com. aluxum

Overview of the electoral management body

The iShares JP Morgan USD Emerging Markets Bond ETF (NASDAQ:EMB) is designed to gain exposure to US dollar-denominated bonds issued by emerging market countries. US-based investors tend to prefer US dollar exposure Reducing currency risks.

From the perspective of emerging market countries, they see this as an opportunity to capitalize on this demand and will therefore base a significant amount of their issuance on US dollar-denominated debt. These two factors contribute to the size of this ETF, which has net assets of more than $14 billion according to the EMB website.

While the idea of investing in emerging market debt may seem risky, this is somewhat mitigated by the extreme diversification of this ETF. As explained in the EMB product brief, a single investment gives you exposure to over 50 sovereign entities, and over 600 Bonds. More than half of this exposure is to investment grade bonds. This year this combination has produced a portfolio return to maturity generally in excess of 7%.

The ETF pays monthly dividends, and the country’s largest exposures were less than 6% at the end of March this year. At that time for example, there was about 5 to 6% exposure to Saudi Arabia, Mexico, Turkey and Indonesia.

When considering where the EMB stands in terms of the bond universe, it is useful to consider the following snapshot of data released at the end of March this year.

EMB product summary using Bloomberg yield data as of March 31, 2024.

Facts about the Electoral Management Authority Fund

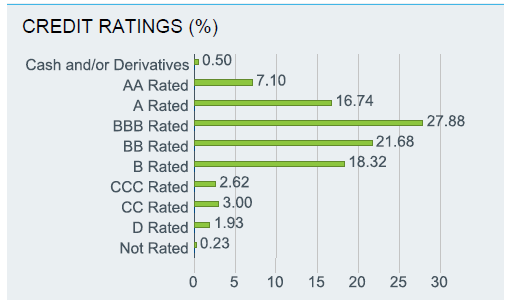

Another notable fact for this ETF is the average maturity of around 12 years, and the effective duration of over 7 years. By earning such high returns, you are taking on some significant risks in terms of sensitivity to interest rate changes.

The decline observed in 2020 is also noteworthy in terms of risk when it comes to the market in a “risk off” environment. I will examine this in the charts below.

This ETF’s fees are a modest 39 basis points, compared to probably more than 1% for actively managed emerging market bond funds. Whether this is “cheap” or not is up to the debate on whether active managers add any value after fees. I will address this discussion in more detail in this article.

Electoral Management Body Fact Sheet 31 March 2024.

Performance history of the electoral management body

Since inception (December 2007) performance figures are listed in the table below:

Electoral Management Body website, data as of May 31, 2024, creation date December 17, 2007.

Admittedly, these performance numbers do not inspire much temptation to invest. But in fairness, it is a timeframe that has largely faced the backdrop of what could be described as a low-yield structural environment for global bonds. This has only really changed in 2022.

With the current high yields on emerging market bonds and the improvement in performance last year, there are even more reasons to invest now. Global inflation concerns in 2022 have eased somewhat.

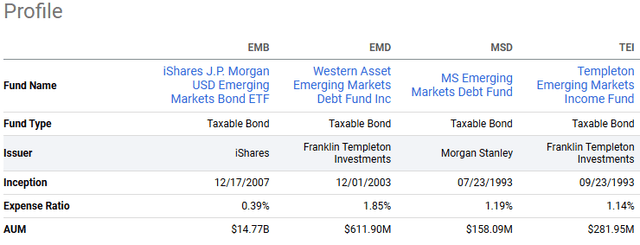

Analysis of their peers in the electoral management body

When comparing an EMB with some other similar trusts that could be considered, I think it would be useful to consider the following.

Compare EMB funds, Seeking Alpha.

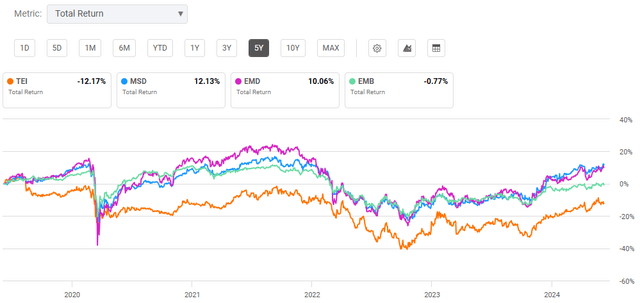

Although I realize that there are 3 closed-end funds targeting higher returns, there are a few reasons why one should consider such alternatives. They benchmark themselves against the JP Morgan USD EMBI Global Index, but take active investment risks, and typically manage portfolios with lower average credit ratings compared to EMBs.

From this perspective, one would expect these mutual funds to perform better in the long run. When evaluating alternatives, we can also take into account the fluctuations that have emerged in recent years.

Total returns for 5 years through June 7, 2024, seeking alpha.

The EMB has outperformed one of the above core efficiency indicators, but is clearly lagging compared to the other two over the past five years. Since this shows total returns, it includes some movement over the time frame in discounts to the net asset value of CEFs. However, these moves were relatively modest, so analyzing the above performance based on NAV returns data only would show a similar result.

It highlights that relying on an active manager can always be a hit or miss. It does provide food for thought though as to whether a passive product like an EMB makes sense with this asset class.

Active or passive management of emerging market debt?

Mutual funds like Templeton Emerging Markets Income ETF (NYSE:TEI), MS Emerging Markets Debt Fund ETF (NYSE:MSD) and Western Asset Emerging Markets Debt Fund Inc (NYSE:EMD) all regularly trade at double-digit discounts. . to NAV in recent years. They charge clearly higher fees than the EMB, but it may be helpful if one subscribes to the theory that active management is preferable in electoral administration.

Not surprisingly, the above article was written by an active manager. However, there are some good arguments favoring positive debt over negative that are unique to emerging market debt. Therefore one should not convey any simple conclusions in favor of negative equity, just because they may believe in the use of negative equity in the United States.

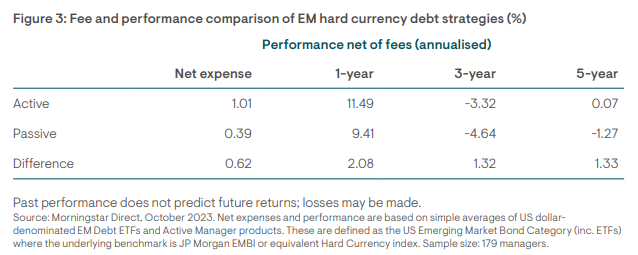

Referring to the study I linked in the previous paragraph above, I found the following table interesting. Even recognizing that looking at the past five years is never a definitive guide to future performance; It’s still worth being aware of. This means that in hindsight, you may have been better off with the “expensive” active manager fees.

Live Morningstar study as of October 2023 via ninetyone.com

Regarding the CEFs I mentioned above, earlier this year I reviewed MSD which was my favorite choice in this area. EMD I would argue it’s not too far off from that though.

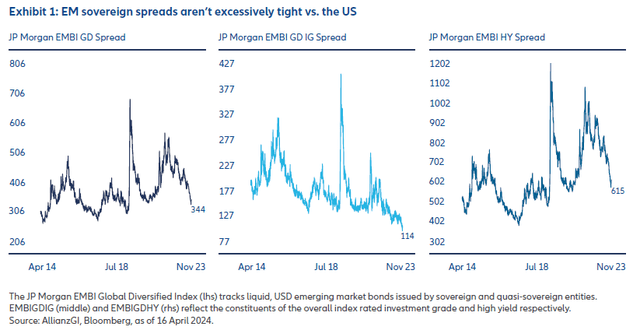

Sovereign interest rate spreads in emerging markets are not at all attractive

Looking at some charts over the past decade, we find that emerging market debt spreads have narrowed significantly over the past two years.

AllianzGI, Bloomberg data as of April 16, 2024

While the spreads are described in the chart as not “excessively tight”, I don’t see them as very attractive given that they are still much lower than what we have seen in the past decade.

Emerging market debt funds have continued to perform well even since mid-April, which is where the spread data on the charts above is updated. With the potential risks ahead, now may be a good time to capitalize on some of last year’s strong gains here.

In the context of the past decade, it can be said that risks are high against the backdrop of global macroeconomics. Most economists expect steady global economic growth to continue next year, but relatively tight emerging market debt spreads appear to be pricing in a “mild” economic environment. This comes at a time when “sticky” inflation and elevated geopolitical risks continue to dominate the headlines.

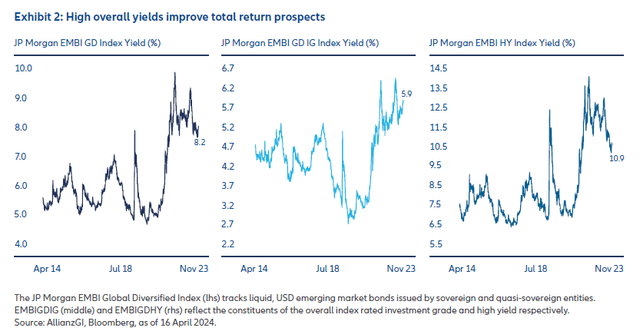

Emerging market bonds offer high total returns, but inflation remains high

Below are the same three charts of emerging market bond indices spanning decades, but displayed by yields instead.

Live Morningstar study as of October 2023 via ninetyone.com

As I mentioned earlier, from a nominal yield perspective, future yield prospects look brighter than they have over the past decade. This may of course be the case, given that this ETF was only generating about 2% per year at the time.

Even if the EMB improves low yields significantly over the past decade, it still needs to overcome what is likely to be higher inflation in the next decade. If inflation remains “stable,” the high returns offered on emerging market debt may not be worth the risk.

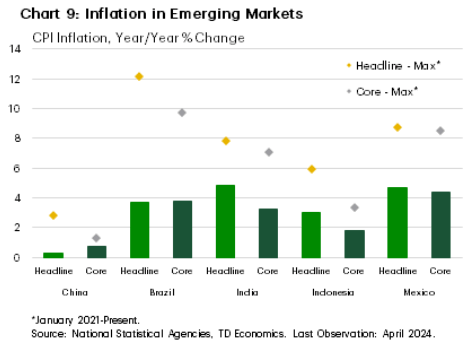

According to TD’s Economic Inflation Tracker, a flat inflation trend was also observed in major emerging market economies. In the words of TD, “ In major emerging markets, inflation has slowed significantly from its peak (Chart 9), but progress has slowed in recent months“.

National Statistical Agencies, TD Economics, data from January 2021 to April 2024.

Will next Fed rate cut help emerging market bonds?

If you read the question above and wonder why I phrased it this way then it’s a given that, well, that’s the point I’m trying to make. There has been a lot of discussion over the past year about choosing an investment to take advantage of upcoming federal interest rate cuts. However, at the same time, we have consistently seen such expected interest rate cuts postponed to the coming months.

Emerging market bonds are an example of an asset class that many investors hope will benefit from the Federal Reserve cutting interest rates, which could lead to a weaker US dollar. On the other hand, a stronger US dollar could be a problem for emerging market countries, as repaying debt financed in US dollars becomes more expensive.

The decline in the US dollar is also often associated with improved risk appetite globally, an environment in which emerging market debt spreads are expected to tighten further.

With emerging market debt spreads having narrowed significantly already in the past couple of years, it makes it a bit worrying for EMB holders to hope for a weaker US dollar.

For investors who are convinced that the US dollar will weaken, they may also prefer to consider investing in emerging market bonds in the local currency. An example of gaining exposure is the iShares JP Morgan EM Local Currency Bond ETF (NYSEARCA:LEMB)

LEMB has underperformed EMB over the past year in a period when the US dollar was more resilient than expected.

Total returns for one year through June 7, 2024, Seeking Alpha.

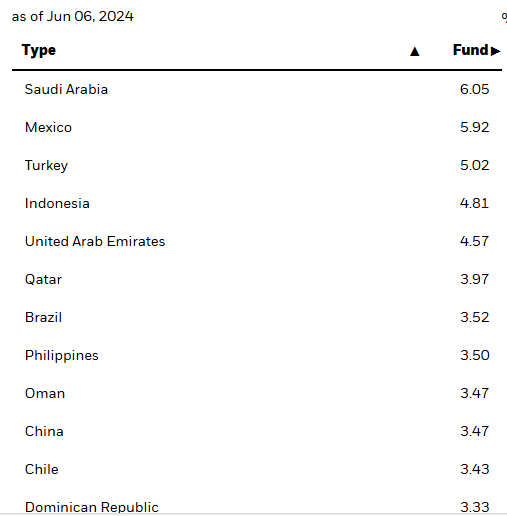

The electoral management body is the country’s most important exposure

Electoral Management Body website, data as of June 6, 2024.

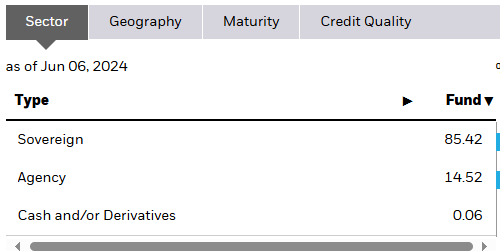

Allocations to the Election Management Body sector

Electoral Management Body website, data as of June 6, 2024.

EMB exposures by credit rating

Electoral Management Body Fact Sheet, data as of 31 March 2024.

Conclusion

If I were looking for a fund that would give me a relatively high monthly income, I would avoid EMB for now. EMB has finally managed to post some solid returns over the past year thanks to shrinking spreads in emerging markets, but now it looks like it’s time for bondholders to take profits.

It remains unclear whether global central banks will be able to fully wave off inflation fears from 2022, including within emerging markets. The Fed’s long-awaited rate-cutting cycle, which many investors also hope will boost sentiment towards the likes of the EMB, also looks increasingly uncertain.

Beyond the uncertain geopolitical environment, recent weeks have also served as a useful reminder of the unpredictability of emerging market politics.

For those who prefer to maintain some core exposure to this asset class, actively managed mutual funds such as MSD or EMD are likely to deliver better returns over the long term.