Zastavkin/iStock via Getty Images

Introduction and thesis of investing

The beauty of the goblin (New York Stock Exchange: Dwarf) is a multi-brand beauty company that offers high-quality cosmetics and skin care products at attractive prices compared to its competitors. I initiated a “buy” rating on the stock on April 5th My thesis was based on my belief that the company is positioned to capture market share in cosmetics and skincare products, as it drives strong product innovation and worthwhile marketing to engage and convert users across its digital and retail ecosystems. Since then, the stock has outperformed the S&P 500, growing 11.7%.

The company reported its Q4FY24 earnings on May 22, with revenue and earnings growing 77% and 100% year over year for the full year, respectively, beating expectations, gaining market share in cosmetics and skincare products to 10.5% and 1. 6%. , respectively. For fiscal year 2025, management has guided for revenue growth of 21%. Adjusted EBITDA margin of 23%. While this represents a deceleration from FY24 levels, I am impressed by the company’s go-to-market and product innovation strategies as it looks to expand its space across retail locations in the US and internationally, while building solid product franchises to drive engagement and customer spending.

Although I’m a little concerned about the potential for diminished ROI on marketing spend in FY25, especially in the event of a macroeconomic slowdown resulting in margin pressures, I think the stock price is attractive given the risk reward, making it a ‘buy’.

The good: Accelerated market share growth in cosmetics and skincare, with global expansion, coupled with strong digital and retail go-to-market strategies and continued product innovation.

Elf Beauty reported Q4 FY24 earnings, with revenue rising 77% year over year to $1.02 billion for the full year, with Q4 marking its 21st consecutive quarter of market share gains as it outperformed across its pillars The three that include color cosmetics, skincare and international expansion.

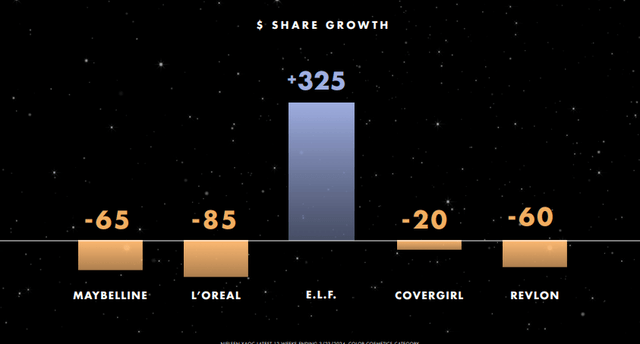

In Q4, elf Cosmetics achieved 30% growth when the entire category declined 3%, allowing it to gain an additional 325 basis points of market share to 10.5%, a sequential rise from 10.1% in Q4. Meanwhile, elf Skin grew by 38%. , outpacing the category by 19-fold and increasing its market share by 45 basis points to 1.6%, which also grew sequentially from 1.4% in the third quarter, driven by the biocompatible skincare brand Naturium which it acquired in October last year. Regarding international expansion, net sales increased by 115% year over year in the fourth quarter, contributing 16% of net sales, compared to 13% in the previous year. This was led by geographies including Canada and the UK, where it is the fastest growing among the top 10 cosmetics brands.

Q4FY24 Earnings Slides: Market Share Growing in Elf cosmetics

I believe there are three key drivers of its outperformance across its growth pillars which include a) its strong value proposition of offering high quality products for every eye, lip and skin at compelling price points, with an average price of $6.50, compared to $9.50 $20 for legacy cosmetics brands and $20 for prestige brands, b) a culture of product innovation, where it focuses on launching lasting product franchises, such as expanding its Power Grip franchise into the spray category with the launch of a $10 Power Grip Dewy spray setting, compared with a $38 prestige equivalent, resulting in a 2x increase in sales, and c) engaging with their customers through unique and creative moments with their disruptive marketing engine, allowing them to reach new audiences beyond Gen Z and create brand awareness.

Meanwhile, the company also saw a 70% year-on-year increase in its digital consumption, with digital channels contributing 22% of total consumption, compared to 18% the previous year. I believe this is driven by growth in the number of members in Beauty Squad’s loyalty program, which stands at 4.8 million, up from 4.5 million in the previous quarter, as they play a key role in their digital ecosystem, driving 80% of total sales on elfcosmetics.com. At the same time, the company’s management also continues to focus on expanding its retail footprint to capture market share by replicating the playbook success of Target (NYSE:TGT), where it is the No. 1 brand with over 19% share. During the earnings call, management discussed that they will expand space with CVS (NYSE:CVS), Walmart (NYSE:WMT) and Ulta Beauty (NASDAQ:ULTA) during the year, which I think will help Elf Beauty take over some white space, especially In the skin care category.

The bad: While profitability expands, marketing ROI can shrink if demand declines due to macroeconomic pressures

Although the company generated $234 million in adjusted EBITDA in fiscal 2024 which grew over 100% year over year as it benefited from improving unit economics such as improvements in transportation costs, and inventory adjustments, And international rate increases, I think we need to pay attention to the ROI of SG&A spending going forward. In FY24, the company spent 51.4% of its net sales on SG&A expenses, up from 50.6% the year before. During the earnings call, management claimed that it ended the year with marketing and digital spend (part of SG&A) of 25% of sales, higher than the 22-24% range it had originally guided. So far, the ROI from their marketing initiatives is yielding results, such as their partnerships with Liquid Death to launch Corpse Point which led to a triple increase in traffic to elfcosmetics.com and the collection sold out in 45 minutes, with 68% new elf buyers

At the same time, as management looks to drive growth through its international strategy by expanding the retail space with Superdrug in the UK, Boots and Shoppers Drug Mart in Canada, and Sephora in Mexico, among others, I believe the return on marketing spend needs to improve. These should be watched carefully in order to assess the profitability landscape, especially if we see a slowdown in revenue growth due to macroeconomic pressures. As interest rates remain high for longer in the United States, coupled with a weak labor market and record high credit card debt, we may see a slowdown in consumer demand, which will result in a decline in the number of units purchased per customer. Given that the company is already selling its products at “cheaper” prices compared to its competitors, a decline in units purchased will certainly put profit margin pressure on the company, forcing it to heavily discount its products, especially at a time when it has built up its inventory by 135% year-on-year to $191.5 million.

For fiscal 2025, management expects to spend approximately 24-26% on marketing spend with an EBITDA margin forecast of 21-23%, which would be in a similar range to fiscal 2024 adjusted EBITDA margins.

Reconsidering my review: Imp remains a ‘buy’

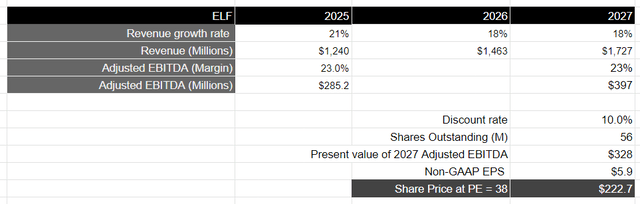

Looking ahead, the company expects its revenue to increase 21% year-over-year to $1.24 billion with adjusted EBITDA of $287 million, representing year-over-year growth of 22% and a margin of 23%. Management’s revenue forecast of 21% is lower than my previous estimate of 27%, which I talked about in my previous post. While this represents a deceleration from the 77% annual growth rate in FY24, I believe management has likely taken into account some potential macroeconomic headwinds weakening consumer demand while setting FY25 revenue guidance. I believe that given management’s execution To date and future growth strategies it has in place to gain market share across the cosmetics and skincare segments, while expanding its digital and retail footprint in the US and internationally, as it drives strong product innovations and engages its employees and user base through memorable brand moments, must Being able to grow in the high teens range over the next two years through FY27, translating to total revenues of $1.7 billion over this time period.

From a profitability standpoint, assuming the company is able to continue to pay targeted price increases along with inventory adjustments to improve unit economics while maintaining a consistent ROI on marketing spend while continuing to delight and convert its users, it should maintain its adjusted EBIT margin and EBITDA of 23%, which would translate to adjusted EBITDA of $397 million in fiscal 2027, equivalent to the present value of $328 million when discounted at 10%.

If we take the S&P 500 as a proxy, whose companies grow their earnings on average by 8% over a 10-year period with a price-to-earnings ratio of 15-18, I think Elf Beauty should trade at least at a 2-2.25x multiple given to the growth rate of its profits during this time period. This would translate into a price ratio of 38 or a target price of $222, which represents an upside of 22.36% from its current levels.

Author evaluation form

Although the aggressive level of marketing spend required to engage and convert its users while gaining increasing market share both in the US and internationally is an area of concern, especially if the ROI from lower consumer demand diminishes in the event of a potential macroeconomic slowdown, Led to margin pressures, I believe the stock is attractively priced at current levels, especially given the white space of opportunity still ahead of it and the superior growth rate compared to its competitors which include L’Oréal, Estée Lauder (NYSE:EL), Coty (NYSE:COTY) , Revlon, and others. So far I have been impressed with management’s execution, and I believe they will continue to deliver superior results given their long-term growth and product innovation strategies and their mission to deliver quality products at compelling prices, creating a sense of community and loyalty around their product. Rating both ‘good’ and ‘bad’, I believe there is still room for upside in the stock, hence I would rate it as a ‘buy’.

Conclusion

I think the troll’s growth story has more room to grow, given the amount of white space in the cosmetics and skincare category. I love how the company is driving strong product innovation coupled with memorable marketing moments to drive engagement digitally and at retail locations in the US and internationally to reach new audiences. Although the ROI on its marketing spend will be scrutinized if the company sees a slowdown due to short-term macroeconomic pressures, I think the share price is attractive from a risk-reward standpoint, making it a ‘buy’.