Monty Racusin

January this year, I released a bullish article about The transfer of energy (New York Stock Exchange: ET) Arguing that its dividend, which at the time yielded roughly 9%, was in a safer position than it had been several years earlier when ET had to cut it. in In the article I also highlighted several dynamics, which, in my opinion, provided quite favorable conditions for ET to achieve strong total returns. In other words, the investment case was not just about dividends, but also about ET’s organic growth and M&A potential.

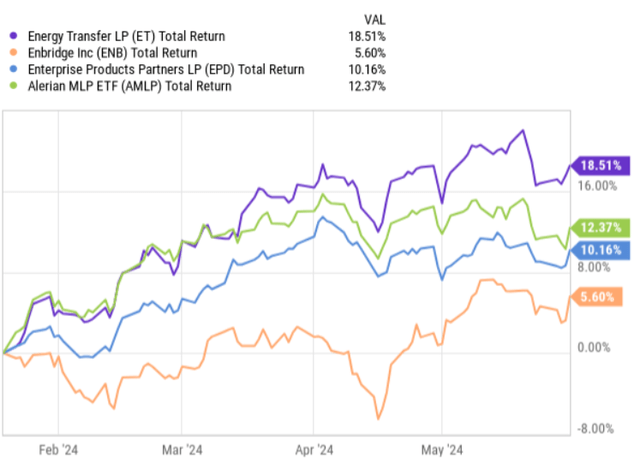

Since publishing this bull case, ET has outperformed the index and other midstream popular names that I also assigned buy ratings to.

Ycharts

This situation, just as it did when you reassessed the situation after the 2023 Q4 earnings report, can raise the issue of overvaluation and whether there is still Decent upside left for ET.

Specifically, in April of this year, I analyzed the Q4 report to see if the fundamentals still justified the above-average multiples and the rise in the stock price. The combination of ET’s strengthening balance sheet, steadily growing business segments and the first signs of a more ambitious M&A program has motivated me to maintain an optimistic view on ET. Since then (April 14, 2024), ET has continued to provide alpha on the MLP index.

Let’s now put the latest data points into the context of the 2024 Q1 earnings report with the current bullish thesis to determine the current appeal of ET.

However, before we analyze the dynamics of the first quarter, I would like to emphasize that my investment strategy is not based on speculation or short-term profits. Instead, I focus primarily on generating attractive profits supported by strong fundamentals, and only then does the capital appreciation component come into play.

Dissertation review

Overall, looking at the key performance metrics for the first quarter of 2024, it should come as no surprise that ET’s stock price has risen in this way. All ET business segments saw growth from Q1 2023 to the previous quarter. Compared to Q1 2023, net income and adjusted EBITDA for Q1 2024 increased 11% and 13%, respectively, driven by higher volumes and more favorable pricing.

Interestingly, registered ET also recorded record volumes in the crude oil pipeline sector, which is one of the most profitable ET sectors (i.e. where the cash conversion rate is the highest). As a result, discounted cash flow in the first quarter of 2024, which reflects the level of real cash generation, reached $2.4 billion compared to $2 billion in the first quarter of last year. This in turn allowed ET to keep about $1.3 billion of cash on its books after paying a quarterly dividend, which on an annual basis yields 8.1%.

If we think about the future, it is important to start with the fact that around 90% of ET’s adjusted EBITDA currently consists of fee-based segments, meaning that only 10% is exposed to fluctuations in commodity markets (i.e. pure commodity). market risk). Given that fee-based segments are tied to cyclical (annual) escalators and are less volatile in nature, they provide the stability needed for ET to keep dividends safe and better manage their leverage profile.

Now, ET recently announced that it will venture into a major acquisition of WTG Midstream by paying approximately $3.2 billion in cash. The new acquisition is intended to be accretive to core DCF generation by adding US$0.04 EPS already in 2025 with expectations (after synergies are achieved) to reach US$0.07 EPS DCF by 2027.

The move goes hand in hand with what Tom Long – co-CEO – announced in a recent earnings call:

Yeah, listen, that’s obviously a very, very good question. We spend a lot of time developing energy transfer strategies here. I will, I guess I’ll start by saying that we still feel that consolidation makes halfway sense. So, answering your 50,000-foot question, we’re still very intentional about evaluating different opportunities as we look forward. So we won’t slow down on that front. Now, as much as we look at it, we’ll always try to look at those things that feed along the way. We always like to talk about how we go from wellhead to water and we do that across all commodities. So you can see our strategy when we look at these things and what assets we look at in terms of how we feed them throughout the value chain when we make these acquisitions.

In other words, ET has clearly ramped up its mergers and acquisitions to extract the benefits of a rather fragmented market. There is also a benefit to inorganic growth in the form of increased diversification and especially discounted cash flow generation as we can, for example, observe by looking at the details of the acquisition of WTG Midstream.

With all that said, one might question ET’s ability to keep the balance sheet protected. This may actually become a problem if ET continues to announce large transactions carried out on a cash basis. However, given the current data points, I see no risks at the bottom end of the balance sheet.

First, as shown above, ET can hold about $1.3 billion in cash each quarter – and that’s after debt service and dividends.

Second, maintenance capital expenditure is very low compared to quarterly cash retention. For example, in the first quarter of 2024, ET spent approximately $460 million on organic growth capital, which still leaves a significant amount of liquidity remaining to direct toward M&A.

Third, ET took some notable steps in reducing its preferred stock positions, by redeeming all of its outstanding Series E preferred units. During the quarter, ET also redeemed $1.7 billion of preferred notes using part cash and part of its credit revolver.

Fourth, along with the first-quarter results, management raised its adjusted EBITDA guidance to $15 billion to $15.3 billion, compared to the previous guidance range of $14.5 billion to $14.8 billion. This will allow ET to access larger amounts of liquidity each quarter to fund acquisitions or further improve the balance sheet.

Now, while I mentioned earlier in the article that the bull case for ET is not based on short-term results or ET’s ability to match consensus forecasts (rather a focus on attractive and steadily growing earnings), I believe that ET will be able to deliver EBIT generation. and Revised Depreciation and Amortization (EBITDA). The main driver behind the increase in EBITDA guidance is the integration (or consolidation) of NuStar’s assets, which closed in May of this year. This impact alone contributes to an additional $500 million in EBITDA, the remainder of which can be easily covered by further add-on acquisitions and continued strong demand for oil and natural gas.

Finally, one can prove theoretically that the ET multiplier has expanded quite a bit and has now reached fairly high levels. While its EV/EBITDA of 7.8x could be considered above average over the past 24 months, if we compare it to some of its more direct peers like Enbridge (NYSE:ENB)(TSX:ENB:CA) and Enterprise Product Partners (NYSE:EPD) ) or Plains All American Pipeline (NASDAQ:PAA), we will realize that ET is still undervalued. For example, the EV/EBITDA for ENB, EPD, and PAA is 11.3x, 9.3x, and 9.2x. Given ET’s growth momentum supported by its investment grade balance sheet, the stock is cheap in my view.

Bottom line

In my opinion, the recent rise in ET stock does not mean that the upside has already been exhausted. The increase in share price was driven by strong underlying business performance and improving growth prospects, as early signs of this were noted in my previous article (April, this year) about ET.

Since updating my thesis, ET has begun to take concrete steps by implementing its M&A strategy to capture the benefits of the fragmented midstream market, as increased consolidation should allow ET to be more diversified and maintain its DCF growth momentum.

Due to the combination of stronger EBITDA growth, accretive acquisitions, lower capex, and ample quarterly cash retention (after servicing earnings of ~8%), ET’s financial risks remain well managed.

As a result of the above dynamics, improving growth profile and attractive, well-covered dividend, Energy Transfer remains a strong buy for me.