com. onurdongel

Williams Enterprises (WMB) has just received a permanent injunction to stop transmission of energy (New York Stock Exchange: ET) from blocking its access to certain “right-of-way” areas to which Energy Transfer has access. This is the second judicial decision against the company When it comes to not sharing “right of way” space. Condominium owners should be concerned as these decisions pile up because sufficient provisions in one direction should result in a change in corporate policy rendering the rest of operations moot. Otherwise, the courts may take additional action that may cost the company a large amount of money. That’s why I prefer to watch this situation from the sidelines until I see a fundamental change in the story unfolding.

Find an Alpha article on the court’s decision on right of access between Energy Transfer and Williams (Search for Alpha website June 5, 2024)

As I noted in the last article I wrote, once losses start to pile up, courts have the option of punishing something deemed trivial. This combined with any recourse the winners may have to recover additional costs due to the delay in filing a claim becomes clear that it will not work. At what point this happens is anyone’s guess. However, Williams is a company worth listening to. If the Williams administration feels this case is a winner and the court then agrees, the remaining cases in progress should be reviewed for viability.

DT Midstream (DTM) was the other judgment issued against the company. These are not fly-by-night operations that win cases in court. Energy Transfer has had a poor record in court the entire time I’ve been following them. The partnership has some wins. But the losses seem to outweigh those few victories.

The courts are tired of the same type of cases being brought before them when the outcome is clear before the case is filed. When this happens, the court’s options can range from no monetary impact to significant monetary impact to discourage filings.

As the Department of Energy Transportation noted in the statement quoted above, they feel that other companies are acting unreasonably. But so far, the courts don’t agree, and apparently there are quite a few law firms that agree with the other side. To me, this is “playing with fire” and it’s only a matter of time before something somewhere down the line burns common unit holders.

Dakota Access Pipeline Dispute

Recently, resolution of the dispute was also postponed until fiscal year 2025. As I discussed in previous articles, proposed solutions range from removing the pipeline to allowing operations to continue as they were. The decision may cost the company nothing, or it may cost the company a large amount of money.

What does this mean

What has changed from the last article is that there is now a specific announcement of a postponed deadline here (replacing expectations), while the outcome of the issues in the other dispute is now clearer. The change here is shareholder neutral as there is no more future clarity than there was before.

But the dispute with Williams clearly indicates that these issues are moving in one direction, which is not in the company’s favor. No one can guess how many more cases will test the court’s patience and result in more costs. But it has become clear that a change in strategy is needed before costs rise (if they ever do).

Shareholders should already be concerned about the sheer number of cases this company has lost over the years since it began pursuing it. Administrative court cases can delay the project, resulting in a lower return on capital than previously reported. There has to be a less expensive way to handle these types of potential disputes.

Acquisition of WTG Midstream Holdings

Hopefully, the announcement of plans to issue up to 51 million common units to acquire WTG Midstream Holdings from its owners is a good move for the company. Diamondback Energy (FANG) was one of the sellers.

Of concern here is the fact that many of these acquisitions do not appear to have led to sufficient progress in earnings per share. What they will do is make Energy Transfer a larger company to better withstand any unfavorable rulings in some disputes.

In the last quarter after the latest acquisition, EPS remained essentially the same while other metrics like cash flow per share had some single-digit percentage gains (because outstanding shares gained in addition to absolute gains in some cash flow metrics).

Compare that to Enterprise Products Partners (EPD) which made an acquisition in fiscal 2022. Not only did common units jump when the acquisition was announced, but it followed a full year of double-digit growth. The performance of this acquisition has been better than anything I’ve seen on a per-unit power transmission basis.

Full return

The last 10-year period has affected all transportation stocks, as the significant decline in oil prices in 2015 led to a re-evaluation of the industry. 2018 has cemented in the market that growth will be very different if it continues at all.

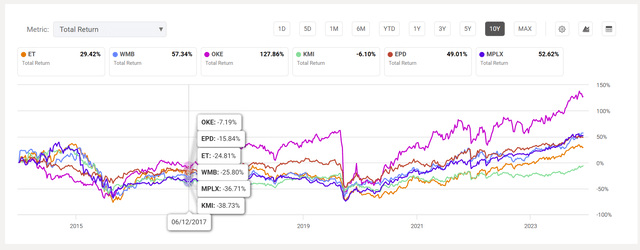

Total energy transmission return compared to other medium carriers (Search for Alpha website June 5, 2024)

However, the total return shown above is lower than the mid-term average return for the period as calculated by Seeking Alpha. Clearly, investors can get better returns without the risk that all the court cases pose for future joint power transmission units.

The ten-year period is useful because any company can have one good year. A longer time period may be a better indicator of management’s ability to return cash to common unitholders.

Readers are advised to read the most recent 10-Q on pages 21 through 31 to get an idea of potential future liabilities in the event the company ends up with an unfavorable outcome after all appeals have been exhausted. 10 pages is considered a menu for any company. I follow several companies that don’t have anything close to a long-running list of potential contingencies in their 10-Q.

But note that management believes it has meritorious defenses in every case and does not believe it has much liability. Note also that, as was the case at the beginning of the article, the disputes associated with Williams are at least not currently in the company’s favour.

This means that the range of possibilities is for legal expenses to continue to an unfavorable outcome in each case.

summary

Energy Transfer is a company with investment grade debt. Now, there is a significant amount of preferred equity between that investment grade debt (although some preferred equity is called) and that debt which can raise leverage with respect to common unitholders.

In many companies, there is a good possibility that the contingency portion of the 10-Q will contain information that is likely to impede the movement of the common unit price. For the foreseeable future, this is expected to continue.

As the Seeking Alpha website chart shows, there are plenty of other opportunities to get a better return without all the drama here. At the very least, I would consider a well-managed partnership like Enterprise Products Partners because it doesn’t have all the contingencies mentioned here.

To me, this is not a suitable investment for an income-oriented investor until the legal issues are resolved further. For those who want to speculate with a small position, by all means they should do so. Just realize that you may suffer a significant loss of capital in the future if this issue is not monitored closely.

For me, this is selling until the legal risk decreases.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.