2024) also shows earnings contraction, and we are back in earnings stagnation.

More broadly, the chart below also shows that out of the last 11 quarters, we only had 5 quarters with positive corporate earnings growth, while there were 6 quarters with negative earnings growth. There’s clearly a long-term earnings slump that was cut short by a few positive quarters.

Trading economics

What is the BEA profit measure?

First, how does the BEA measure corporate profits, as part of the GDI report? BEA measures corporate earnings as follows: Corporate earnings with inventory valuation and capital consumption adjustments.

The BEA defines a capital consumption adjustment (CCAdj) as: “The adjustment used to convert measures of depreciation that rely on historical cost accounting – such as capital consumption allowances reported in tax returns – to NIPA measures of private consumption of fixed capital that are based on current cost with Consistent service life and with empirically based consumption schedules.” So, basically, this is depreciation. Depreciation is a non-cash cost on the income statement.

BEA determines Inventory Valuation Adjustment (IVA) As follows: “An adjustment made in the National Income and Product Accounts (NIPAs) to corporate profits and proprietor income to remove stock ‘profits’, which are more like capital gains than profits from current production.”

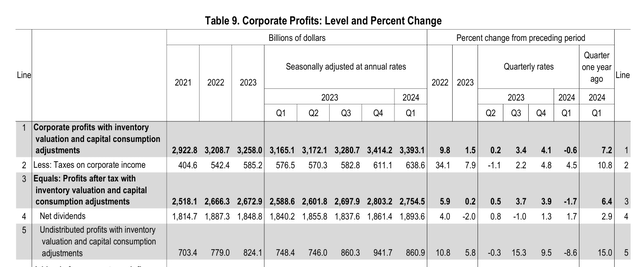

Note that corporate profits after tax excluding CCAdj and IVA grew by 3.2% in Q1 2024. However, BEA’s earnings measure aims to capture real profit growth through accounting adjustment, and this measure was negative -0.8%.

After taking into account the 4.5% increase in corporate tax, corporate profits after tax fell by 1.7%. However, corporate profits rose by 1.7%, despite a decline in after-tax profits, resulting in undistributed earnings falling by 8.8% in the first quarter.

US Federal Bureau of Investigation

Financial versus non-financial

The BEA measure of corporate growth also breaks down the earnings of financial companies, which actually includes the Federal Reserve, and non-financial companies.

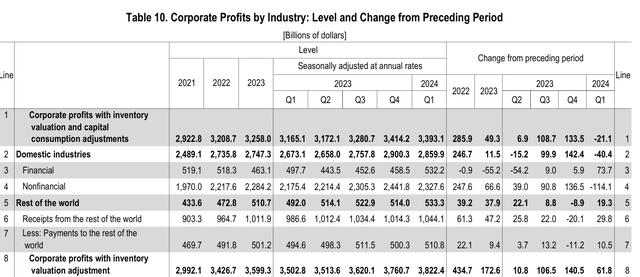

Overall, adjusted corporate profits fell by $21 billion, with domestic industries losing $40 billion, and the rest of the world gaining $19 billion.

Of the domestic industries, the financial sector actually gained $73 billion, including $5 billion lost by the Fed, while the non-financial sector lost $114 billion.

Hence, the non-financial sector appears to be suffering from stagnant earnings.

US Federal Bureau of Investigation

Analysts’ expectations for earnings per share growth

BEA’s measure of corporate profits is broad, across all company sizes and industries. Based on market analysts’ bottom-up EPS metric, we already know that 2023 has been a tough year for corporate earnings, backing up BEA’s earnings metric.

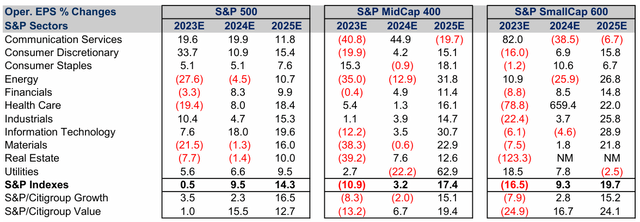

- S&P 500 earnings rose just 0.5% in 2023, driven by 34% earnings growth in the consumer discretionary sector (XLY), mostly from Amazon (AMZN), and 20% growth in the communications services sector (XLC), mostly from Alphabet (GOOG). (GOOGL) and META.

- Mid-cap companies achieved earnings growth of -10% in 2023.

- Small-cap companies achieved earnings growth of -17% in 2023.

Thus, except for a few large-cap companies, overall corporate earnings were negative in 2023.

CFRA

However, analysts expect earnings growth to rebound sharply in 2024.

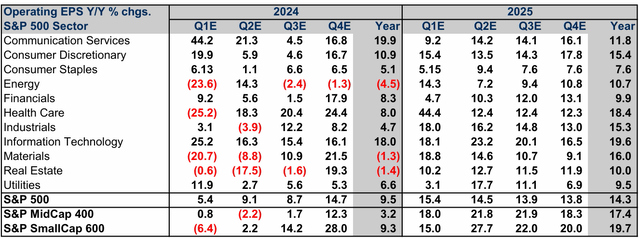

- The current prediction is that corporate profits will increase by 9.5% for S&P 500 companies in 2024 (and by 14.3% in 2025).

- The current prediction is also that corporate earnings will increase by 3.2% for mid-cap companies in the S&P500 in 2024 (and by 17.4% in 2025).

- Additionally, current projections are that corporate earnings will increase by 9.3% for small S&P 500 companies in 2024 (and by 19.7% in 2025).

Furthermore, a bottom-up measure of earnings per share for S&P500 companies shows estimated growth of 5.4% in the first quarter of 2024. This measure would be consistent with GDI’s expected measure of corporate earnings of 3.9%. However, BEA’s initial estimate came in at -1.7%. Thus, there is a disconnect between analysts’ EPS measure and BEA’s Q1 2024 corporate earnings measure.

The analyst-based EPS measure for the first quarter appears to have been skewed by the technology sector’s behemoths ( XLK ), most notably Nvidia ( NVDA ), as well as other larger companies. Based on preliminary data from the Global Growth Index, the rest of the companies, on average, are experiencing stagnant profits.

CFRA

Ramifications

Corporate profits generally decline in economic downturns, usually by 10-15%. Yes, it is possible to have an earnings recession outside of a recession due to a negative earnings impact from one or a few sectors – without systemic effects.

However, widespread negative growth in corporate profits is a reflection of economic stagnation. Therefore, a decline in corporate profits in the first quarter could be a sign of the coming recession.

The S&P 500 (SP500) is not currently priced for a recession. Earnings estimates for 2024 are very high, while official GDP/GDI data show that corporate profits are actually falling.

There is no reason to expect second-quarter earnings to be better than first-quarter earnings – given that interest rates remain tight, the yield curve remains inverted, and excess consumer savings are exhausted. Consequently, S&P 500 earnings estimates are likely to be cut. Additionally, the current stock price multiple of 22 is likely to contract sharply with the onset of a recession. Thus, the S&P 500 faces a significant decline as a stagnant bear market emerges.