Mengwen Guo

Investment overview

I give a Buy rating for Endava PLC (New York Stock Exchange: DAFA) The long-term digitization trend remains strong, and I see no reason for it to slow down in the foreseeable future. Generative AI (or AI technology) is a I believe it will be a game-changer, and will continue to drive digital transformation in the business world. My view is that the near-term DAVA growth slowdown is macroeconomic driven, and once the macro backdrop recovers, growth should accelerate back to historical levels easily.

Job description

DAVA provides services and solutions to help companies accelerate their digital transformation, targeting a wide range of industries, from automotive to government to payments and even private equity. Breaking down revenue by geographic region, DAVA has approximately 31% of revenue from North America, 26% from Europe, 34% from the UK, and 9% from the rest of the world.

In Q3 2024, performance wasn’t great across the board. Revenue declined 14.3% to $174.4 million, gross margin declined 1,050 basis points versus 3Q23 to 21.3%, and EBIT margin shifted to 10.5%. As a result, adjusted net margin also declined by the same amount, from 16.8% in Q3 2023 to 7.3%. The good news is that DAVA still has a strong balance sheet, with a net cash position of about $190 million (excluding operating leases).

Growth forecasts

I divide my view on DAVA’s growth outlook into two parts: near-term and long-term.

Statista

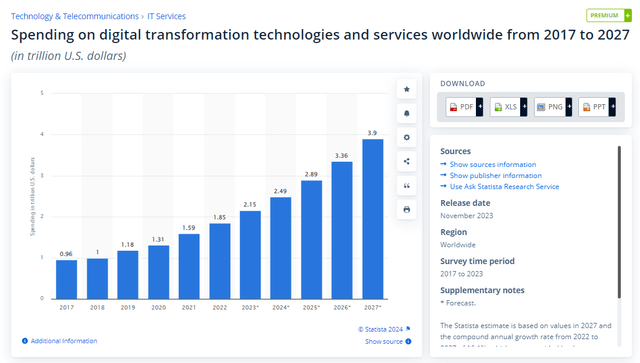

I think the long-term growth outlook for DAVA remains very positive, as I believe digitalization will continue to penetrate every aspect of the business world, and this is happening as I write this post. From an addressable market perspective, spending on digital transformation and global services is expected to reach $3.9 trillion in 2027, representing an increase of more than 50% from 2023 levels.

Dafa

I believe the amount of spending will continue to grow at a rapid rate due to all the various new digital technologies that the world is coming out with. In particular, the game-changing technology is generative AI (or AI technology), because it has proven to deliver significant cost savings and productivity gains, two attributes that are what the majority of companies are aiming for all along. My opinion is that we are still very early in this adoption cycle, as companies are still in the testing phase, where they are putting in minimal resources to test if they can achieve what they are aiming for before deploying more resources into it. There are also hurdles from a risk standpoint, which I believe prevents the adoption process from accelerating. For example, copyright infringement, data privacy laws, etc. However, as companies realize the benefits of generative AI, I expect to see increased adoption, and there are already early signs of this happening, as IT managers move forward with its adoption despite the unknowns. .

In the near term, I think demand will remain weak, not because the trend is slowing down or fading, but because of the overall backdrop. Specifically, the high-rate environment is raising the cost of doing business for many industries, prompting management to postpone any major implementation of digital transformation projects and focus on shorter-duration projects that have an immediate return on investments (i.e., cost-saving projects). . Once we get through this difficult macro backdrop, which appears to be on track with inflation continuing to decline, the Fed should eventually cut interest rates, and this would reinvigorate investments in digital transformation projects.

Remember, this business grew 20-40% year over year between 2017 and 3Q23, and unless there is something structural that has weakened the digital transformation trend, I don’t think the recent slowdown (5% in 2023Q4 , -4% in Q1 2024, -10.6% in Q2 2024, and -14% in Q3 2024) will continue over the long term. In fact, I think this slowdown simply means that There is a lot of pent-up demand waiting to be diverted once the macro backdrop turns for the better. TechTarget’s recent survey supports my view that demand has not evaporated. This dynamic is also consistent with management’s comment about the growth in its pipeline.

I think it goes back to the pipeline conversion problem as we add to the pipeline, it grows, and it’s the speed at which it continues to sign off on the work it started that continues to be the problem. Company’s 3Q24 earnings

Global presence is a competitive advantage

Dafa

The competitive advantage I like about DAVA is that it has a global presence to capitalize on digitalization trends in key regions. Having a global team means DAVA can serve large multinational companies (MNCs) on their digital transformation journey. This is very important because it ensures that digital real estate can be standardized across entities. It is also easier for multinational companies to deal with only one vendor rather than coordinating with multiple vendors, which is very time consuming. Sub-players are disadvantaged because they typically have fewer resources to deploy in areas where there are a large number of agents. Moreover, digital transformation, especially for large enterprises, often has long duration and sales cycles (there are many customizations and iterations) which requires the seller to have sufficient financial resources to continue through the entire process, which is not a luxury for a small player to have ( Unlike DAVA, which has $140 million of net cash and is FCF positive).

Huge upside once growth turns around

May investment ideas

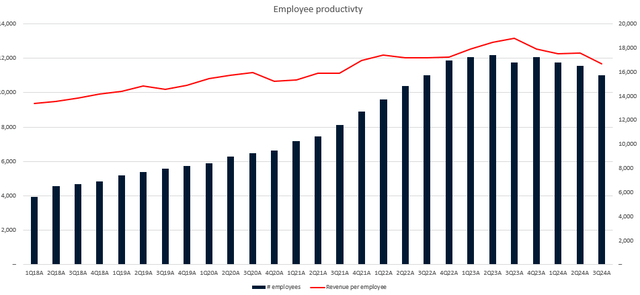

While the adjusted earnings margin has declined, this also means that the upside potential for margin expansion is much greater today. Note that DAVA has historically operated at 10% to 20% EBIT margin. What supports my point is that DAVA has found a way to improve employee productivity (based on revenue per employee) over the years, and even in recent quarters where revenue per employee has declined, it remains above pre-coronavirus levels. Financially, this means that DAVA can now generate the same revenues as it did in the past, but at a lower cost base. Staff costs represent the largest cost in DAVA’s business, because they are the costs that DAVA deploys to facilitate digital transformations.

evaluation

May investment ideas

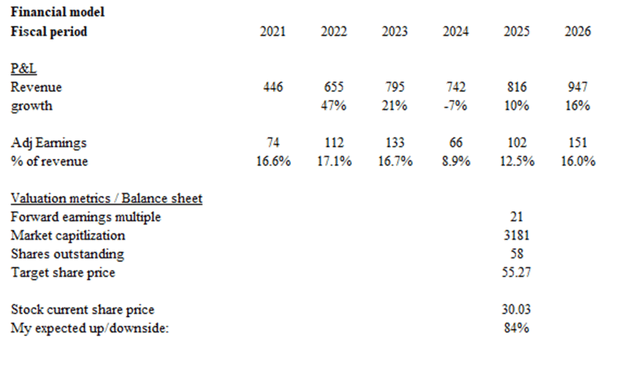

Based on my research and analysis, the expected price target for DAVA is approximately $55.

- Revenues should eventually recover as the macro environment improves. I expect DAVA to meet FY24 guidance of $742 million, followed by a 16% rebound in FY25. My 16% assumption assumes DAVA can grow at least half the rate it has historically, which I note may be too conservative given The trend of digital transformation is strong and I don’t expect to see any slowdown.

- Earnings should recover based on revenue growth, I assume 16%. Profit margin in FY25. Again, this may be too conservative, as DAVA achieved an adjusted earnings margin of 16.6% in FY21 on a revenue base of $446 million. As employee productivity improves, margins will likely rise.

- Shares should trade at no less than their other peers in the digital transformation space today when growth impacts. (TWKS), Accenture plc (ACN), and EPAM Systems, Inc. (EPAM), Cognizant Technology Solutions Corporation (CTSH), etc., which have average expected mid-to-high single-digit growth and trade at an average of ~21x forward P/E.

risk

The continued prolonged poor economic situation will delay the implementation of digital transformation projects, and DAVA will continue to suffer during this period. The timeline for growth recovery will then be delayed further, which also means that valuations will not see an upgrade anytime soon.

Currently, many companies are already powering their digital transformation with AI, but at some point, with more advanced AI models and better hardware to support high-performance computing, companies may rely more on AI to facilitate their digital transformation projects (with On the share away from Dafa). As such, AI could pose a long-term risk to DAVA.

Conclusion

I give DAVA a Buy rating. I believe the long-term trend of digital transformation remains intact and I see no reason to slow down in the long term. My view is that macro headwinds are causing the current weakness and that recovery should occur once the environment improves. Also, although margins are compressed now, I see room for expansion as growth returns due to improved employee productivity.